The Morning Transition from Batch to Intraday Liquidity

Timing windows are precise and governed by the settlement window timing protocols established by the Federal Reserve and Nacha. For many regional and national banks, the second major update occurs between 8:00 AM and 9:00 AM Eastern Time.

This period aligns with the transition from overnight batch processing to intraday liquidity management. During this hour, the Federal Reserve Bank services finalize the settlement of future-dated entries and Same Day ACH files. Readers can review the official documentation regarding settlement timing directly through the appropriate U.S. government source.

Behind the scenes, institutions manage their liquidity by balancing these incoming credits against their required reserve buffers. A bank must ensure it has sufficient “good funds” in its Federal Reserve account before it can legally finalize the credits.

This is especially true when analyzing institutional risk positioning during high-volume periods like tax season. Large institutions often wait for the 8:00 AM window to ensure their overnight interbank lending obligations are met before releasing retail liquidity.

This sequence protects the bank from technical overdrafts in their reserve accounts while ensuring compliance with federal mandates. The Bureau of the Fiscal Service also plays a role in this timing for federal payments like Social Security or refunds.

These files are often sent to the Federal Reserve in massive sequences that require significant processing time at the recipient bank. If the transmission begins late in the evening, the final file might not reach a bank’s processing queue until 8:00 AM.

This explains why one neighbor might see their deposit at midnight while another waits until the start of the business day. Precise coordination ensures that trillions of dollars move without destabilizing the broader market liquidity of the nation.

Reconciling the Final Handshake Between Systems

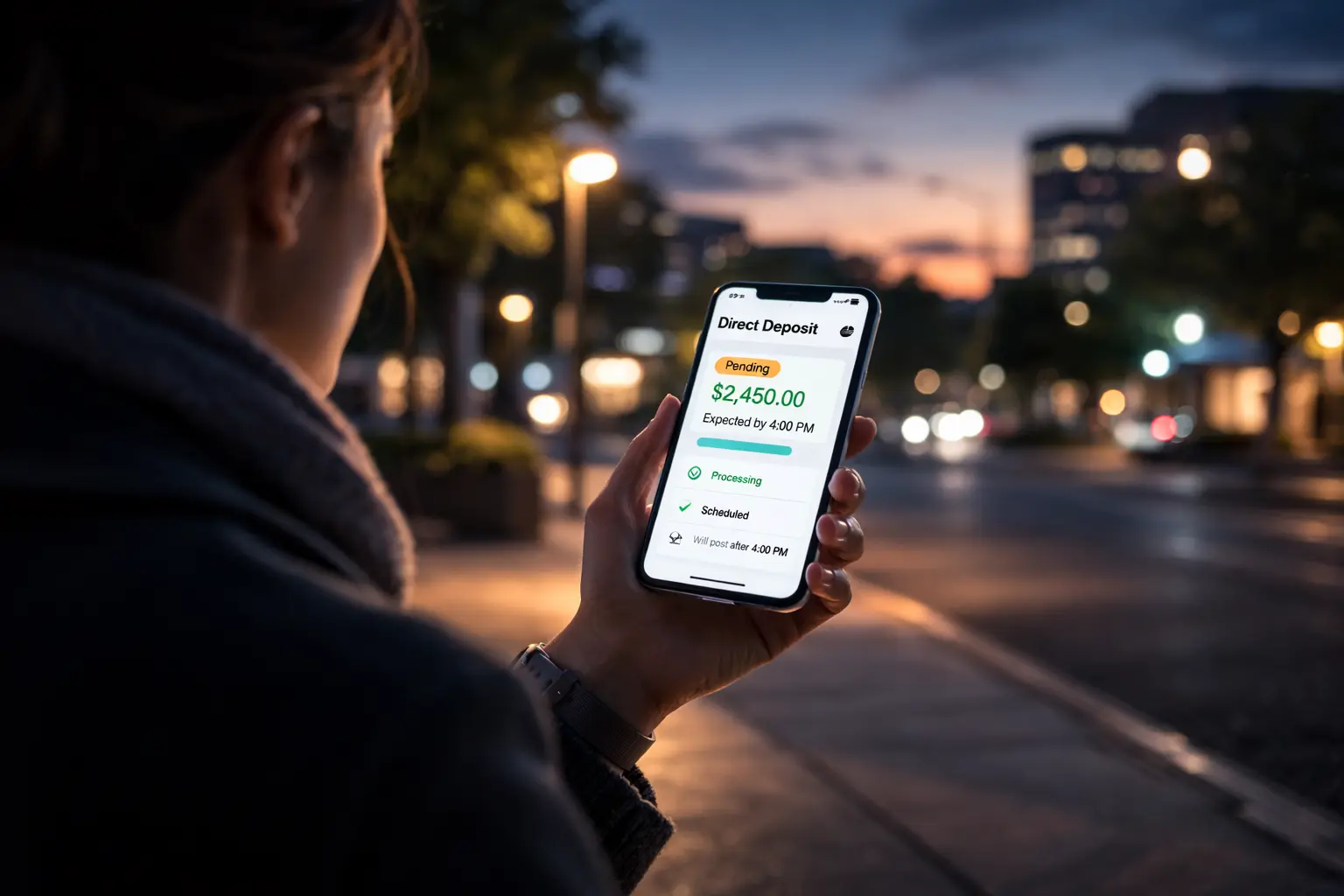

From the household perspective, this 8:00 AM gap is simply a matter of technical sequencing. If the money is not there at 7:45 AM, it often arrives by 9:15 AM as the bank completes reconciliation. This hour represents the final “handshake” between the federal infrastructure and the private ledger.

Knowing this timing helps residents plan their morning bill payments or transfers with greater accuracy. It replaces the anxiety of the “missing” deposit with the predictability of the system’s schedule. Readers can explore detailed breakdowns of these transmission schedules through the Bureau of the Fiscal Service’s Green Book.

Institutional risk modeling further dictates how these morning windows are utilized by various bank tiers. Smaller community banks may lack the automated high-frequency ledger updates found at larger “Money Center” banks. Consequently, they might batch all morning arrivals into a single 9:00 AM release to ensure their liquidity ratios remain stable.

This behavior connects the liquidity timing household stability directly to the infrastructure choices made by their specific financial provider. The system does not move slowly by accident; it moves at the speed of verified security.

In the end, the movement of money is a governed, mechanical process rather than an instantaneous digital miracle. The banking system operates on a logic of safety and verification that prioritizes structural integrity over speed.

Understanding the 8:00 AM settlement gap reinforces that a banking liquidity shift is a function of the architecture itself. When the system behaves as expected, it creates a foundation of stability that allows the American economy to function with precision. Reframing these morning minutes from a period of doubt into one of structural awareness restores a sense of agency.

Author