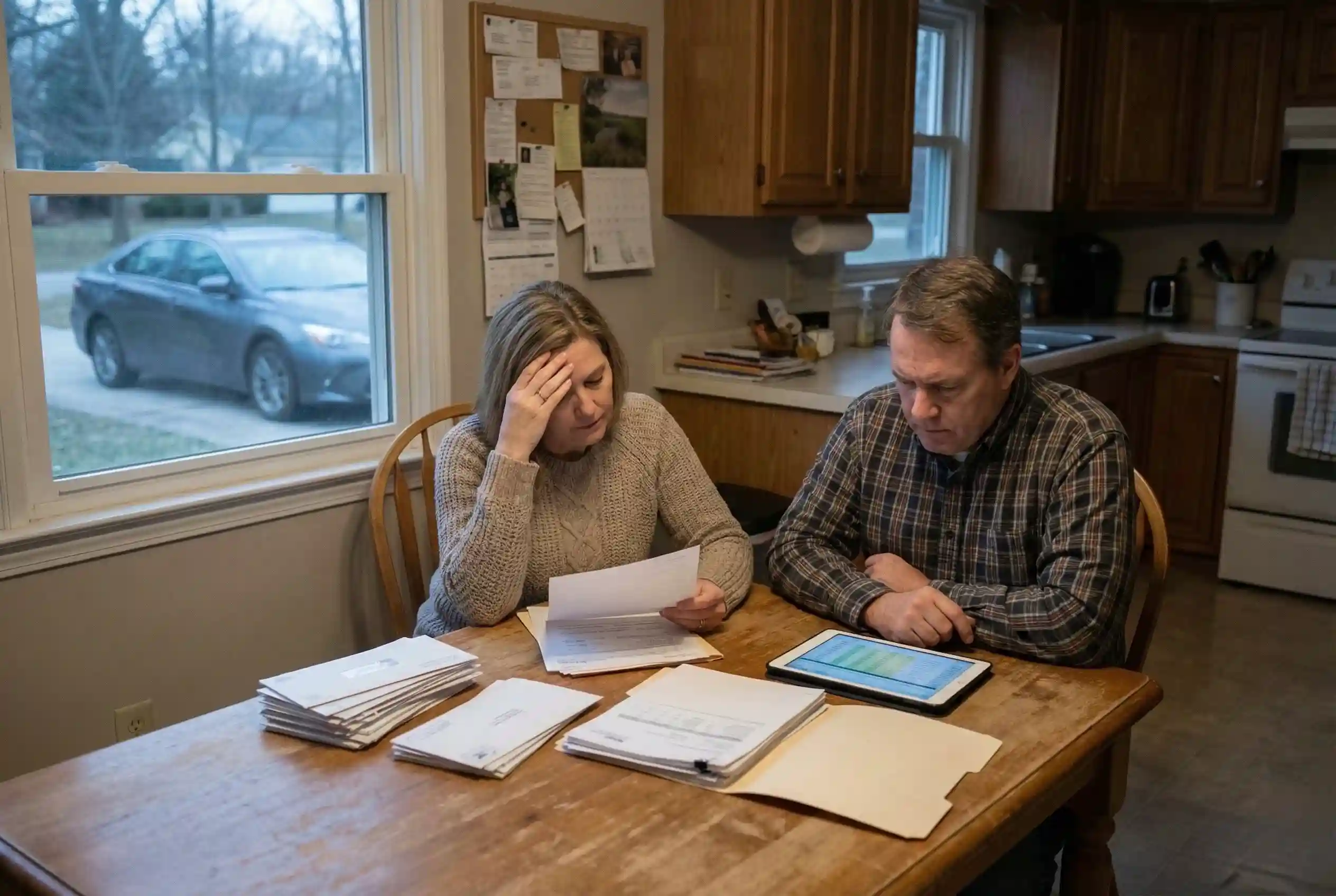

The envelope usually arrives on an ordinary weekday. There’s no warning label or bold red text demanding attention. It sits quietly among grocery ads and credit card offers, looking like routine mail.

You open it casually, expecting standard language and maybe a modest adjustment — until you see the number and realize your monthly escrow payment is jumping by hundreds of dollars, not a few.

For many homeowners, this is the moment when financial certainty starts to wobble.

Mortgage payments were supposed to be predictable, a stabilizing anchor in household budgets. Instead, rising home insurance costs are turning once-fixed expenses into moving targets.

Even as families focus on food prices and everyday inflation, insurance has been quietly reshaping the cost of homeownership in the background.

A Hidden Shift Most Homeowners Never See Coming

Over the past few years, attention has stayed locked on interest rates and visible inflation. What most homeowners missed was the quieter shift happening inside insurance pricing models across the country.

Risk assessments are being rewritten, often without notice, by algorithms that reassess neighborhoods, building materials, and long-term exposure.

This change isn’t driven by a single storm or unlucky season. It’s the result of insurers deciding that certain zip codes no longer offer the same protection they once did.

By the time renewal letters arrive, the recalculation has already happened — and for many households, alternatives are limited.

This Isn’t a Temporary Spike—It’s a Reset

What homeowners are experiencing now isn’t a billing error or a short-term fluctuation. It’s a structural reset. For decades, home insurance remained relatively affordable because rebuilding costs were manageable and weather risks were stable. That balance no longer exists.

Rebuilding a standard home today costs far more than it did just a few years ago, while wages haven’t kept pace. Insurers aren’t absorbing that gap.

Instead, rising home insurance costs are becoming one of the fastest-growing household expenses in certain regions, quietly reshaping affordability.

Why Repairs Are Driving Premiums Higher

Storms grab headlines, but insurers focus on something more practical: repair bills. A damaged roof or flooded interior today costs significantly more to fix than it did in 2019.

Materials are pricier, skilled labor is harder to secure, and supply chains remain fragile.

Insurers now price policies based not just on past events, but on projected worst-case scenarios. Behind local insurance companies sit global reinsurance firms that absorb catastrophic risk.

When those reinsurers raise rates, the cost flows straight to homeowners—with no cushion and little warning.

Technology Is Changing How Risk Is Calculated

Modern insurance pricing relies heavily on data most homeowners never see.

Satellite imagery, drone inspections, and predictive modeling allow insurers to evaluate properties remotely with remarkable precision.

Roof condition, building age, and environmental exposure can all be assessed without a single site visit.

This shift means homeowners can be penalized for risks they didn’t even realize existed, simply because of where or when their home was built.

As a result, home insurance costs are rising even in places that once felt financially stable and low-risk.

Why the Increases Are Spreading Inland

Insurance pressure used to feel regional, confined to coastal or wildfire-prone states. That assumption no longer holds.

Inland states are now seeing meaningful increases tied to secondary risks like hailstorms, flash flooding, and severe convective weather that rarely makes national news.

Housing data from the U.S. Census Bureau shows affordability tightening from multiple angles, with insurance playing a growing role.

In some areas, insurers are exiting markets altogether, issuing non-renewal notices that leave families scrambling for alternatives.

What Homeowners Usually Notice First

Most homeowners never see the risk models or reinsurance data driving premium decisions. What they notice instead are smaller, easy-to-miss changes.

Deductibles creep higher, fewer insurers offer renewal quotes, and policy language starts to feel tighter than it did a year ago.

These early signals often arrive long before major price jumps. By the time renewal notices show a sharp increase in home insurance costs, the shift has already been underway.

That’s why so many families feel blindsided—the warning signs didn’t look like warnings at the time.

The Burden Falls Heaviest on Middle-Income Families

Premium increases affect everyone, but the impact isn’t evenly distributed. Wealthier households can absorb higher costs or self-insure.

Middle-income families often can’t, forcing difficult trade-offs between protection and affordability. Higher deductibles, reduced coverage, and increased exposure are becoming common compromises.

Many homeowners remain insured on paper but are functionally vulnerable, one major storm away from serious financial strain.

When Coverage Shrinks Without You Noticing

Rising premiums are only part of the problem. To slow headline increases, insurers are quietly changing policy terms.

Coverage that once paid full replacement cost may now cover only depreciated value — a difference that becomes painfully clear after damage occurs.

Percentage-based deductibles are also replacing flat amounts in higher-risk areas.

A small percentage can translate into thousands of dollars out of pocket. Understanding your insurance coverage now matters just as much as the premium itself.

What Homeowners Can Do Before Renewal Season

You can’t control weather patterns or global reinsurance markets, but you can stop being passive. Auto-renewal has become risky.

Shopping policies every couple of years is essential — not just for price, but for coverage quality. Knowing what it would truly cost to rebuild your home today is critical.

Compare insurer estimates with construction cost data and ask direct questions about deductibles, exclusions, and code-upgrade coverage. These details determine whether insurance protects you when it matters most.

Balancing Risk With Financial Reality

If you have a strong emergency fund, accepting a higher deductible may be a strategic choice. But that decision should be intentional, not forced by confusing renewal documents.

Insurers are also beginning to reward homeowners who reduce risk.

Impact-resistant roofing, leak-detection systems, and routine property maintenance now function as financial defenses, helping control home insurance costs over time.

The New Reality of Homeownership

The era of “set it and forget it” homeownership is fading. Owning a home today requires awareness, not panic.

The anxiety many homeowners feel is a rational response to a system that’s changing quietly but decisively. Navigating today’s financial headwinds means paying attention to the unglamorous details others overlook.

In a world where safety nets are thinning, understanding how home insurance costs are changing is no longer optional it’s essential.

Author

-

The information on this site is for educational and general guidance only. It is not intended as financial, legal, or investment advice. Always consult a licensed professional for advice specific to your situation. We do not guarantee the accuracy, completeness, or suitability of any content. For complete details, please review our full disclaimer.