If you received a CP53E notice from the IRS this morning, your tax refund has hit a critical administrative bottleneck. Under a new 2026 federal mandate, the IRS has largely phased out the automatic issuance of paper checks when a direct deposit fails.

Instead of receiving a check in the mail a few days after a bank rejection, your funds are now being held in a “temporary freeze” that requires immediate taxpayer intervention to release. This 30-day freeze is part of a broader shift in the us money movement toward fully electronic disbursements.

For filers who were counting on their refund this week, the arrival of this notice signifies that the “pipes” moving your money have been blocked due to a bank account mismatch or a rejected transfer.

What Taxpayers are Seeing in Bank Accounts Right Now

Taxpayers across the country are logging into their banking apps today only to find that expected refunds have vanished or were briefly visible as “Pending” before disappearing entirely. When a bank rejects a deposit, often due to a typo in the routing number or a closed account, the funds are sent back to the Treasury.

In previous years, this would trigger an automatic paper check, but in 2026, it triggers a CP53E notice. The notice informs the recipient that the IRS attempted to send the refund but could not complete the transaction. Until you act, the money remains in the treasury payment rather than being re-routed to your mailbox.

Why the IRS Frozen Your Refund for 30 Days

The 30-day window is a mandatory “correction period” established by Executive Order 14247. The goal is to force the transition to digital payments by giving taxpayers one opportunity to provide a valid bank account.

During this time, your refund is technically “frozen” at the Treasury level, meaning it is not earning interest and cannot be accessed by any other agency or creditor. This freeze prevents the IRS from issuing a paper check immediately.

The agency’s new policy is to wait until the 30-day clock expires before even beginning the manual process of printing and mailing a physical check, a process that can add up to six weeks to your wait time.

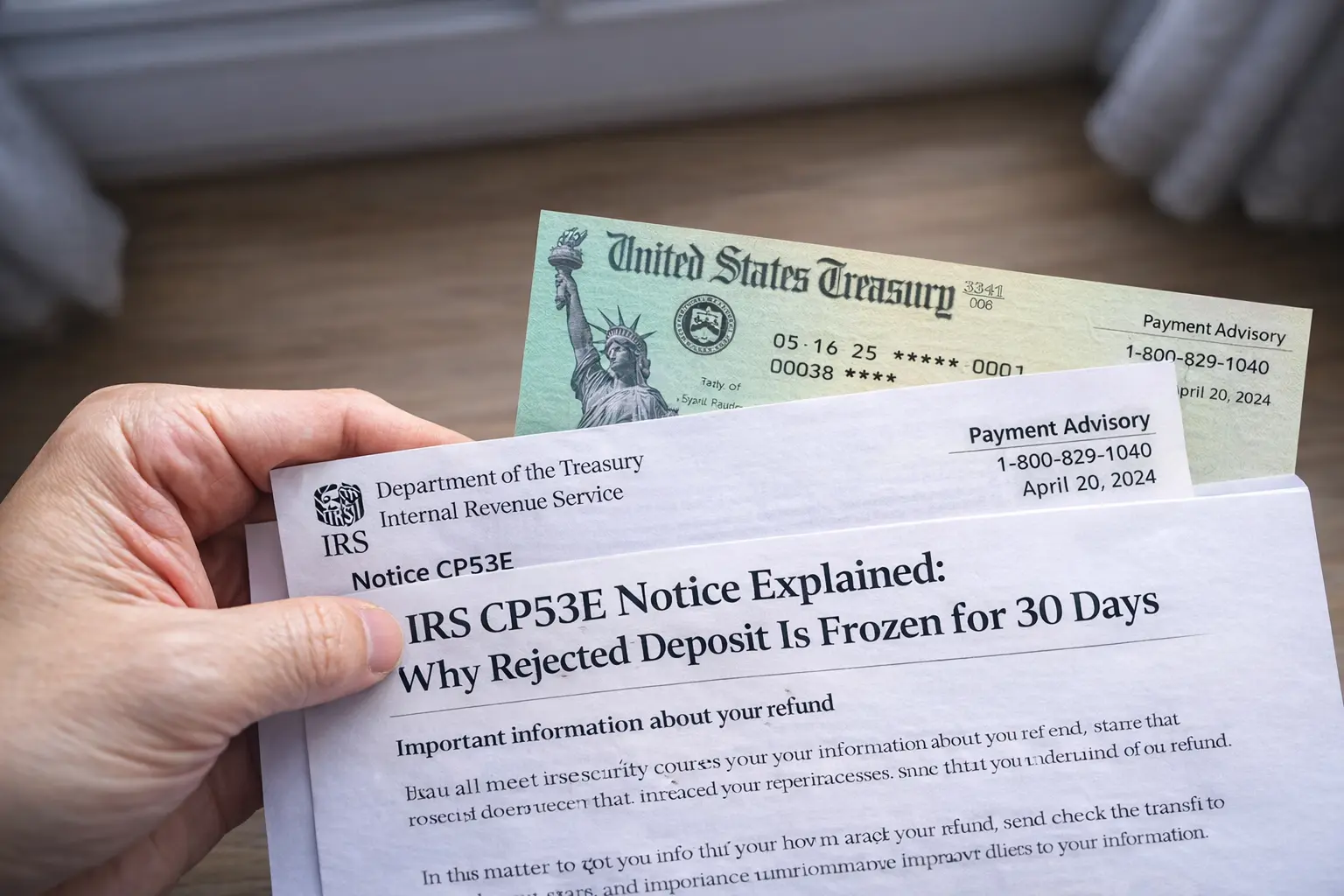

Understanding the CP53E Notice and the 2026 Paper Check Phase-Out

The CP53E notice is the official “bridge” between a failed electronic transfer and a final paper check. Because the IRS is aggressively retiring paper instruments to save costs and reduce mail theft, the federal payment status of your refund will remain in a “Hold” pattern until you log into your IRS Online Account to update your details.

If you ignore the notice, the system assumes you do not have access to a digital account. However, the “Safety Net” check won’t be authorized until the 30-day response window has fully closed, creating a significant delay for households that need liquidity now.

How the Federal Reserve Settlement Window Affects Rejections

When a bank rejects a direct deposit, it doesn’t just “stop” the money; it must initiate a “Return” file through the Federal Reserve’s ACH network. This settlement window timing typically takes two to three business days. Only after the Federal Reserve confirms the return to the Treasury does the IRS system generate the CP53E notice.

This means by the time you receive the letter in the mail, your money has already traveled back through the invisible payment rails and is sitting in a holding account at the Bureau of the Fiscal Service.

Why You Only Have One Chance to Fix the Rejection

A critical detail of the 2026 rule is the “One-Shot” update policy. The IRS allows you to update your banking information through your Online Account exactly once per tax year. If the updated information you provide is also incorrect and results in a second direct deposit settlement failure, the digital option is permanently disabled for that refund.

At that point, the refund is automatically moved to the “Paper Check Queue,” and you may be forced to wait until late spring or early summer to receive your funds via the U.S. Postal Service.

Why Some Deposits Are Rejected Even with Correct Numbers

In some cases, the CP53E notice arrives even if you entered your account and routing numbers correctly. This often happens due to “Mismatched Name” flags or “Account Type” restrictions. For example, if you tried to send a joint tax refund to a bank account held only in one spouse’s name, the bank’s overnight bank clearing filters may flag it as a third-party payment and reject it.

Additionally, some savings accounts have limits on the number of ACH transfers they can receive. If your refund exceeds these internal bank limits, the deposit will bounce back, triggering the 30-day freeze.

What You Should Check in Your IRS Online Account Right Now

If you have received the notice, you must log into your Official IRS Online Account immediately. Do not call the IRS toll-free line to provide bank details; for security reasons, IRS employees are no longer authorized to take banking information over the phone.

Look for the “Refund Status” or “Tax Records” tab. You should see a prompt to “Update Direct Deposit Information.” If the deposit not there status is still showing on the IRS “Where’s My Refund” tool, it may take another 24 hours for the online portal to open the update window.

What Happens if You Miss the 30-Day Deadline

If you do not respond to the CP53E notice within 30 days, the IRS will eventually “unfreeze” the funds and issue a paper check by default. However, this is the slowest possible path to your money. The federal payment pipeline for paper checks is now deprioritized behind all digital transfers.

Most taxpayers who fail to respond to the notice report that their paper check does not arrive for 6 to 10 weeks after the initial freeze date. In the current economic environment, this delay can be devastating for those relying on their refund for essential bills.

Final Outlook on the 2026 Refund Freeze

The CP53E notice is not an audit; it is a technical correction. While the “30-Day Freeze” is frustrating, it is a solvable problem if you act quickly. By understanding the overnight bank clearing cycles and the new digital-first rules of the Treasury, you can navigate this bottleneck and release your funds.

Make sure to double-check your updated banking details before hitting “Submit” on the IRS portal. A successful update today can see your refund hit your account in as little as 5 to 7 business days, bypassing the 10-week wait for a paper check.

Author