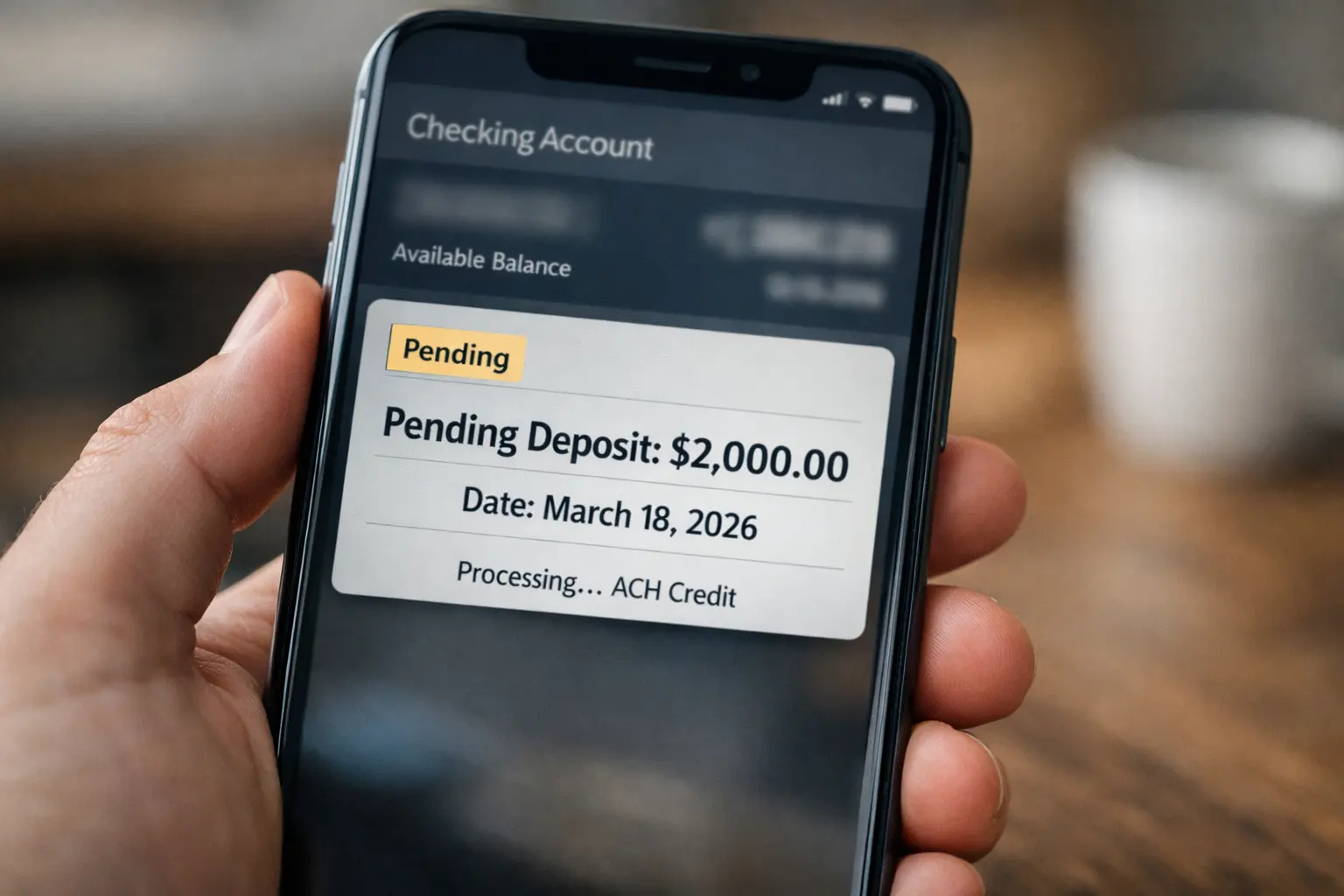

The digital banking landscape across the United States is currently flooded with a wave of specific transactions as millions of Americans check their mobile apps to find a 2000 dollar deposit sitting in a pending state.

This massive movement of capital on March 18 2026 is not a glitch but a coordinated release of federal funds triggered by the One Big Beautiful Bill Act known as OBBBA.

While the money is visible for many it remains inaccessible for immediate withdrawal creating a high level of financial tension for households relying on these settlements.

To understand why your balance has not updated you must look past the surface of your banking app and into the invisible rails of the national money movement system.

The OBBBA Release and $2000 Payout Logic

The primary driver of the current $2,000 deposit wave is the secondary implementation phase of the OBBBA legislation. Unlike previous tax years where refunds were distributed in smaller erratic batches the 2026 framework has consolidated millions of individual taxpayer credits into a massive single day disbursal.

This has created a technical bottleneck within the FedACH network which is responsible for the final settlement of these funds. Many users are seeing the exact amount of 2000 dollars because this represents the standardized advanced credit authorized under the new legislative rules.

If you are seeing this amount as pending it confirms that the Treasury has successfully transmitted the payment file to your financial institution. However the transition from direct deposits show pending to an available balance depends entirely on your bank internal liquidity timing.

While the funds are technically at the bank they are often held in a memo post status until the Federal Reserve completes the final ledger refresh which is scheduled for the mid afternoon window today.

Federal Reserve Settlement Friction Today

A critical reason for the delay that mainstream financial news is overlooking is the integration of the ISO 20022 messaging standards. This update to the us money movement system allows for more secure transactions but it has introduced a layer of verification that slows down the traditional midnight posting cycle.

Banks are now required to match specific identity markers before a federal deposit can clear a pending status. This is particularly relevant for those who have recently moved or changed their primary banking relationship.

For those tracking their status through official channels it is essential to verify the transcript for any presence of Code 846 which indicates the Treasury has released the hold.

If the code is present with today date but the money remains pending the friction is occurring at the bank posting timing level rather than a federal error. Most major institutions like Chase Wells Fargo and Bank of America are processing these in three distinct waves with the final wave expected to clear shortly after the 1 PM refresh.

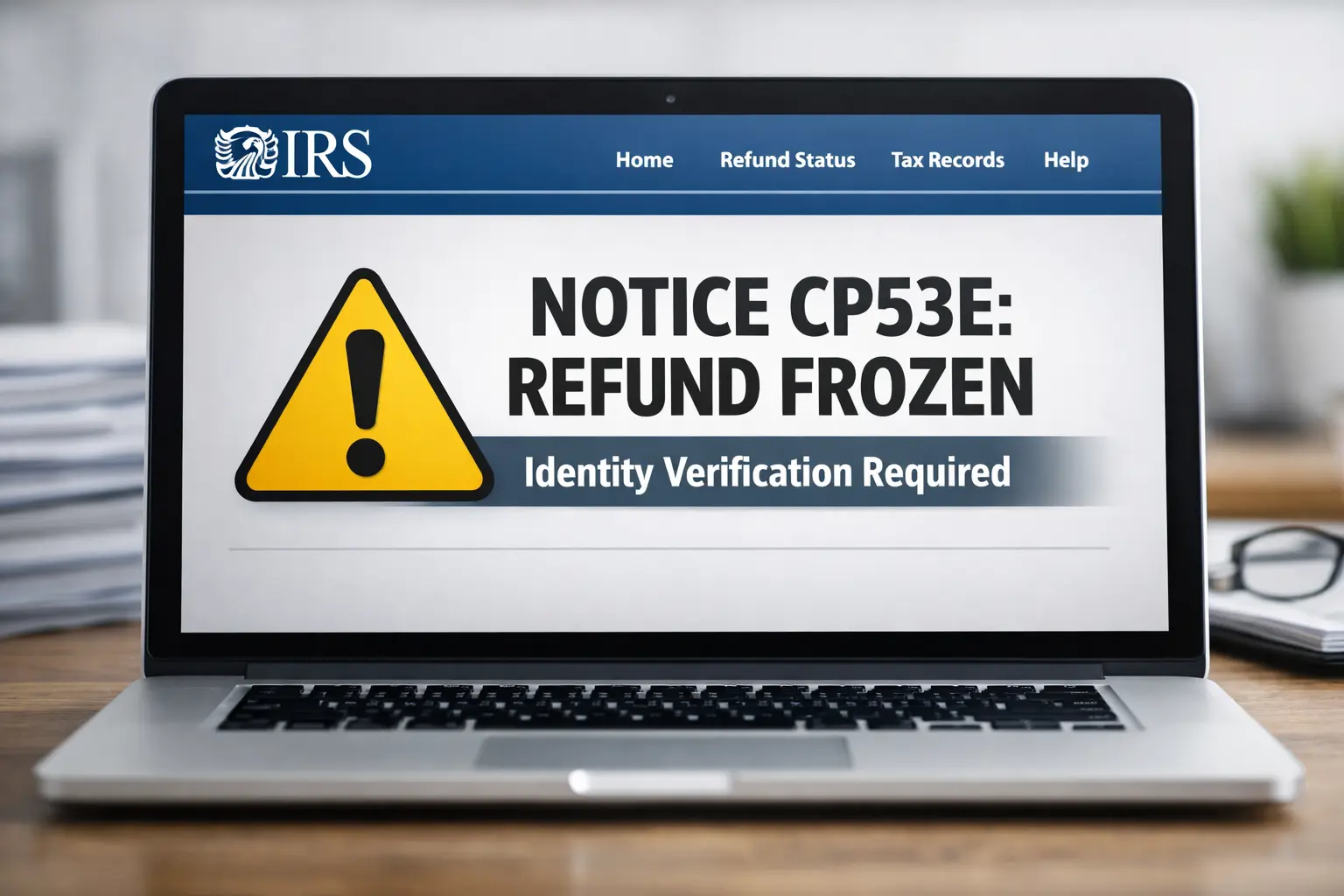

The Hidden Impact of the CP53E Freeze

While most people will see their $2,000 deposits clear by the end of the day a significant group of taxpayers is facing a more permanent delay due to the CP53E notice.

Under the 2026 tax modernization rules any refund that encounters a routing mismatch or a flagged identity profile is immediately placed in a hard freeze. This prevents the funds from being moved and results in a federal payment released balance frozen notification.

If your deposit has been pending for more than 24 hours without moving to an available status you may need to check your secure IRS portal for a CP53E alert. This notice requires a manual update of your banking credentials before the funds are re released.

This is a departure from previous years where a paper check would be mailed automatically. In the current system the onus is on the recipient to resolve the flag before the next deposit wave clears in the following week cycle.

Banking Liquidity and The 1 PM Refresh

The final piece of the puzzle for today March 18 involves the way banks manage their daily liquidity. Federal payments are not credited to accounts in a continuous stream but rather in specific settlement windows.

The most important window for today is the 1 PM local time refresh. This is the moment when banks reconcile their internal ledgers with the Federal Reserve settlement files. For the millions of Americans currently staring at a pending screen this 1 PM window is the most likely time for the funds to become spendable.

If you find that your deposit is not there this morning it is vital to avoid excessive refreshing of your banking portal which can sometimes trigger security pauses on the account.

Instead rely on the technical certainty that banks control payment posting and the vast majority of the OBBBA $2,000 credits are slated for final availability before the close of the business day.

Managing Your Available Balance Expectation

As the afternoon progresses the focus shifts from receiving the file to the true liquidity available balance in your account. It is common for the total balance to show the $2,000 while the available balance remains unchanged.

This discrepancy is a byproduct of the overnight bank clearing cycles catching up with the massive daytime volume of the OBBBA release. By understanding that these delays are structural and technical rather than individual errors you can better manage your household finances today.

Investozora will continue to provide real time updates on the money movement system settlement to ensure you have the latest information on why your money is moving at the speed of the 2026 modern banking rails.

Author