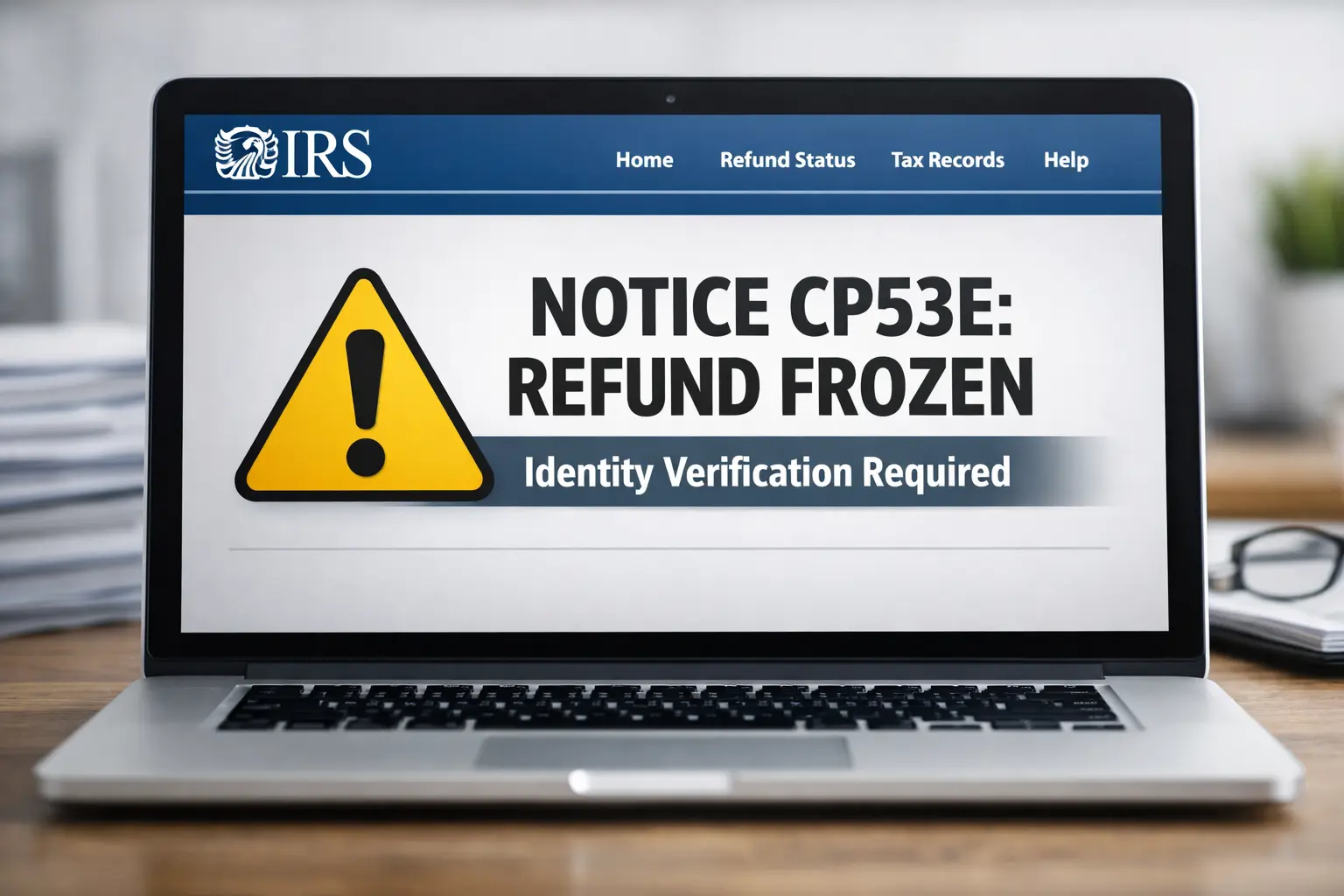

A wave of confusion is hitting households across the United States today March 18 2026 as millions of taxpayers encounter a specific obstacle known as the IRS CP53E notice.

While many were expecting their federal refunds to land in their bank accounts this morning a significant number of direct deposits have been blocked due to new security protocols embedded in the One Big Beautiful Bill Act or OBBBA.

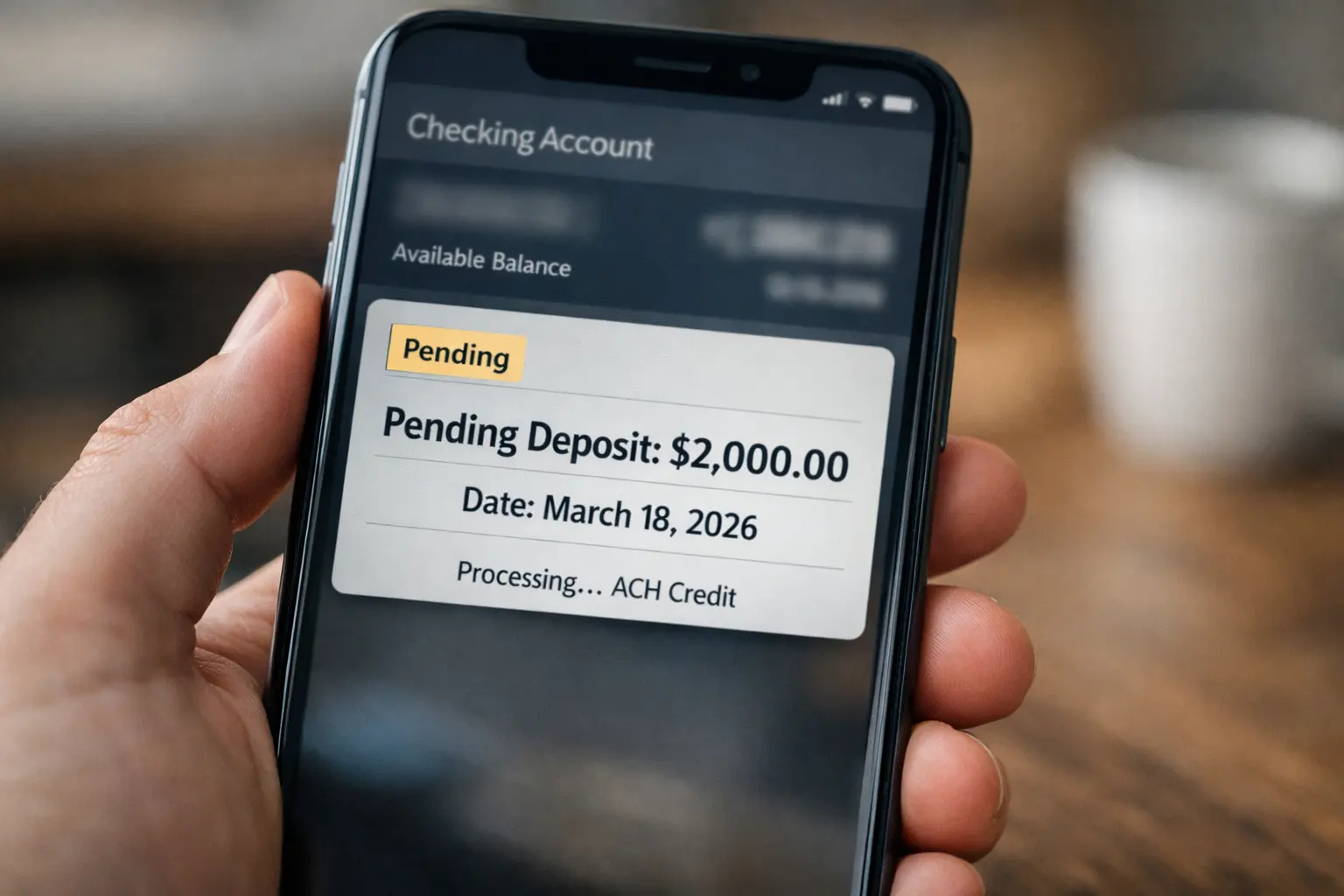

This notice represents a “hard freeze” on funds that were previously marked as sent leaving many with a zero balance when they expected financial relief. If you are seeing a deposit pending status that suddenly disappears without the funds becoming available you are likely facing this new 2026 regulatory hurdle.

Understanding the CP53E Frozen Refund Trigger

The CP53E notice is not a standard letter but a digital and physical red flag that occurs when the federal treasury attempts to send a direct deposit that is subsequently rejected by a financial institution.

In previous tax years a rejected deposit would automatically trigger a paper check sent to the address on file. However under the 2026 tax modernization rules the government has phased out automatic paper check fallback to reduce fraud.

Now when a bank rejects a transfer the funds are pulled back into a federal payment released balance frozen state. The rejection usually happens for three specific reasons. First any mismatch in the name on the tax return versus the name on the bank account will trigger an immediate CP53E freeze.

Second the use of temporary “neo-bank” accounts that do not support the new ISO 20022 messaging standards can cause the us money movement system to flag the transaction as high risk.

Finally if you have moved recently and your bank has an old address on file the identity verification layers of the OBBBA will stop the payout to prevent identity theft.

How to Fix a Frozen Tax Refund Today

The most frustrating aspect of the CP53E warning is that the irs code 846 may still appear on your transcript as if the money was sent. This creates a massive information gap for the taxpayer.

To fix this you must move beyond the standard “Where is my refund” tool which often lags behind real time events. You must log in to your secure IRS online account to check for the digital version of the CP53E notice.

Once you confirm the notice is present the resolution requires a manual “re-link” of your banking credentials. You will need to provide a verified routing number and account number that matches your primary identification exactly.

In some cases you may be required to complete an identity verification through a video call or by providing secondary documentation. Once this is completed the funds are placed back into the next deposit wave clears queue which typically processes every Tuesday and Friday.

The Role of Bank Posting Times and Rejections

It is important to distinguish between a technical delay and a CP53E freeze. If your money is simply pending it likely means your institution is still working through the overnight bank clearing cycles or waiting for the final 1 PM ledger refresh.

However a rejection happens instantly at the gateway level. If you call your bank and they claim they have no record of an incoming transfer while your transcript says the refund was sent you are almost certainly caught in the CP53E net.

Many traditional banks are now using more aggressive filters to comply with the 2026 OBBBA standards. This means that banks control payment posting with much higher scrutiny than in the past.

If your account has been inactive for more than ninety days or if you have a pending garnishment the bank may reject the federal deposit which then triggers the IRS to issue the CP53E freeze for your protection.

Immediate Steps for Affected Taxpayers

If you suspect your refund is frozen today you should avoid waiting for a physical letter to arrive in the mail as this can take up to fourteen days.

Instead take immediate action by verifying your true liquidity available balance and cross referencing it with your federal transcript. If the 846 code is present but the bank denies seeing the file you must prioritize the digital identity verification process.

The modernization of the us money movement system settlement is designed to ensure that the trillions of dollars moved today reach the correct hands. While the CP53E notice causes immediate stress it is a safeguard against the rising tide of digital refund theft.

By following the new 2026 protocols and resolving the notice digitally you can move your funds out of the frozen state and into your spendable balance within the next business cycle.

Investozora will continue to monitor the wednesday federal deposit wave to provide updates on any system wide freezes affecting the public.

Author