It’s 11:57 PM. You refresh your banking app. Midnight hits. Still nothing.

Every single night across the United States, millions of people search the same question: will my direct deposit hit at midnight? Whether it’s payroll deposit timing, a federal direct deposit time from the IRS, or a Social Security payment, the midnight expectation has become almost universal.

And when the money doesn’t appear at 12:00 AM sharp, anxiety kicks in. Search volume spikes for phrases like what time does direct deposit hit, direct deposit time bank, and why direct deposit late. The truth is less dramatic than the fear.

Most direct deposits do not “hit” at midnight. Midnight is largely a psychological checkpoint, not a settlement event. Understanding how ACH batch processing time, overnight clearing cycles, and bank ledger rollover time actually work can remove the stress from that 12:01 AM refresh.

The Midnight Bank Update Myth

The belief that deposits arrive at midnight comes from how some banks display pending activity. In certain systems, transactions appear with a 12:00 AM timestamp, which creates the illusion that midnight is when funds are processed.

In reality, most banks complete their overnight clearing cycles before customers wake up, not at the exact moment the clock flips. The midnight bank update myth persists because customers associate date changes with balance updates. But ACH files do not universally settle at 12:00 AM.

Instead, ACH batch processing time depends on when files were transmitted and when the receiving bank runs its internal posting window. ACH files move in scheduled batch windows governed by NACHA operating rules.

What Time Does Direct Deposit Hit?

When people ask what time does direct deposit hit, they are really asking when funds move from “in process” to “available balance.”

There are three major stages:

First, the originator such as an employer for payroll deposit timing or a federal agency for federal direct deposit time, submits the payment file. That submission is governed by the ACH cutoff timing. If the file misses the daily cutoff, it shifts to the next business day.

Second, the Automated Clearing House network processes and settles those files during designated windows. This is where people search when does ACH settle and why timing matters.

Third, the receiving bank performs internal bank reserve verification, ledger updates, and fraud screening. Only after that does the deposit appear as available funds. For many institutions, this final 6AM vs 9AM posting occurs between 6 AM and 9 AM local time, not midnight.

ACH Cutoff Time Today and Why It Matters

One of the most misunderstood elements of direct deposit timing is the ACH cutoff timing. If an employer submits payroll after the cutoff, the file does not enter that day’s settlement window.

If your employer submits payroll at 4:58 PM and the cutoff is 5:00 PM, you’re fine. If they submit at 5:02 PM, settlement shifts a full business day.

This explains why payroll deposit timing can shift by a full day. If your employer submits the file at 5:15 PM and the cutoff was 5:00 PM, your funds may settle the following business day. That delay is not a system failure; it is how ACH scheduling works.

Searches for direct deposit Friday timing increase when paydays fall on Fridays, because the interaction between ACH batch processing time and weekend schedules changes expectations.

Overnight Clearing Cycle and Early Morning Deposits

The overnight clearing cycles are where most direct deposits actually move. ACH files transmitted during the day are processed in batches and delivered to banks overnight. However, delivery to the bank does not automatically equal posting to your balance.

Banks operate internal systems that complete ledger rollover time, a recalibration process that resets accounts for the new business day. This process may happen around midnight, but the visible balance update often occurs hours later.

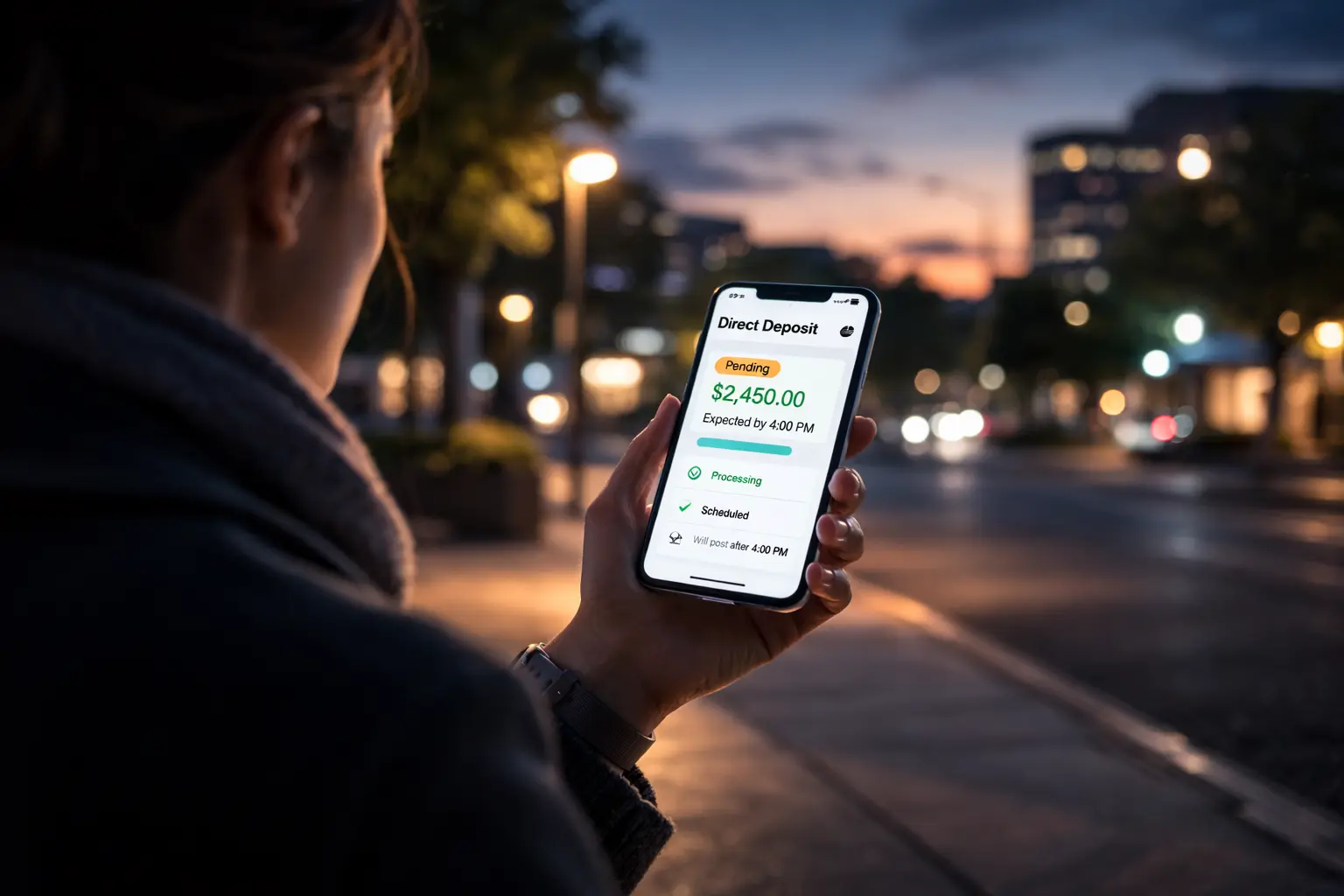

That’s why people who search does direct deposit hit early morning often see funds appear at 6:12 AM, 7:03 AM, or 8:47 AM rather than 12:00 AM, as detailed in our settlement timeline.

Settlement vs Posting: The Critical Difference

One of the biggest sources of confusion is settlement vs posting. Settlement refers to the interbank transfer confirmation within the ACH network. Posting refers to when your specific bank credits your account.

Funds can settle within the ACH system before your bank chooses to post them. This is especially true during high-volume weeks when federal direct deposit time overlaps with payroll file processing.

If you see a pending before clearing indicator in your banking app, it often signals that the ACH file has been received but is still inside internal processing. Understanding this distinction eliminates much of the midnight anxiety.

Why Direct Deposit Is Late (Or Feels Late)

Searches for why direct deposit late trend every Thursday night and Friday morning. In most cases, the deposit is not late in a systemic sense. It is simply aligned with the bank’s standard posting cycle.

Differences between institutions also matter. Some online banks front funds earlier because of risk models that assume incoming settlement. Traditional banks may wait until bank reserve verification completes before making funds available.

This explains why banks post differently; two employees at the same company, with identical payroll deposit timing, can receive funds at different hours.

Federal Direct Deposit Time vs Payroll Timing

Federal direct deposit time, including IRS refunds, Social Security, and other Treasury Department payments, follows a structured release schedule. But once the funds enter ACH batch processing time, the receiving bank determines visibility.

Payroll deposit timing depends on employer submission behavior and ACH cutoff timing. Federal payments depend on Treasury release timing. In both cases, the midnight expectation is misplaced.

Direct deposit Friday timing often results in early morning crediting rather than midnight posting because banks concentrate volume processing during morning windows.

Bank Posting Time 2026: What Has Changed?

In 2026, banking systems are faster, but they are not universally real-time for ACH deposits. While same-day ACH has expanded, most recurring payroll and federal deposits still follow scheduled batch cycles within the US money movement landscape.

The evolution of bank posting time 2026 reflects improved efficiency, but not the elimination of overnight clearing cycles mechanics. That means the pattern remains consistent: funds move overnight, appear in the early morning, and rarely post exactly at midnight.

When Should You Be Concerned?

If your direct deposit has not appeared by mid-morning on the official payment date, it may be appropriate to check with your bank. If the ACH cutoff time today was missed or if there was an account issue, delays can occur.

However, if you are refreshing your app at 12:03 AM and searching will my direct deposit hit at midnight, the absence of funds at that moment is usually normal. The system is working. It just does not align with the midnight expectation.

The Bottom Line

Midnight is a psychological milestone, not a financial one. Direct deposit time bank policies, ACH batch processing time, and overnight clearing cycles mechanics determine when money becomes visible.

Most deposits post between 6 AM and 9 AM, after settlement vs posting steps complete and bank reserve verification finalizes. If your deposit does not appear at 12:00 AM, that does not mean it is late. It means your bank’s posting window has not yet opened.

In a system processing millions of transactions every night, timing differences are standard, and understanding that truth removes the stress from the 12:01 AM update, the pending tonight check, or realizing the deposit not there.

Author