You own a home. You have a 401(k). Your Net Worth is higher than ever. So why are you terrified of a $500 car repair? Welcome to The Illiquidity Trap.

There is a dangerous optical illusion in modern personal finance. If you look at the balance sheet of the average American household, things look robust.

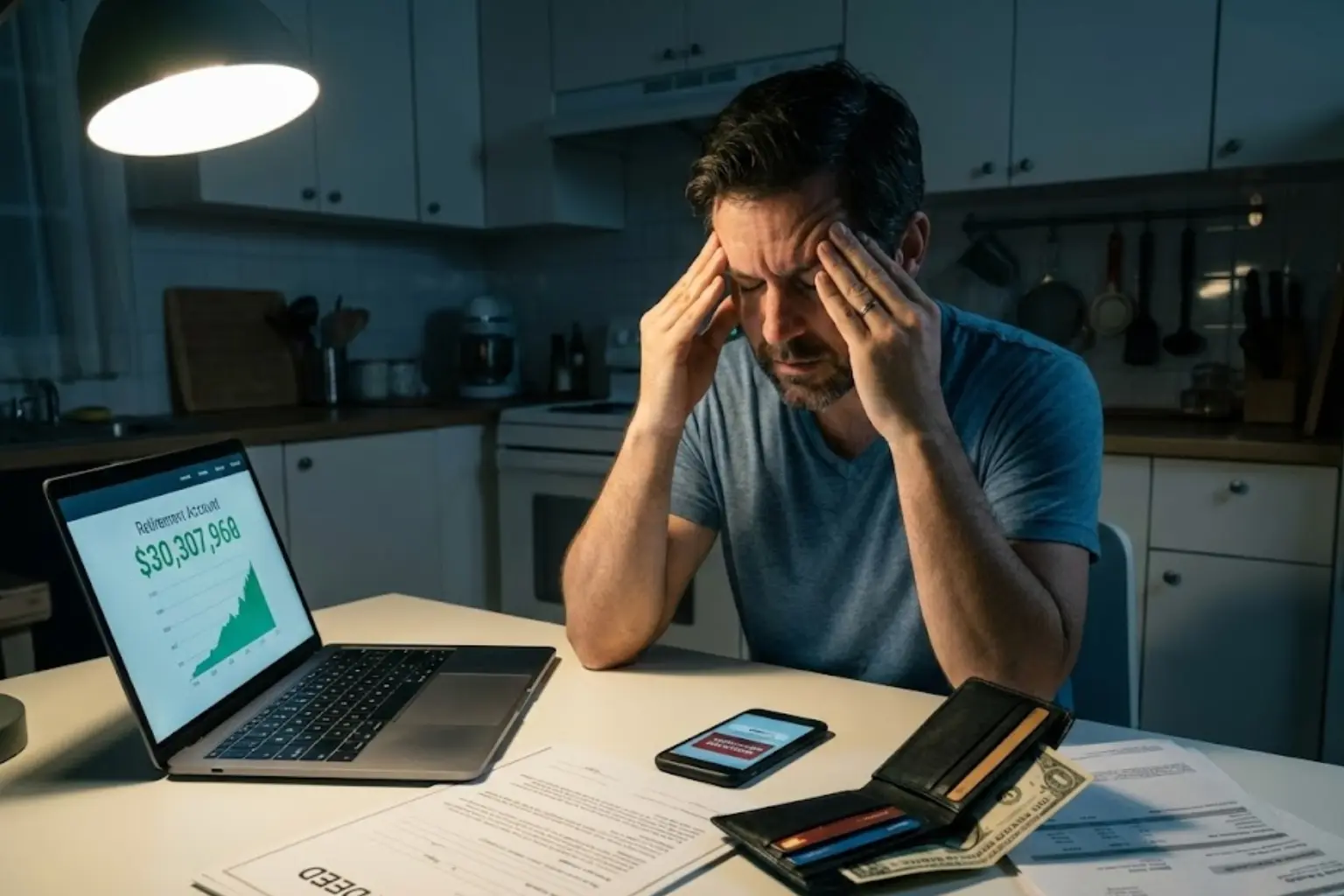

Home values are up. Retirement accounts have compounded. On paper, the middle class appears wealthy. But you cannot buy groceries with Home Equity. You cannot pay the electric bill with Unrealized Gains.

In the real economy of 2026, Solvency what you own has detached from Liquidity what you can spend. While we focused on building Wealth for the long term, we neglected cash flow for the short term.

The result? A generation of high-earners who are technically millionaires, yet are living paycheck-to-paycheck, using credit cards to bridge the gap between their assets and their bills.

Here is why your money is trapped behind a wall of penalties and interest rates, and why cash flow is the only metric that matters in the great downgrade.

- The Paper Tiger Wealth: The bulk of middle-class wealth is locked in illiquid assets like real estate and retirement accounts that cannot be accessed without massive penalties or taxes, leaving daily life financially vulnerable.

- The Cash Flow Squeeze: While assets grew, liquid disposable income collapsed due to the hollow raise and rising fixed costs, creating a cash crunch despite high salaries.

- The Debt Bridge: To survive the liquidity gap, households are using phantom debt as a fake checking account, paying interest just to access basic spending power.

- The New Safety Net: In an illiquid world, the emergency fund amount is no longer just for emergencies; it has become the operational capital required to prevent insolvency.

The Locked Vault of Wealth

The primary driver of the Illiquidity Trap is that our assets have become prisons. Decades of financial advice told us to dump everything into two buckets: The Home and The 401(k). In 2026, both are traps.

The Housing Trap: As we explored in the rent vs buy analysis, homeowners are sitting on record equity. But with interest rates remaining elevated, you cannot access that money via a HELOC without doubling your monthly payment. Your wealth is stuck in the drywall.

The Retirement Trap: Your average retirement savings by age might look healthy, but that money is legally fenced off. Touching it triggers a 10% penalty and immediate taxation.

The Result: You are Rich in the future, but Poor today. You have a mountain of gold that you can’t touch, while you struggle to pay for the Service Downgrade of modern life.

The Solvency Liquidity Gap: The Asset-Rich, Cash-Poor Index 2026

This analysis highlights the widening disparity between household Net Worth and actual Spendable Cash. While balance sheets reflect record-high equity due to asset inflation, the daily operational reality reveals a structural liquidity crisis where families are technically wealthy but operationally insolvent.

| Financial Metric | The Paper Reality (Net Worth) | The Tuesday Reality (Liquidity) | The Trap Mechanism |

|---|---|---|---|

| Home Equity | Record Highs (+40% since 2020) | Zero Access | High interest rates make HELOCs and refinancing too costly to unlock usable cash. |

| Retirement | Compounding (Stock Market) | -30% Value | Early withdrawal penalties and taxes make retirement funds unusable during emergencies. |

| Income | Six Figures (Nominal) | Negative Flow | The hollow raise and rising fixed costs consume nearly all take-home pay. |

| Spending Power | High Credit Limits | Debt Trap | Purchasing power is driven by 25% APR credit cards, not by available cash. |

| Savings Status | “Wealthy” | “Insolvent” | Can survive retirement planning, but cannot survive a car insurance deductible or unexpected bill. |

Source: Investozora Market Analysis 2026, synthesizing data from the Federal Reserve (Flow of Funds Z.1) regarding household equity and FDIC banking data on liquid deposit trends.

The Collapse of Free Cash

While your assets are locked up, your liquid cash is under siege. The January paycheck drop highlighted how taxes and benefit costs are intercepting money before it hits your bank account. But the squeeze continues after the deposit.

The Escrow Shock: For homeowners, the mortgage escrow shortage has siphoned off hundreds of dollars of monthly liquidity to pay for insurance spikes.

The Subscription Tax: The great detachment of the economy has shifted costs to monthly recurring models. You don’t own movies; you rent streaming. You don’t own software; you lease it.

This raises your burn rate the minimum amount of cash needed just to wake up in the morning. Even high earners are finding that after the fixed cost harvest, their discretionary seed corn is gone.

Credit as Fake Liquidity

When you have Assets but no Cash, you turn to the only liquidity available: Debt. This explains the confusing data in our credit card debt January report. People aren’t using credit cards because they are irresponsible shopaholics. They are using credit cards because they are illiquid.

They are using the card to pay for groceries on Tuesday because the paycheck doesn’t arrive until Friday. And they are using phantom debt Buy Now, Pay Later to smooth out cash flow spikes.

The Trap: This creates a Negative Carry. You are paying 24% APR to borrow liquidity, effectively eroding the wealth you are building in your locked accounts. You are paying interest to access your own lifestyle.

Breaking the Trap: The Liquid First Strategy

Escaping the Illiquidity Trap requires a fundamental shift in how you view money. You must stop optimizing for net worth a vanity metric and start optimizing for Liquidity a survival metric.

Pause the Aggressive Paydown: If you are aggressively paying down a 3% mortgage while you have $0 in the bank, stop. You are trapping liquid cash in an illiquid wall.

Supercharge the Buffer: The old rules don’t apply. As we stated in our emergency fund amount guide, you need 3-6 months of liquid cash in a High Yield Savings Account, not a CD, not a Bond. It must be accessible instantly.

Perform a Liquidity Audit: Use the Sunday money reset to map your cash conversion cycle. Know exactly when bills hit versus when income hits.

The Bottom Line

In 2026, Cash is not trash. Cash is Oxygen. Do not let the financial industry shame you into locking up every cent for a retirement that is 30 years away while you suffocate today.

The goal of the 50/30/20 budget wasn’t just to save; it was to keep you operationally sound. Reclaim your liquidity. Because being Rich on Paper doesn’t matter if you can’t pay for the present.

Methodology

This article analyzes the liquidity premium in household finance by contrasting Federal Reserve Z.1 Financial Accounts Net Worth data against Bureau of Economic Analysis (BEA) Personal Saving Rates.

It incorporates current banking interest rate environments to evaluate the cost of accessing liquidity via credit versus the opportunity cost of holding liquid cash, defining the modern Illiquidity Trap.

Investozora uses only trusted, verified sources. We focus on white papers, government sites, original data, firsthand reporting, and interviews with respected industry experts. When relevant, we also use research from reputable publishers. Every fact is checked against a primary source so readers get clear, accurate, and up-to-date information, and we update our citations whenever official guidance changes.

- Federal Reserve — Financial Accounts of the United States (Z.1) – Comprehensive Flow of Funds data detailing household balance sheets, asset allocation, liabilities, and liquidity trends.

- FDIC — Quarterly Banking Profile – Official FDIC analysis of U.S. banking conditions, deposit behavior, liquidity, and systemic risk indicators.

Frequently Asked Questions

Author