Last Updated: November 11, 2025

Why Life Insurance Matters in 2025

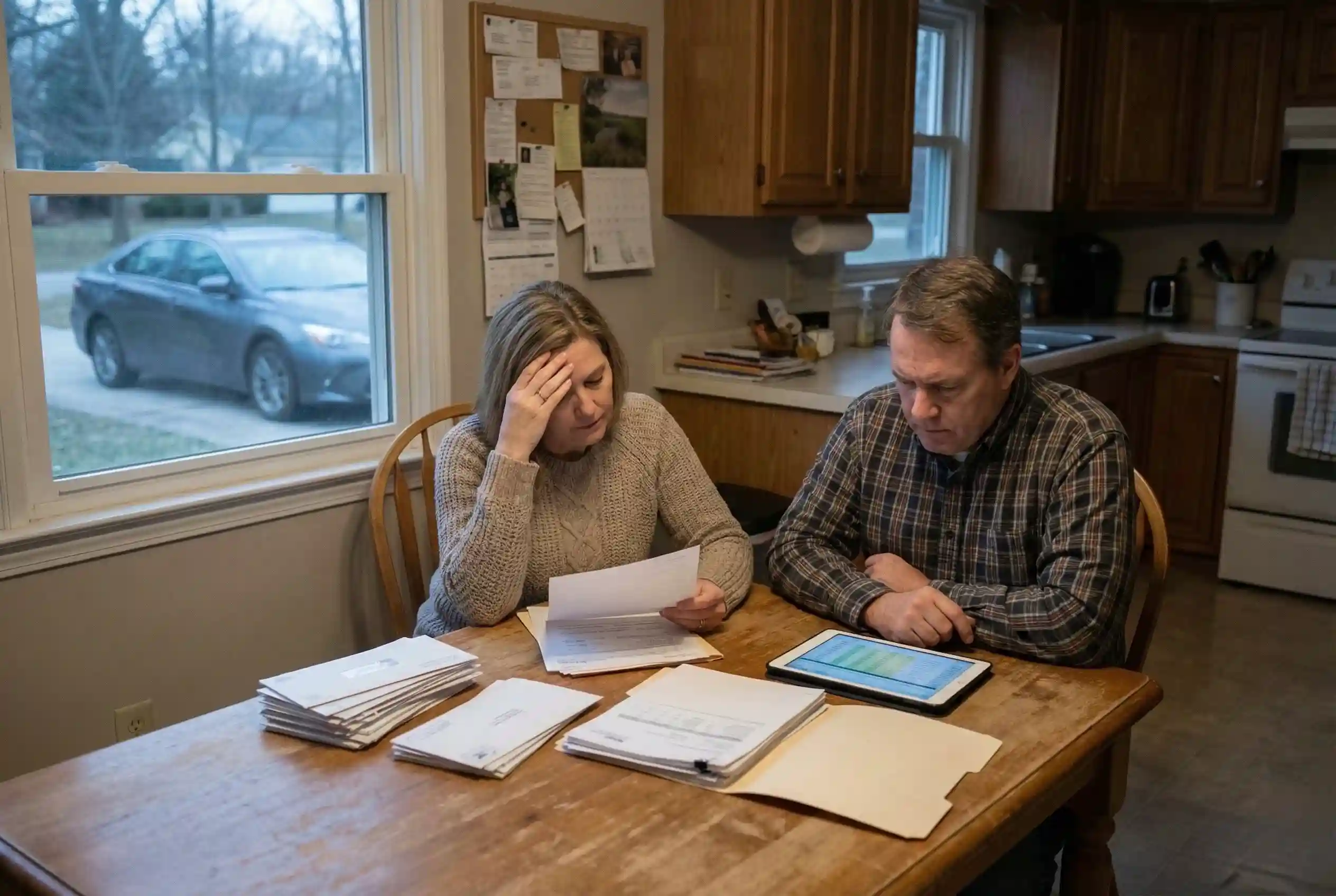

Life insurance policies have become more than just a safety net for families they’re now an essential tool for financial planning in 2025. Rising costs of living, uncertain economic cycles, and higher healthcare expenses are pushing more U.S. households to secure affordable protection. Having the right coverage ensures that loved ones can maintain financial stability even if unexpected events occur. For many families balancing savings in high-yield accounts with insurance coverage, this balance between liquidity and protection is crucial.

Another reason life insurance policies are gaining attention is the shift in generational priorities. Younger adults, including Gen Z professionals, are beginning to view insurance not just as protection but as part of an overall wealth-building strategy. Similar to how many start with student credit cards to establish credit, they’re also seeking life insurance earlier to lock in lower premiums. Federal resources such as the official guide emphasize that starting young provides long-term cost advantages and wider policy options.

The growth in demand also reflects rising awareness of policy diversity from term coverage to permanent plans with investment components. While retirement-focused tools like tax-free investment strategies help build wealth, life insurance adds a layer of guaranteed protection. The FTC’s consumer guide reminds buyers that comparing multiple insurers and understanding state protections is key to avoiding costly mistakes. In 2025, life insurance policies are no longer optional they are a cornerstone of a responsible financial plan.

What Is Life Insurance?

At its core, life insurance is a contract between you and an insurer, designed to provide financial protection for your beneficiaries after your passing. With life insurance policies, the insurer promises a payout called the death benefit so your loved ones can cover expenses like housing, education, or debts. Unlike a checking account, which focuses on daily money management, life insurance exists to ensure long-term security when income support disappears unexpectedly.

Life insurance policies in the U.S. work under clear federal and state guidelines. After paying regular premiums, policyholders maintain coverage, and when a claim is filed, the insurer disburses the agreed benefit. The state insurance offices provide oversight to ensure that companies meet obligations and protect consumers. According to the IRS rules, most life insurance payouts are not taxable, which makes them one of the most efficient financial safeguards available for American households.

It’s also important to see how life insurance compares with other protections. Health coverage manages medical costs, while umbrella insurance extends liability protection. Life insurance policies, however, are uniquely designed to provide a guaranteed payout to heirs, regardless of market conditions. This makes them different from investment accounts, which fluctuate in value. In short, life insurance stands apart by offering certainty an assurance that families won’t be left vulnerable during life’s most unpredictable moments.

Why Do You Need Life Insurance?

One of the strongest reasons why get life insurance is to protect your family’s lifestyle when you’re no longer there to provide income. Life insurance policies give dependents the ability to cover daily expenses such as housing, food, and education without financial disruption. Parents often combine policies with student accounts or student credit cards to ensure children can continue school even if the primary earner passes away. The official federal guide also stresses that coverage decisions should reflect the true cost of raising a family, not just short-term bills.

Another major benefit of life insurance USA households rely on is debt protection. If you carry a mortgage, car loan, or private student loan, your family could inherit that burden. With life insurance policies, beneficiaries can settle these balances without sacrificing their savings or emergency funds. This becomes especially important when paired with other financial tools like high-yield savings or tax-free investment strategies, since it prevents loved ones from having to liquidate assets at the wrong time. The FTC’s consumer advice also reminds borrowers that insurance plays a role in preventing creditors from disrupting household finances.

Life insurance policies also extend far beyond family coverage. Entrepreneurs often use them as a business continuity tool, ensuring partners can buy out shares or keep operations running. Estate planning is another critical use wealthy households pair life insurance with retirement strategies to balance taxes and inheritance.

Types of Life Insurance Policies in the U.S.

Term Life Insurance

Term life insurance is the simplest and most affordable option among all types of life insurance policies. It provides coverage for a fixed period typically 10, 20, or 30 years. If the policyholder passes away during the term, the insurer pays the death benefit to beneficiaries. If the term expires, coverage ends unless renewed, usually at a higher premium.

Families choose term life to protect specific financial obligations, such as mortgages, education costs, or income replacement during peak earning years. It’s straightforward, with no cash value or investment features just pure protection. This makes it a strong fit for young professionals balancing student accounts or starting families.

The Texas insurance guide explains that term coverage is especially effective for temporary needs, like paying off a 30-year mortgage. Because premiums are lower than permanent policies, buyers can secure high coverage amounts at affordable rates.

Key Features of Term Life Insurance:

- Provides coverage for a fixed term (10–30 years).

- Affordable premiums compared to permanent policies.

- No cash value accumulation pure protection only.

- Suitable for income replacement, mortgage protection, and family security.

- Can be converted to permanent coverage in some cases.

Whole Life Insurance

Whole life insurance is a permanent policy that provides coverage for your entire lifetime, as long as premiums are paid. Unlike term coverage, it never expires, and it builds a cash value component that grows at a guaranteed rate. This makes whole life one of the most reliable types of life insurance policies for long-term planning.

Premiums are higher than term insurance, but they remain level for life, offering predictability. The cash value grows tax-deferred and can be borrowed against or withdrawn if needed, although loans reduce the final death benefit. Families often combine whole life with retirement strategies to ensure both protection and a financial safety net.

The Pennsylvania insurance office highlights that whole life insurance is especially effective for estate planning and wealth transfer. High-net-worth individuals use these policies to leave tax-advantaged inheritances, while parents may use them to provide lifelong protection for dependents.

Key Features of Whole Life Insurance:

- Permanent coverage: lasts a lifetime if premiums are paid.

- Level premiums: payments stay the same over time.

- Cash value: grows tax-deferred and available for loans or withdrawals.

- Guarantees: both death benefit and cash value growth are predictable.

- Useful for estate planning, wealth transfer, and long-term security.

Whole life insurance works best for those who want stability, predictable costs, and a guaranteed financial legacy alongside lifelong coverage.

Universal Life Insurance

Universal life insurance is a flexible type of permanent coverage that allows policyholders to adjust both their premiums and death benefits over time. Unlike whole life, it doesn’t lock you into fixed payments. As long as the policy has enough cash value to cover the cost of insurance, you can reduce or increase contributions when your financial situation changes.

The cash value in universal life earns interest, often tied to market rates. Extra premium payments build this value, which can later offset premiums or boost benefits. Many business owners or families with variable incomes choose universal life insurance policies because it adapts to their changing needs. It also serves as a useful tool for tax planning, especially in managing estate obligations.

The Utah buyer’s guide explains that universal life policies are designed for long-term commitments while offering flexibility that term or whole life may lack. This makes them appealing to policyholders who want lifelong protection but prefer to control how and when they contribute.

Key Features of Universal Life Insurance:

- Permanent coverage with flexible premiums and benefits.

- Cash value earns interest and grows tax-deferred.

- Policyholders can adjust payments depending on financial situation.

- Allows access to cash value for loans or withdrawals.

- Works well for estate planning, high earners, and business continuity.

Universal life insurance is best suited for people seeking lifelong coverage that can adapt as their financial needs evolve.

Variable Life Insurance

Variable life insurance is a permanent policy that combines life insurance protection with investment opportunities. In addition to providing a guaranteed death benefit, the policyholder can invest the cash value in sub-accounts similar to mutual funds. These may include stocks, bonds, or balanced portfolios. Because of this structure, the value of the policy can rise or fall depending on market performance.

This type of policy appeals to individuals comfortable with investment risk who want growth potential inside their insurance plan. Unlike high-yield savings, where returns are steady but limited, variable life can deliver higher gains if markets perform well. On the other hand, poor performance can reduce the cash value and, in extreme cases, impact the policy’s stability.

The New York DFS regulates these products closely, requiring insurers to provide clear disclosures about risks and fees. Policyholders must be actively involved in monitoring their investments, making this type of life insurance more complex than term or whole life.

Key Features of Variable Life Insurance:

- Permanent coverage with a guaranteed death benefit.

- Cash value invested in sub-accounts (stocks, bonds, mutual funds).

- Policy performance depends on market results.

- Higher growth potential than traditional policies, but more risk.

- Regulated by state insurance offices for consumer protection.

Variable life insurance is best for financially savvy buyers who want both lifelong protection and the chance to grow wealth through market-linked investments.

Indexed Universal Life Insurance

Indexed universal life insurance (IUL) is a permanent policy that blends flexible coverage with growth potential tied to a market index. Instead of earning a fixed interest rate, the cash value grows based on the performance of an index like the S&P 500. Returns are capped at a maximum percentage, but they never drop below zero, which protects policyholders from market losses.

This type of policy works well for people who want moderate growth without directly investing in risky markets. It offers more upside than traditional whole life and less volatility than variable life. Buyers often combine IUL policies with robo-advisors or other investment strategies to balance safety and growth.

The California Department of Insurance notes that indexed policies have gained popularity because they provide both flexibility and market participation. Premiums and benefits can be adjusted, making them practical for professionals and families with changing financial priorities.

Key Features of Indexed Universal Life Insurance:

- Permanent coverage with flexible premiums and adjustable death benefits.

- Cash value linked to an equity index, such as the S&P 500.

- Returns capped at a maximum rate but protected from losses.

- Offers more growth than whole life, less risk than variable life.

- Useful for long-term planning, wealth building, and estate strategies.

Indexed universal life insurance appeals to those seeking steady lifetime protection with potential for higher returns than traditional policies.

Guaranteed Issue Life Insurance

Guaranteed issue life insurance is a type of permanent coverage designed for people who may not qualify for traditional policies due to health issues or age. It requires no medical exam and very limited health questions, making it one of the most accessible types of life insurance policies. Because the risk for insurers is higher, premiums are more expensive, and coverage amounts are usually smaller—often just enough to cover funeral costs, medical bills, or other final expenses.

This type of policy is most common among seniors or individuals with chronic conditions who want to ensure loved ones are not left with financial burdens. Families often compare guaranteed issue with no medical exam insurance to see which option offers the best balance of affordability and coverage.

The North Dakota Insurance Department explains that guaranteed issue plans provide valuable coverage for underserved groups who might otherwise be uninsured. While the death benefit may be modest, it ensures that beneficiaries can manage end-of-life costs without dipping into savings or emergency funds.

Key Features of Guaranteed Issue Life Insurance:

- Permanent coverage with no medical exam required.

- Higher premiums compared to traditional policies.

- Lower coverage amounts, often $5,000–$25,000.

- Designed to cover funeral costs, debts, and final expenses.

- Available to seniors and people with health challenges.

Guaranteed issue life insurance provides peace of mind for families by ensuring basic financial protection, even for those considered high-risk by insurers.

What Is Term Life Insurance?

Term life insurance is the most straightforward form of protection in the U.S. insurance market. It covers a person for a fixed number of years commonly 10, 20, or 30. If the insured dies during that period, their beneficiaries receive a lump-sum payment, known as the death benefit. If the policy term ends and the individual is still alive, the coverage simply stops.

Unlike permanent products such as whole life insurance, term life does not build cash value. Its sole purpose is financial protection. That’s why premiums are significantly cheaper compared to permanent policies. For many families balancing mortgage payments, student loans, and day-to-day expenses, this affordability makes term life the entry point to coverage.

For instance, a 30-year-old parent may purchase a 20-year term policy to cover their children until they graduate college. If something happens to the parent within that period, the payout ensures tuition and household bills are covered. This makes term life one of the most practical types of life insurance policies for young professionals and families in 2025. The Texas Department of Insurance highlights it as an ideal option for families seeking “maximum protection with minimum cost.”

Pros and Cons of Term Life Insurance

While term life offers many advantages, it also comes with some limitations. Understanding both sides helps buyers make better decisions.

Advantages:

- Affordability: Young buyers often secure $500,000 or more in coverage for less than $25 per month.

- Flexibility: Available in different terms (10, 15, 20, 30 years), which can be matched to specific debts like mortgages.

- Simplicity: No complex investment features; only pure financial protection.

- Conversion options: Some insurers allow conversion to whole life or universal life without a medical exam.

Drawbacks:

- Temporary protection: Once the term ends, coverage stops, leaving families without benefits unless renewed.

- Higher renewal costs: Premiums increase sharply with age, often making renewal unaffordable.

- No cash value: Unlike investment accounts, term policies don’t build savings.

This structure makes term life ideal for temporary needs, but not for those seeking lifelong guarantees or cash accumulation.

Average Term Life Insurance Quotes in 2025 (Cost by Age & Gender)

Insurance costs are based on factors like age, gender, health, smoking status, and coverage amount. In general, women pay less than men because of longer life expectancy. Buying early locks in significantly cheaper rates, while waiting until your 50s or 60s can make premiums steep.

Sample Monthly Premiums (20-Year Term, $500,000 Coverage, Non-Smoker, 2025)

| Age | Male (Monthly) | Female (Monthly) |

|---|---|---|

| 25 | $18 – $22 | $15 – $19 |

| 30 | $22 – $26 | $18 – $23 |

| 40 | $33 – $41 | $28 – $35 |

| 50 | $78 – $95 | $65 – $80 |

| 60 | $190 – $230 | $155 – $200 |

Example: A 25-year-old woman buying a $500,000 policy pays around $16 monthly—less than most high-yield savings account contributions. But by age 50, that same policy could cost more than $80 monthly. According to the Utah life insurance buyer’s guide, purchasing early ensures decades of affordable security.

Best Term Life Insurance Companies in the U.S.

Choosing the right insurer matters as much as the policy itself. The best companies combine financial strength, affordable premiums, good customer service, and flexible conversion options.

Top Providers in 2025:

- New York Life: Oldest U.S. insurer, A++ rating, strong financial stability. Great for long-term conversions.

- Northwestern Mutual: Offers flexible term-to-whole conversion, highly rated customer service.

- Haven Life: Tech-driven, backed by MassMutual, known for instant online applications.

- State Farm: Local agent support, flexible riders, and wide availability.

- Guardian Life: Trusted for estate planning and family protection.

Special groups also have unique access:

- Military Families: VA life insurance programs like SGLI and VGLI provide tailored, affordable term options.

- Federal Employees: FEGLI gives access to group term coverage at competitive rates.

When shopping, the California Department of Insurance recommends comparing at least three quotes and checking financial ratings before finalizing. Policyholders can also use state policy locators if they lose track of coverage.

Real-World Example: Family Mortgage Protection

Consider a couple in their 30s with a $300,000, 30-year mortgage. They purchase a 30-year term life policy matching the loan length. If either spouse passes away during the loan period, the death benefit pays off the mortgage entirely, ensuring the family home is secure. This shows why term life is often seen as the best bridge between affordability and protection.

What Is Whole Life Insurance?

Whole life insurance is a permanent policy that provides lifelong coverage as long as premiums are paid. Unlike term life, which expires after a set number of years, whole life guarantees a death benefit no matter when the policyholder passes away. One of its defining features is the cash value component, which grows at a fixed, tax-deferred rate. This means the policy functions both as insurance and a conservative savings vehicle.

Premiums are higher than term life but remain level for the lifetime of the policy. Over time, the growing cash value can be borrowed against or withdrawn, offering policyholders a source of liquidity. For families seeking stability, many use whole life alongside retirement strategies to balance guaranteed protection with asset-building.

According to the Pennsylvania Insurance Department, whole life insurance is particularly effective for estate planning and wealth transfer. This makes it attractive to high-net-worth individuals who want to leave a tax-efficient legacy to heirs.

Pros and Cons of Whole Life Insurance

Whole life has unique strengths but also clear drawbacks compared to other types of life insurance policies.

Advantages:

- Lifelong coverage: The policy never expires as long as premiums are paid.

- Level premiums: Payments remain consistent for life.

- Cash value growth: Builds guaranteed savings over time.

- Tax-deferred benefits: Cash value grows without annual tax obligations.

- Estate planning tool: Helps transfer wealth across generations.

Disadvantages:

- Higher cost: Premiums are significantly more expensive than term life.

- Lower returns: Cash value grows slowly compared to investment accounts.

- Less flexibility: Cannot easily adjust death benefit or premium payments.

- Loan impact: Borrowing against cash value reduces the final payout.

This balance shows why whole life is best suited for individuals who value stability and guaranteed benefits more than low-cost, temporary coverage.

Whole Life Insurance as an Investment: Is It Worth It?

Whole life is often marketed as both insurance and investment, but whether it’s “worth it” depends on financial goals. The cash value grows at a predictable rate usually 2% to 4% annually. While this is safer than market-based robo-advisors, it is less lucrative over decades.

For example, someone paying $500 monthly into whole life might see modest cash accumulation compared to investing the same amount in mutual funds or retirement accounts. However, the guaranteed growth, combined with a lifelong death benefit, provides stability that market investments cannot.

The IRS notes that policy loans are tax-free as long as the policy remains active, making whole life a potential tool for liquidity in retirement. Still, consumer experts and the FTC warn that buyers should carefully compare costs versus alternatives like term coverage plus outside investing.

Whole life is most beneficial for:

- High-net-worth families seeking estate planning tools.

- Parents wanting lifelong coverage for dependents.

- Individuals who value guaranteed growth over market volatility.

Best Whole Life Insurance Companies in 2025

The best providers of whole life insurance combine financial stability, strong dividend histories, and flexible rider options. In 2025, these insurers stand out:

- MassMutual: Known for strong dividend performance, flexible policies, and high financial strength ratings.

- New York Life: Oldest mutual insurer in the U.S., offers customizable whole life with conversion options.

- Northwestern Mutual: Excellent reputation for policyholder dividends and estate planning support.

- Guardian Life: Offers whole life policies with long-term flexibility and loan options.

- State Farm: Strong service model, accessible for families seeking local agent guidance.

For government employees, the FEGLI program provides additional group coverage options, though it is structured differently than private whole life. State-specific guidance, like the California Insurance Department, also helps consumers understand their options.

Real-World Example: Estate Planning with Whole Life

Consider a 55-year-old professional with significant assets who wants to ensure their children inherit wealth without tax burdens. By purchasing a $1 million whole life policy, they guarantee both a death benefit and a cash value reserve. Combined with tax-free investment strategies, this approach ensures heirs receive both liquid funds and long-term security.

What Is Universal Life Insurance?

Universal life insurance is a permanent policy that blends lifelong coverage with flexibility. Unlike whole life, which locks in fixed premiums, universal life allows policyholders to adjust both premiums and death benefits. If a family’s income fluctuates, payments can be increased, reduced, or even skipped, as long as the cash value is sufficient to cover costs.

The cash value grows tax-deferred, earning interest linked to market rates. This flexibility makes universal life attractive to business owners or high-income earners who need adaptable coverage. It’s also used in estate planning, alongside tax minimization strategies.

According to the Utah buyer’s guide, universal life policies help balance long-term commitments with adaptability. However, the cost of insurance may rise with age, requiring policyholders to manage contributions carefully.

Key Features:

- Permanent coverage with adjustable premiums and benefits.

- Cash value grows at interest rates tied to market benchmarks.

- Allows loans and withdrawals from accumulated cash value.

- Works well for estate planning and high earners needing flexibility.

Variable Life Insurance Explained

Variable life insurance is another permanent product, but instead of earning fixed interest, the cash value is invested in sub-accounts similar to mutual funds. Policyholders can choose portfolios of stocks, bonds, or balanced funds. This introduces higher risk but also higher growth potential compared to traditional savings accounts.

Because market performance directly impacts the policy, variable life is best for financially savvy individuals. A strong investment period can grow both cash value and death benefit, but a downturn can reduce them. The New York DFS regulates these products, ensuring consumers receive detailed disclosures on risk.

Key Features:

- Permanent coverage with guaranteed death benefit.

- Cash value invested in market-based sub-accounts.

- High growth potential but with significant investment risk.

- Suitable for investors comfortable with market volatility.

Indexed Universal Life (IUL) Insurance Pros & Cons

Indexed Universal Life (IUL) combines the flexibility of universal life with growth linked to a stock market index, such as the S&P 500. Instead of direct investments, the cash value earns interest tied to index performance. Returns are capped at a maximum rate but never fall below zero, protecting against losses.

This balance makes IUL popular among moderate-risk buyers who want some market upside without full exposure. Families often pair IUL with robo-advisors for broader diversification. The California Insurance Department highlights IUL as a product that blends safety with growth, though caps limit high returns.

Pros:

- Flexible premiums and death benefits.

- Potential for higher returns than whole life.

- Downside protection never loses cash value in negative markets.

Cons:

- Returns capped, limiting long-term growth.

- More complex than term or whole life.

- Fees can reduce overall returns.

Guaranteed Issue & Final Expense Insurance for Seniors

Guaranteed issue life insurance is designed for seniors or individuals with health issues who may not qualify for traditional policies. It requires no medical exam and minimal health questions. Premiums are higher, and coverage amounts are small usually between $5,000 and $25,000. These policies are often used to cover funeral costs, debts, or final expenses.

Many seniors compare guaranteed issue with no-medical-exam insurance to see which is more affordable. The North Dakota Insurance Department emphasizes that while coverage is modest, it provides peace of mind for families who want to avoid financial burdens at the end of life.

Key Features:

- Permanent coverage with no health requirements.

- Higher premiums than traditional policies.

- Lower coverage amounts, focused on final expenses.

- Accessible for seniors or high-risk applicants.

Real-World Example: Senior Coverage Planning

Consider a 72-year-old retiree in Pennsylvania with heart issues. Traditional insurers may deny coverage, but a guaranteed issue policy offers $15,000 in protection. This ensures funeral and medical costs are covered, sparing family members from dipping into savings or retirement accounts.

Term vs. Whole Life Insurance: Which Is Better?

Cost Comparisons with Examples

When comparing term vs whole life insurance USA, the biggest difference is cost. Term life offers affordable coverage for a set period, while whole life provides lifetime protection with a savings component.

For example, a 30-year-old non-smoker seeking $500,000 in coverage pays around $22 per month for a 20-year term policy, but about $350–$400 monthly for a whole life policy. That’s nearly 15 times higher, reflecting the cash value and guaranteed lifelong coverage whole life provides.

Here’s a 2025 cost snapshot for a $500,000 policy

| Age | 20-Year Term (Monthly) | Whole Life (Monthly) |

|---|---|---|

| 25 | $18 – $22 | $300 – $350 |

| 35 | $25 – $30 | $400 – $450 |

| 45 | $50 – $70 | $600 – $700 |

| 55 | $120 – $160 | $900 – $1,100 |

This difference explains why many young families start with term coverage, then consider retirement investments alongside it instead of committing early to whole life. The FTC’s consumer advice also reminds buyers to compare lifetime costs carefully before committing.

Suitability for Different Age Groups

Suitability depends on age, financial priorities, and long-term goals.

- Young Adults (20s–30s): Term life is ideal due to low premiums. A $500,000 policy may cost less than a student bank account monthly maintenance fee. Whole life at this stage may strain budgets.

- Middle Age (40s–50s): Many combine term coverage with high-yield savings or investments. Whole life may make sense for estate planning or long-term dependents.

- Seniors (60+): Term life becomes expensive and harder to qualify for. Whole life or guaranteed issue coverage may be better options to secure inheritance or cover final expenses.

The Pennsylvania insurance office stresses that suitability often depends on whether you want temporary protection (term) or lifelong security plus cash value (whole life).

Life Insurance for Families in 2025

Life insurance remains one of the most important financial tools for families in 2025. Parents use it to protect income, pay off mortgages, and ensure children’s education is funded if the unexpected happens. Stay-at-home spouses also need coverage, since their household role carries real financial value if suddenly lost. For children, policies help guarantee future tuition and living costs, making sure long-term goals stay on track. By combining affordable term coverage with savings accounts and retirement strategies, families create both immediate security and lasting stability.

Best Policies for Parents

For parents, life insurance is the cornerstone of financial security. A primary wage earner’s sudden death could leave children and surviving spouses struggling with mortgages, childcare, and long-term expenses. That’s why many parents choose term life policies they offer affordable coverage during the years when financial obligations are highest.

For example, a 35-year-old parent with two children might purchase a 20-year term policy aligned with the years until their kids graduate from college. This ensures tuition, housing, and daily needs are covered even if income disappears. Parents who want lifelong protection and wealth transfer may consider whole life or universal life insurance for permanent coverage plus cash value.

The Texas Insurance Department advises parents to calculate coverage by including income replacement, mortgage payoff, and education costs not just funeral expenses. Combining life insurance with high-yield savings ensures liquidity alongside protection.

Life Insurance for Stay-at-Home Spouses

Stay-at-home parents contribute enormous economic value childcare, household management, and daily support that would be expensive to replace. Yet many families overlook insuring the non-working spouse. If a stay-at-home spouse passes away, the surviving partner may face childcare expenses, domestic help, and reduced ability to work full-time.

Affordable term policies for stay-at-home spouses can cover these hidden costs. A modest $250,000–$500,000 policy ensures funds are available for childcare, tutoring, or household support. Some families also explore umbrella insurance to expand liability coverage, but life insurance remains the primary tool for family stability.

The FTC’s consumer guidance stresses that families should insure both partners, not just the income earner, to avoid financial gaps. This approach reflects the true cost of raising children and maintaining stability.

Covering Children’s Future Education

Education costs in the U.S. continue to rise, making college funding one of the biggest motivators for family life insurance. Policies can ensure that tuition, housing, and other expenses are covered even if parents aren’t around to provide financial support.

Parents often pair a 20- or 30-year term life policy with a coverage amount designed to cover projected tuition. For example, a $500,000 policy can set aside $200,000 for education while leaving $300,000 for housing and other living expenses. Families also combine life insurance with dedicated student accounts and student credit cards to build early financial habits for children.

The Utah life insurance buyer’s guide encourages families to calculate future tuition inflation when deciding coverage amounts. Some whole life or indexed universal policies can also be used strategically, as their cash value can help offset rising education costs while still providing a death benefit.

Real-World Example: Two-Parent Household

Consider a couple with two children aged 5 and 7. Both parents purchase $500,000 20-year term life policies. If one parent passes away, the surviving spouse can pay off the mortgage, hire childcare, and allocate funds for future college tuition. By pairing coverage with retirement investment strategies, the family creates both immediate protection and long-term growth.

Life Insurance for Seniors

Best options for seniors

Picking the right coverage gets harder (and pricier) with age, so keep it simple and goal-based.

Ages 50–59 (still working or paying a mortgage)

- 10–20-year term for income replacement and mortgage payoff. Convert later if needed.

- Guaranteed Universal Life (GUL) to a set age (90/95/100) for lifelong protection without high whole-life costs.

- If you hate medical exams, look at simplified issue or no medical exam options (see no medical exam).

- Pair insurance with emergency cash in high-yield savings to keep premiums affordable.

Ages 60–69 (pre-retirement/early retirement)

- 10–15-year term for late mortgage years or to bridge a spouse to full retirement benefits.

- GUL to age 90/95 for permanent but cost-controlled coverage.

- Small whole life for estate needs or lifetime final-expense planning.

- Review beneficiary tax basics (death benefits are usually income-tax free per IRS rules).

Ages 70+ (fixed income, legacy/final expenses)

- Final expense whole life ($5k–$25k) with easy underwriting; some are guaranteed issue.

- GUL may still be available if health is good; expect higher premiums and lower face amounts.

- Veterans should review VA life insurance options; check state resources for consumer protections (consumer guide, state resource, buyer’s guide).

Helpful resources: state buyer guides like consumer guide (Texas) and buyer’s guide (Utah) explain senior options plainly.

Final expense policies explained

Final expense policies are small whole life plans designed to cover funeral and last bills so family doesn’t scramble for cash. Key traits:

- Coverage amounts: usually $5,000–$25,000 (sometimes up to $40,000).

- Underwriting: many are simplified (a few health questions) or guaranteed issue (no health questions).

- Graded benefit: some guaranteed policies pay a limited benefit in the first 2 years (e.g., refund of premiums plus interest if death is non-accidental), then full benefit after the waiting period.

- Permanent: premiums stay level; coverage lasts for life if you pay on time.

- Uses: funeral/burial, small debts, medical copays, travel costs for family.

When to choose it:

- You’re 70+, on a fixed income, and want a small, permanent policy your kids can rely on.

- Health issues make traditional underwriting hard. Look at state resource and consumer advice for red-flags and shopping tips.

- If you already have savings, you may combine a smaller policy with cash in high-yield savings to avoid over-insuring.

If you’ve lost track of an old policy, some states offer policy locator tools (see policy locator).

Costs and coverage examples

Rates vary by age, health, tobacco use, face amount, and state rules. These illustrative ranges (non-smoker, average health) show the pattern seniors can expect in 2025.

Example 1 — Final Expense Whole Life ($15,000 benefit)

| Age | Male / mo. | Female / mo. |

|---|---|---|

| 60 | $45–$65 | $35–$55 |

| 70 | $75–$110 | $60–$90 |

| 75 | $110–$155 | $85–$125 |

Example 2 — Simplified-Issue Whole Life ($25,000 benefit)

| Age | Male / mo. | Female / mo. |

|---|---|---|

| 60 | $70–$95 | $55–$80 |

| 65 | $90–$125 | $70–$100 |

| 70 | $130–$180 | $100–$145 |

Example 3 — 10-Year Term ($100,000 benefit)

| Age | Male / mo. | Female / mo. |

|---|---|---|

| 60 | $40–$70 | $32–$55 |

| 65 | $70–$120 | $55–$95 |

| 70 | $130–$220 | $100–$175 |

Why these ranges help: they show how earlier purchase = lower cost. If premiums feel high, consider a smaller face amount plus cash in high-yield savings or coordinate with retirement strategies.

Quick decision guide

- You want the lowest bill and only need coverage for 10–15 years → pick short term.

- You need coverage for life but want to control cost → look at GUL to age 90/95.

- You mainly want funeral costs covered and want easy approval → choose final expense (consider guaranteed issue if health is tough).

- You’re a veteran or federal retiree → check VA life insurance and FEGLI program before buying private coverage.

- You’re unsure about taxes → death benefits are generally income-tax free (see IRS rules), but review estate issues if your assets are large (coordinate with tax minimization).

Real-world scenarios

- Age 58 couple, mortgage left: Each buys $250k, 15-year term to finish the loan and protect income. Keeps emergency cash in high-yield savings.

- Age 66 retiree, no debt: Buys GUL to age 95 for $150k to leave money to adult children and a charity.

- Age 73 widow, fixed income: Buys $15k final expense to cover funeral and small medical bills. Uses state consumer guide to compare offers; avoids high-pressure upsells.

- Age 70 veteran: Reviews VA life insurance options first; supplements with a $10k final expense policy if needed.

Life Insurance for Young Adults

Why Millennials & Gen Z Should Consider Coverage

Life insurance might feel premature when you’re young but here’s why it’s actually smart, even in your 20s:

- Lock in low rates: Providers base premiums on age and health at application, so members of younger generations can secure long-term affordability. A healthy 25-year-old might pay as little as $18–$22 per month for a $500,000, 20-year term policy cheaper than popular streaming subscriptions.

- Cover growing responsibilities: Many millennials and Gen Zers graduate with student loans, start families, or take on mortgages. A modest term policy protects loved ones from debt lifecycles or sudden income loss and sets the foundation for future financial planning.

- Build lifelong financial habits: Pairing life insurance with high-yield savings or retirement investment strategies helps create a stable financial base. It’s like locking your protection into your routine before life gets costlier.

- Peace of mind for families: Even if you’re single, insuring yourself ensures parents or co-signers aren’t left with debts you’ve guaranteed.

According to the FTC’s consumer guide, buying early maximizes coverage value and avoids age-related rate increases. Young Americans are increasingly turning to budgeting apps and robo-advisors, but life insurance adds a layer of certainty that digital tools alone can’t replace.

Cheapest Policy Options for Young Buyers

For young adults looking for value and simplicity, these are the most cost-effective life insurance strategies:

20- or 30-Year Term Life Insurance

- Why it’s ideal: Lowest premium per dollar of coverage. Covers critical years (student loans, careers, first home) without long-term commitment.

- Example: A healthy 30-year-old non-smoker male gets $500,000 coverage for ~$22/month; a female pays slightly less.

- Flexibility: Many policies allow conversion to permanent options later without another medical exam.

Simplified-Issue or No Medical Exam Term

- What’s different: Skips full exam just health questionnaire. Premiums are slightly higher but approval is quicker and more convenient.

- Best for: Busy college students or early professionals who don’t want to schedule a clinic visit.

Riders for Added Security

- Accidental Death Rider: Adds coverage specifically for accidental death only, at minimal cost useful for risky jobs or hobbies.

- Waiver of Premium: Lets your premiums pause if you become disabled, keeping coverage intact during hardship.

Hybrid or Convertible Options

- Convertible Term Policies: Start with low term cost, then convert to whole or universal life later—a good match for changing plans (e.g., marriage, home buying).

- Indexed Universal Life (IUL): If you’re finance-savvy, an IUL ties cash value growth to market indices. You get some upside without direct investment risk but still more expensive than term.

Quick Decision Checklist

| Question | If “Yes” → Best Option |

|---|---|

| Want lowest cost now? | 20- or 30-year Term |

| Want easy online approval? | Simplified-issue Term |

| Plan to convert later? | Convertible Term |

| Want permanent coverage from the start? | IUL or Permanent Term |

| Need extra coverage for accident/death? | Add an Accidental Death Rider |

Real-World Scenario

A 27-year-old graphic designer, single with $40k in student loans and no debt otherwise:

- Buys a 20-year $250k term policy for ~$12/month.

- This policy covers her student loans and provides income replacement if something unexpected happens.

- She channels the difference between this low premium and what she’d pay for whole life into high-yield savings, creating both protection and liquidity.

Key Takeaways for Young Adults

- Buying life insurance early maximizes your financial efficiency, securing coverage when you’re most affordable.

- For most in this age group, term life is the smartest, most budget-friendly starting point.

- Add-ons like simplified underwriting or conversion options add flexibility as your life changes.

- This modest investment today lays the foundation for long-term security and gives you a head start most of your peers haven’t taken.

Life Insurance for High-Net-Worth Individuals

Life insurance is not just about protecting income for high-net-worth households it becomes a strategic wealth tool. In 2025, many affluent families use policies as part of estate planning, tax efficiency, and legacy transfer. Here’s how it works in detail:

Estate Planning Benefits

For individuals with multi-million-dollar estates, life insurance ensures liquidity when heirs need it most. Federal estate taxes can be significant for estates exceeding the exemption limits, which means beneficiaries may face heavy tax bills upon inheritance. By owning a well-structured policy, families provide heirs with immediate funds to cover taxes and legal costs without selling assets like real estate or businesses at a discount.

A permanent policy such as whole life or guaranteed universal life provides predictable benefits. Some wealthy households also use umbrella insurance alongside life insurance to ensure liabilities don’t erode estate value. The Pennsylvania Insurance Department notes that life insurance is often one of the simplest tools for ensuring estates pass smoothly across generations.

Using Life Insurance for Tax Strategies

Life insurance offers multiple tax advantages. The death benefit is generally income-tax free for beneficiaries, according to the IRS rules. Cash value in permanent policies also grows tax-deferred, which means no annual taxes on gains. Wealthy policyholders often leverage loans against cash value, creating tax-advantaged liquidity during retirement or business transitions.

For estates above the federal exemption threshold, life insurance can fund estate taxes directly, preventing heirs from liquidating other investments. Pairing coverage with tax-free investment strategies ensures a diversified approach: liquid savings, market investments, and guaranteed policy proceeds all work together to maximize after-tax wealth.

Trusts and Wealth Transfer Planning

High-net-worth families frequently use trusts to integrate life insurance into broader wealth transfer strategies. An Irrevocable Life Insurance Trust (ILIT), for example, removes the policy from the estate, keeping the death benefit outside taxable limits. The trust owns the policy, pays premiums, and directs proceeds to heirs or charitable causes.

This structure is particularly useful for families with complex estates or philanthropic goals. It ensures that payouts are controlled, tax-efficient, and legally protected. State regulators, like the California Department of Insurance, emphasize consulting with estate attorneys to set up trusts properly, as missteps can bring policies back into taxable estates.

By combining ILITs, charitable trusts, and permanent life insurance, wealthy families can balance philanthropy, tax planning, and multi-generational wealth transfer. Pairing these with retirement investment strategies helps ensure that liquidity, growth, and protection align with long-term family goals.

Life Insurance for Small Business Owners & LLCs

Running a small business or LLC means your family and employees often depend directly on you. For many entrepreneurs, life insurance isn’t just personal protection it’s a business continuity tool. In 2025, more owners are using policies to protect their companies, fund transitions, and give employees and partners confidence that the business will survive unexpected events.

Key Person Insurance

Key person insurance (sometimes called key man insurance) is coverage a business purchases on the life of its most critical individual usually the owner, founder, or top executive. If that person passes away, the policy pays a death benefit directly to the company.

Why it matters:

- Provides cash to cover operating expenses, hire a replacement, or offset lost revenue.

- Reassures investors, lenders, and employees that the business has a plan if leadership is lost.

- Helps maintain customer and supplier confidence during a difficult transition.

For example, an LLC with one lead software developer and founder could take out a $1 million key person policy. If the founder dies unexpectedly, the death benefit would fund hiring a skilled replacement and keep payroll running. Without coverage, the company could collapse within months.

The FTC’s consumer guidance recommends that small business owners carefully assess who their “key people” are and insure them appropriately. Pairing this with umbrella insurance can further reduce liability risks.

Buy-Sell Agreements Funded by Life Insurance

For businesses with multiple partners or LLC members, buy-sell agreements ensure a smooth ownership transition when one partner dies. The agreement specifies how ownership shares will be bought and sold. Life insurance provides the funding mechanism to make this possible without draining company assets.

How it works:

- Each partner is insured with a life policy.

- If a partner passes away, the policy’s death benefit is paid to the surviving partners or the business.

- Those funds are used to “buy out” the deceased partner’s shares from their family or estate.

- The surviving owners retain full control, while the deceased partner’s family receives fair compensation.

Example: A three-member LLC values itself at $3 million. Each member owns one-third ($1 million each). To fund the buy-sell agreement, each owner is covered by a $1 million life insurance policy. If one partner dies, the surviving two partners receive the payout and use it to purchase the deceased partner’s share.

The IRS confirms that life insurance payouts are generally income-tax free, which makes them an efficient way to fund these agreements. For additional structure, businesses can hold policies in a trust or directly in the company.

Why It Matters for Small Business Owners

- Protects business value and employees from sudden disruptions.

- Ensures heirs are fairly compensated without forcing a fire sale of company assets.

- Provides liquidity when banks or investors might hesitate to support the company during leadership changes.

- Strengthens credibility with lenders, since many banks require key person policies before issuing loans.

Pairing buy-sell funding with retirement strategies or tax-free investment tools creates a holistic financial plan for business continuity. State-level departments like the California Insurance Department also provide consumer guides for business owners reviewing insurance products.

How Much Life Insurance Do You Really Need?

Many Americans struggle with the big question: how much life insurance do I need USA? The answer depends on income, debts, family obligations, and long-term goals. Instead of guessing, you can use rules of thumb, calculators, and real-world scenarios to arrive at a number that provides peace of mind without overspending. Below is a step-by-step guide that takes you through the process.

Two Fast Ways to Estimate Coverage

The simplest way to calculate coverage is to start with a quick formula. The most popular is the 10–15× income rule. For example, if you earn $70,000 annually, you’d need at least $700,000 and up to $1,050,000 in coverage. This ensures your family can replace your income for many years if something happens to you. It’s a fast estimate but doesn’t capture every expense, so it should be refined later.

Another widely used method is the DIME formula, which stands for Debt, Income, Mortgage, and Education. You add up your outstanding debts (excluding mortgage), the number of years you want to replace income, your remaining mortgage balance, and expected education costs for children. Subtract any savings or existing coverage, and the result is your insurance need. Both methods are quick, easy, and recommended by resources like the Utah life insurance buyer’s guide.

A Quick Worksheet

Once you know the formulas, it helps to put them into a worksheet. This lets you see every piece of your financial picture clearly. For example, list all debts, annual income, and the years you’d want your family covered. Add your mortgage and future education costs, then subtract assets like high-yield savings or brokerage funds.

If you already have life insurance through work, subtract that as well. The Texas Insurance Department advises families to think of insurance as filling the gap between what you already have and what your loved ones will need. Writing out numbers makes the process more realistic than simply picking a round figure.

Examples You Can Borrow

Sometimes the best way to answer “how much life insurance do I need USA” is by looking at people in similar situations. Take a 35-year-old parent with two young kids and a $280,000 mortgage. If they want to replace income for 12 years, pay off the mortgage, and cover two college educations, they’d need roughly $1.3–$1.5 million in coverage.

A dual-income couple in their 40s, with older children and just 10 years left on the mortgage, may only need $750,000. A small business owner with loans might need closer to $2 million to cover both family and company obligations. These scenarios mirror real life and help you visualize why coverage amounts differ so much depending on family stage.

Factors That Move Your Number Up or Down

Every household is different, and small details can change how much life insurance you need. A large family with young children requires more coverage than a couple with no dependents. If your spouse doesn’t earn much, you’ll need higher income replacement. If you have co-signed private student loans, your heirs might inherit them, so coverage should be larger.

On the flip side, if you have substantial liquid assets or investments, you can reduce the amount of insurance you buy. The Pennsylvania Insurance Department advises buyers to revisit these factors every few years to make sure coverage stays aligned with changing goals.

Term Length: Pick Years That Match Real Life

It’s not just the amount of insurance, but the length of coverage that matters. Most families choose between 10, 20, or 30-year term life insurance. The rule of thumb is to match the term to your biggest financial responsibilities. If you have toddlers, a 30-year term makes sense it lasts until they’re grown and independent. If your mortgage only has 12 years left, a 15-year term may be enough.

Some households use laddering: buying two or more policies with different lengths. For example, a 30-year $1 million policy plus a 15-year $500,000 policy gives strong coverage now, then naturally decreases as kids finish school and debts shrink. This approach reduces costs while matching real-life needs.

Don’t Forget These Easy-to-Miss Items

Many people focus only on replacing their salary, but they overlook other important coverage needs. For example, stay-at-home spouses provide services like childcare and household management that would be expensive to replace. A modest term policy ensures funds for daycare or domestic help.

Employer-provided coverage is another trap. While useful, it usually covers only one or two times your salary, and it often disappears if you leave the job. Inflation is also a big factor $500,000 in 2025 won’t buy the same security 15 years later. That’s why the FTC’s consumer guide advises families to revisit policies regularly. Riders, like child coverage or accelerated death benefits, also add value but should be chosen carefully.

Taxes, Beneficiaries & Paperwork

One of the reasons life insurance is so powerful is tax treatment. According to the IRS, death benefits are generally income-tax free, though very large estates may still face estate taxes. To avoid confusion, it’s important to name both a primary beneficiary (like your spouse) and a contingent beneficiary (like your children).

Families should also know about tools like the California policy locator, which help track lost or forgotten policies. Proper paperwork ensures claims are paid quickly, avoiding delays during an already stressful time.

Action Plan

To answer how much life insurance do I need USA in practice, follow three steps. First, pick a method: either the 10–15× income rule or the DIME formula. Second, match the term length to your financial milestones, such as paying off a mortgage or funding a child’s education. Third, compare quotes from at least three A-rated insurers, and review your policy every 2–3 years to make sure it still fits your situation.

The USA.gov official guide recommends starting with at least basic coverage while young and healthy, then adjusting upward as responsibilities grow. By using a structured approach, you’ll avoid both under-insuring your family and overspending on coverage you don’t need.

How Much Does Life Insurance Cost in 2025?

One of the most common questions people ask is: what’s the life insurance cost per month in the USA? The answer depends on several key factors: age, gender, health, lifestyle, coverage amount, and policy type. Insurers use actuarial tables, medical records, and underwriting questions to calculate premiums, which is why no two buyers pay the same rate. Still, you can get a good idea of what to expect by looking at averages across the industry in 2025.

Average Premiums by Age, Gender, and Health

Age is the single biggest driver of life insurance cost per month. A healthy 25-year-old might pay less than $20 for a $500,000 term policy, while a 55-year-old could pay five times as much. Rates rise each year you delay, which is why experts and the Utah buyer’s guide stress the importance of buying coverage early.

Gender also plays a role. Women typically pay 15–30% less than men for the same policy, because they tend to live longer. For example, a healthy 30-year-old woman may pay around $18 monthly for a $500,000 20-year term, while a man of the same age may pay $22–$25.

Health status significantly affects premiums. Non-smokers pay much less than smokers sometimes less than half. A smoker in their 40s could easily pay $100–$150 per month for the same policy a non-smoker gets for $35–$45. Conditions like diabetes, high blood pressure, or obesity may also increase costs.

Lifestyle factors matter as well. Risky hobbies (skydiving, scuba diving), hazardous occupations, or DUIs can all lead to rate increases. Insurers look at your total risk profile, not just your age.

Table of Sample Quotes 2025 Estimates

Here’s a look at average monthly premiums for a 20-year, $500,000 term life policy in 2025 (non-smokers, average health)

| Age | Male (Monthly) | Female (Monthly) |

|---|---|---|

| 25 | $18 – $22 | $15 – $19 |

| 30 | $22 – $26 | $18 – $23 |

| 35 | $27 – $34 | $22 – $28 |

| 40 | $33 – $41 | $28 – $35 |

| 45 | $50 – $65 | $42 – $55 |

| 50 | $78 – $95 | $65 – $80 |

| 55 | $110 – $140 | $90 – $115 |

| 60 | $190 – $230 | $155 – $200 |

Smokers can expect to pay 2–3× these amounts. For example, a 40-year-old smoker could pay over $100 per month for the same coverage a non-smoker buys for $35.

Permanent policies, such as whole life insurance, cost significantly more because they provide lifetime coverage and build cash value. A 30-year-old might pay $350–$450 per month for a $500,000 whole life policy more than 15 times the cost of term.

Key Insights on Costs

- Buy young to save big: Waiting until your 40s or 50s multiplies your premiums. A 25-year-old pays less than one-tenth of a 60-year-old’s rate.

- Health is wealth: Staying smoke-free, maintaining a healthy BMI, and controlling chronic conditions lowers premiums significantly.

- Women save more: Across the board, women consistently pay less due to longevity.

- Coverage amount matters: $1 million of coverage is not double the cost of $500,000 it’s often just 50–70% more. Larger policies can be more cost-efficient per dollar of coverage.

- Policy type makes the difference: Term life is pure protection and cheapest per dollar. Whole, universal, or indexed policies cost much more but provide lifetime guarantees and savings components.

Real-World Example

A 32-year-old woman, non-smoker, with no major health issues, buys a $750,000 20-year term policy. Her premium is about $24 per month. If she waited until 42 to buy the same policy, her monthly premium would jump to around $42–$50, and at 52 it would soar to $90–$120. This simple example shows why the best time to secure life insurance is when you’re young and healthy.

Factors That Affect Life Insurance Premiums

When shopping for coverage, one of the first things people ask is: “Why do two people with the same policy pay such different rates?” The answer is underwriting. Insurers look at dozens of variables to calculate the life insurance cost per month, but the biggest factors are your age, health, habits, occupation, lifestyle, and the type of policy you choose. Understanding these variables helps you anticipate costs and position yourself for the best rates.

Age: The Most Powerful Premium Driver

Age is the single largest factor. The younger you are when you apply, the lower your monthly cost will be. A healthy 25-year-old can secure $500,000 of 20-year term coverage for under $20 per month, while a 55-year-old might pay five times that amount for the same policy.

The reason is simple: insurers price risk based on life expectancy. Each year you delay, the probability of death rises, and premiums increase accordingly. That’s why experts and the Utah life insurance buyer’s guide encourage locking in coverage early. Buying while young also allows you to qualify for longer terms 20, 25, or 30 years at much cheaper rates.

Health: Medical History and Current Condition

Health plays a critical role. Applicants complete questionnaires and often undergo a medical exam. Chronic conditions like diabetes, hypertension, or obesity can increase premiums significantly. Family history of early heart disease or cancer may also impact your rate.

On the other hand, maintaining good health pays off. Regular exercise, healthy weight, and preventive care can place you in a “preferred” category, leading to lower premiums. Some insurers even reward healthy behaviors certain companies offer discounts for non-smokers or those who track fitness through apps. The FTC’s consumer guidance advises reviewing your medical information carefully to ensure accuracy when applying, since misstatements can delay or deny claims.

Occupation & Lifestyle Risks

Insurers also consider your career and hobbies. Certain jobs such as construction, aviation, trucking, or firefighting carry higher risks and result in higher premiums. Similarly, lifestyle activities like scuba diving, skydiving, or rock climbing may trigger surcharges.

Even driving history can impact premiums. Multiple DUIs or reckless driving convictions can raise costs, since they suggest higher mortality risk. The New York DFS requires insurers to disclose how lifestyle risks impact underwriting so consumers know what to expect. For many applicants, being transparent upfront avoids surprises later.

Policy Length and Coverage Amount

Finally, the type of policy and the coverage size matter greatly. A 10-year term policy will always be cheaper than a 30-year term, because the insurer’s exposure window is shorter. Likewise, a $1 million policy costs more than a $250,000 policy but not always four times as much. Larger policies often offer better “per dollar” value, meaning the cost per $1,000 of coverage declines as the face amount increases.

Permanent policies like whole life or universal life cost far more than term because they guarantee lifetime coverage and include a cash value component. For example, a 30-year-old might pay $25 monthly for a term plan but $400 for a comparable whole life plan. State regulators, like the California Department of Insurance, stress that buyers should carefully weigh these costs against long-term financial goals.

Pulling It Together: Why These Factors Matter

Your life insurance cost per month reflects a mix of personal and policy-related risks. While you can’t control your age, you can improve health habits, quit smoking, and choose policy terms that align with your needs. For families, it’s often best to combine an affordable long-term policy with other tools like high-yield savings accounts and retirement investment strategies for a balanced plan.

By understanding these factors upfront, you can shop smarter, compare rates with confidence, and lock in affordable coverage that truly matches your family’s financial picture.

Medical Exam vs No Medical Exam Policies

When buying coverage, one of the first choices is whether to take a traditional medical exam or apply for a no-exam policy. Both options provide valuable protection, but the differences affect price, approval speed, and eligibility. Understanding how they work helps you decide which is right for your situation.

Pros and Cons of Medical Exam Policies

Traditional medical exam policies require applicants to undergo a brief health check-up. This usually includes blood and urine tests, height/weight measurement, blood pressure reading, and sometimes an EKG. The exam is free, handled by the insurer, and often conducted at your home or office.

Pros:

- Lower premiums: Insurers have detailed health data, so healthy applicants get the cheapest rates.

- Higher coverage amounts: Often available in the $500,000 to multi-million-dollar range.

- Broader policy options: Term, whole, universal, and even advanced riders are more accessible.

Cons:

- Slower approval: Underwriting can take 4–8 weeks.

- Invasive for some: Medical testing may be uncomfortable.

- Stricter for health conditions: Existing issues may lead to higher premiums or denial.

For young, healthy buyers, exam policies usually offer the best value per dollar of coverage, especially when looking at large-term or permanent policies.

Pros and Cons of No Medical Exam Policies

No-exam life insurance skips lab work and instead relies on health questionnaires, prescription history, or electronic records. Approval can take just days, sometimes even instantly.

Pros:

- Fast approval: Coverage often issued within 24–72 hours.

- Convenient: No needles, doctor visits, or scheduling delays.

- Accessible: Good for people who dislike exams or have busy schedules.

Cons:

- Higher premiums: Insurers price cautiously without exam data, so coverage costs more.

- Lower face amounts: Usually capped at $250,000–$500,000, though some carriers go higher.

- Limited availability: Fewer permanent products, with most options being term policies.

For buyers who value speed or may have mild health concerns, no-exam coverage offers a practical balance. Seniors also use these policies, especially when they only need smaller amounts for final expenses.

Companies That Offer No-Exam Coverage

In 2025, several reputable U.S. insurers provide strong no-exam options:

- Haven Life – Online-first, backed by MassMutual; offers term policies up to $1 million for healthy applicants.

- Bestow – 100% online application, quick approval, coverage up to $1.5 million for younger adults.

- Ethos – No-exam term and whole life products, strong fit for middle-aged buyers.

- Lincoln Financial – Accelerated underwriting program for select applicants, up to $1 million.

- State Farm – Simplified issue policies, particularly popular with families.

For smaller coverage amounts, many carriers offer final expense no-exam policies, often capped at $25,000–$40,000. These are especially useful for seniors or people with health challenges. The North Dakota Insurance Department stresses that while no-exam options are convenient, buyers should always compare costs with exam-based policies before committing.

How to Apply for Life Insurance in the U.S.

Step 1: Assess Your Needs and Budget

The first step is deciding why you need life insurance and how much protection is appropriate. Consider your income, debts, family size, and long-term goals. Parents may want enough coverage to support children until adulthood, while business owners may need additional protection for buy-sell agreements or key person risks. A quick way to estimate is using the 10–15× income rule or the DIME method (Debt, Income, Mortgage, Education). Once you have a target number, compare it against your budget. The policy should be affordable without straining your monthly cash flow. Combine it with other tools like high-yield savings accounts for added security.

Checklist:

- Calculate debts (mortgage, loans, credit cards).

- Estimate years of income replacement needed.

- Add children’s future education costs.

- Subtract savings, investments, or existing coverage.

- Decide on a monthly premium range you can sustain.

Step 2: Research Policy Types and Companies

Once you know your coverage needs, compare the different types of life insurance policies term, whole, universal, variable, or final expense. Each serves different purposes. For example, term life is best for affordable temporary protection, while whole life offers lifetime coverage plus cash value. Next, research insurers with strong financial ratings (A.M. Best, Moody’s, or S&P). Choose companies with a reputation for paying claims promptly. Government and state guides like the Texas Insurance Department provide plain-language comparisons that make shopping easier.

Checklist:

- Compare term vs. permanent coverage options.

- Check financial strength ratings (A+, AA, etc.).

- Look for accelerated/no-exam policies if needed.

- Compare quotes from at least 3 insurers.

- Read state buyer’s guides for trusted advice.

Step 3: Gather Necessary Documents and Information

Before starting an application, gather the documents insurers typically require. This saves time and reduces back-and-forth during underwriting. You’ll need basic ID, proof of income, and details about your health history. If you have existing coverage, note down policy numbers. For business owners, financial records may be requested. Seniors applying for no-medical-exam life insurance can expect fewer documents but still need accurate personal details.

Checklist:

- Driver’s license or government ID.

- Social Security number.

- Employer/pay stub or tax return (income proof).

- Mortgage/debt statements.

- Medical records or prescription list (if applicable).

Step 4: Complete the Application Form

Applications can be completed online, through an agent, or over the phone. Expect to provide personal details (age, occupation, family history, and health status). Answer all health questions honestly misrepresentation can lead to denial of claims later. Some companies use electronic health databases, prescription checks, and driving records as part of the process. Applications usually allow you to select riders (extras like child coverage or waiver of premium). Review everything carefully before submission.

Checklist:

- Provide accurate personal and contact details.

- List medical conditions truthfully.

- Choose coverage amount and policy length.

- Select optional riders (if desired).

- Review and sign digitally or on paper.

Step 5: Medical Exam or Accelerated Underwriting

Most traditional policies require a medical exam, which insurers schedule at your convenience (often at home or work). It typically includes blood/urine tests, height/weight, and blood pressure. Results help insurers classify you (Preferred, Standard, or Substandard). Some companies offer accelerated underwriting or no-exam policies, especially for younger, healthy applicants. The North Dakota Insurance Department recommends comparing both routes since no-exam plans cost more but are faster.

Checklist:

- Schedule your exam promptly (morning is best).

- Fast 8–12 hours before bloodwork (unless advised otherwise).

- Bring ID and medication list.

- Stay hydrated and avoid caffeine/smoking before exam.

- Ask for a copy of your results.

Step 6: Underwriting and Approval

After the application and exam, the insurer’s underwriting team evaluates your risk. They review your medical results, driving history, prescription use, and financial background. Depending on complexity, this stage may take 2–8 weeks. During this time, insurers may request additional information or medical records. If approved, you’ll receive an official policy offer with premium details. If denied, you can often reapply with another carrier or explore no-exam options.

Checklist:

- Be responsive to requests for extra documents.

- Stay in touch with your agent or company.

- Compare the final offer with initial quotes.

- Adjust coverage if premiums exceed your budget.

- Consider re-shopping if declined or rated up.

Step 7: Accepting and Activating the Policy

Once approved, review the policy carefully. Check the death benefit, premium schedule, riders, and exclusions. Pay your first premium to activate coverage most insurers require autopay or online billing. Keep a copy of the policy in a safe place, and inform beneficiaries where to find it. Update beneficiary designations after major life events like marriage, divorce, or having children. The FTC’s consumer advice reminds buyers to always verify policy terms and cancellation rules.

Checklist:

- Review policy contract details.

- Pay the first premium to start coverage.

- Store documents safely (digital + paper copy).

- Notify beneficiaries about the policy.

- Revisit coverage every 2–3 years.

Common Mistakes to Avoid When Buying Life Insurance

When searching for life insurance, many people focus only on cost and speed. But overlooking key details can leave your family underprotected or cause you to overpay. Here are three of the most frequent mistakes buyers make and how to avoid them.

Buying Too Little Coverage

A common mistake is underestimating how much your family would actually need if you weren’t around. People often buy a small policy just to “have something,” but that rarely covers real costs like mortgage payments, childcare, and education. For example, a $100,000 policy may sound large, but for a family with two kids and a home loan, it might last less than two years. To avoid this, use a coverage formula like the 10–15× income rule or the DIME method (Debt, Income, Mortgage, Education). The Utah life insurance buyer’s guide emphasizes calculating based on actual obligations rather than guesses.

Choosing the Wrong Policy Type

Another mistake is buying the wrong type of policy for your goals. For example, term life is ideal for temporary needs (like raising children or paying off a mortgage), while whole life or universal life works better for lifelong protection, estate planning, or building cash value. Some buyers pay higher premiums for permanent coverage when a simple 20-year term policy would have met their needs at a fraction of the cost. The Texas Department of Insurance suggests reviewing both term and permanent options with an agent to avoid mismatches.

Not Comparing Multiple Quotes

Finally, many buyers stick with the first insurer or agent they talk to. This often means paying higher premiums than necessary or missing out on better policy features. Premiums for the same coverage can vary widely between companies. For instance, a healthy 30-year-old non-smoker could see differences of $10–$20 per month on a $500,000 policy depending on the insurer. That adds up to thousands of dollars over the term. Comparing at least three quotes and reviewing state guides like the California Department of Insurance ensures you find the best balance of price, coverage, and service.

Best Life Insurance Companies in the U.S. 2025

Finding the best life insurance companies USA 2025 means comparing financial strength, customer satisfaction, product variety, and digital convenience. Each insurer has unique advantages depending on whether you want the lowest premiums, the most flexible policy, or the strongest estate planning tools. Below is a detailed review of the top providers in 2025, followed by a comparison table.

State Farm

State Farm remains one of the most trusted insurers in the U.S., thanks to its agent-driven model. Families who prefer face-to-face support appreciate its personalized service. The company offers term, whole, and universal life, plus strong rider options. State Farm is especially strong for customer satisfaction and is ranked among the top for claims support. However, online applications are more limited compared to newer digital-first competitors.

- Strengths: Excellent service, wide agent network, strong rider availability.

- Ratings: A++ (AM Best).

- Best For: Families wanting local support and personalized advice.

New York Life

New York Life is the largest mutual life insurance company in the U.S., with over 175 years of history. It offers a broad range of permanent policies, including whole life with strong dividends. Policyholders benefit from the company’s financial strength and ability to pay long-term claims. While premiums may be higher, New York Life excels in long-term value and conversion flexibility.

- Strengths: Leading financial strength, strong dividends, variety of permanent policies.

- Ratings: A++ (AM Best).

- Best For: Buyers seeking lifelong coverage and estate planning stability.

Northwestern Mutual

Northwestern Mutual consistently ranks among the top life insurers for financial strength and dividends. It offers customizable whole life and universal policies, with strong planning support for high-net-worth individuals. Like New York Life, it is a mutual company, meaning profits are shared with policyholders through dividends. The main drawback is that online quotes are limited you generally work through a financial advisor.

- Strengths: Outstanding dividends, estate planning expertise, strong financial reputation.

- Ratings: A++ (AM Best).

- Best For: High-net-worth buyers and those seeking permanent life with strong cash value.

Prudential

Prudential is well-known for offering flexible term life policies and a variety of universal life options. It also has more lenient underwriting for certain health conditions, such as diabetes or tobacco use. Digital tools are improving, and Prudential remains one of the largest insurers worldwide. However, it does not currently sell new whole life policies.

- Strengths: Wide range of universal life products, flexible underwriting, global strength.

- Ratings: A+ (AM Best).

- Best For: Buyers with health conditions or those seeking advanced universal life strategies.

Guardian Life