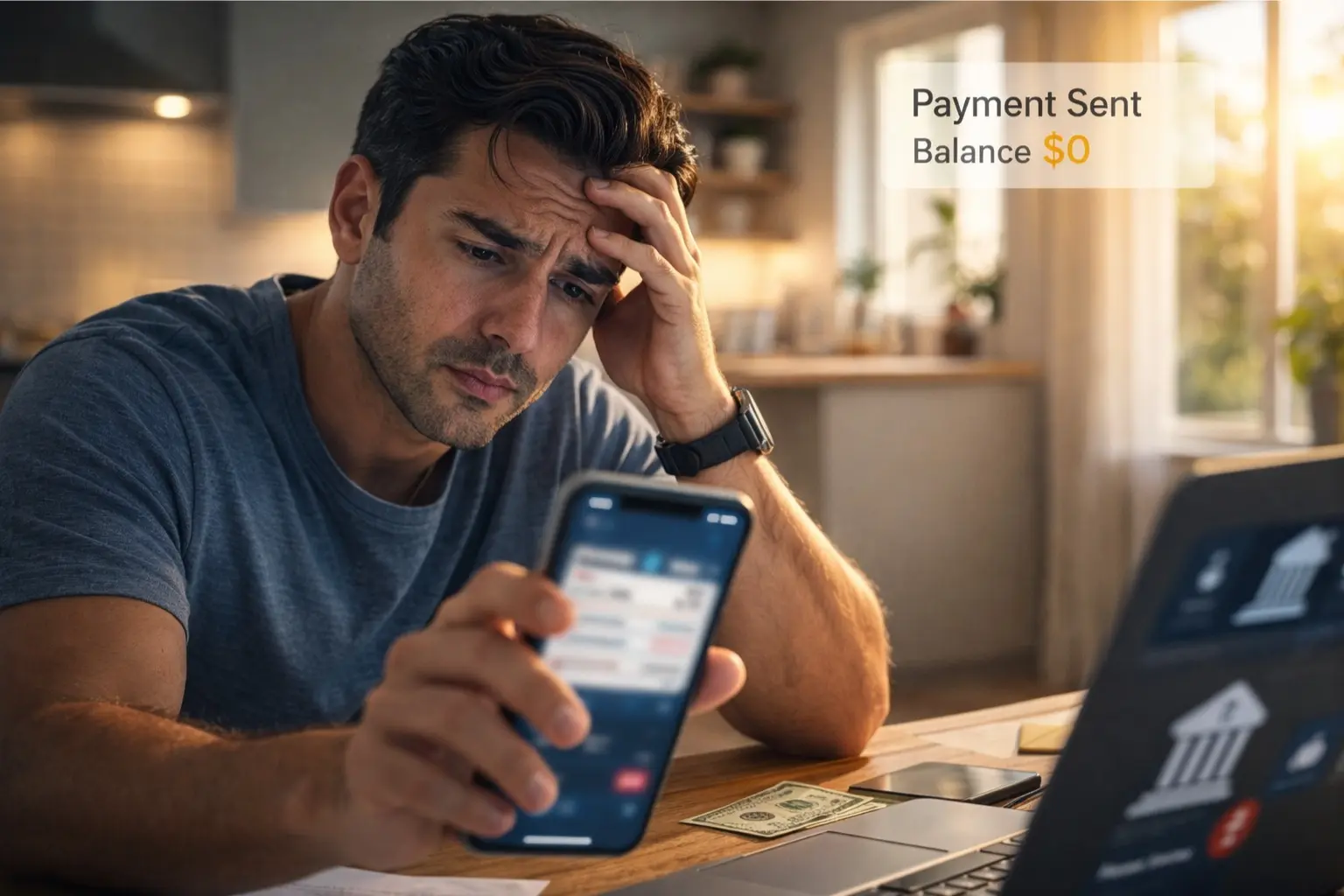

For many people waiting on a deposit, the most confusing moment arrives when a payment status shows “sent,” but the bank balance still reads $0. The message suggests the money has already moved, yet nothing appears inside the account.

That gap happens more often than people realize. Across the United States, payments for payroll, tax refunds, government benefits, and other direct transfers are frequently released overnight.

But the time when a payment is sent and the moment a bank displays the funds can be separated by several hours. This delay is not usually a mistake; it reflects how the payment settlement pipeline processes incoming payment files before they are posted to individual accounts.

Understanding what happens during that window can help explain why balances sometimes remain unchanged in the early morning. Even after a payment has technically been issued.

What “Payment Sent” Actually Means

When a payment status changes to “sent,” it usually means the sending institution has transmitted a payment file into the banking network.

Employers, government agencies, and financial institutions use this step to release deposit instructions to the broader payment infrastructure. However, that transmission does not mean the receiving bank has already posted the funds to a customer’s account.

Instead, the payment moves into a settlement pipeline that coordinates how money travels between financial institutions. Because of overnight payment release protocols, the sending organization submits payment instructions.

But the receiving bank must still process the incoming file and verify the transaction before updating account balances. This is why a payment can be officially “sent” while the receiving bank is still preparing the deposit for posting via the ACH transfer network.

The Overnight Processing Stage

Most large deposit files enter the banking system overnight. During these hours, payment instructions move through clearing networks that handle the transfer of funds between banks. These networks process transactions in batches, allowing thousands or even millions of payments to travel through the system simultaneously.

Financial institutions receive incoming settlement files during this stage and begin preparing them for posting. Because this deposit processing stage occurs behind the scenes, customers do not see the processing phase directly.

From their perspective, it may simply appear as if a payment has disappeared into the system. But during these overnight hours, banks are actually performing the first stage of reconciliation before deposits become visible.

Why Bank Balances Stay $0 at First

Even after a bank receives a payment file, the funds do not immediately appear in customer balances. Financial institutions run a series of internal checks before releasing deposits.

These verification steps ensure that incoming transactions match settlement records, account details, and regulatory requirements. Once those checks are complete, banks schedule the deposit for the next posting window based on their individual bank posting schedule.

Each institution operates its own posting timetable. Some banks update balances shortly after early morning settlement files arrive, sometimes showing a pending deposit explanation to alert customers.

Others post deposits later in the day as additional batches are processed. That difference in timing explains why two people expecting deposits at the same time can see completely different results.

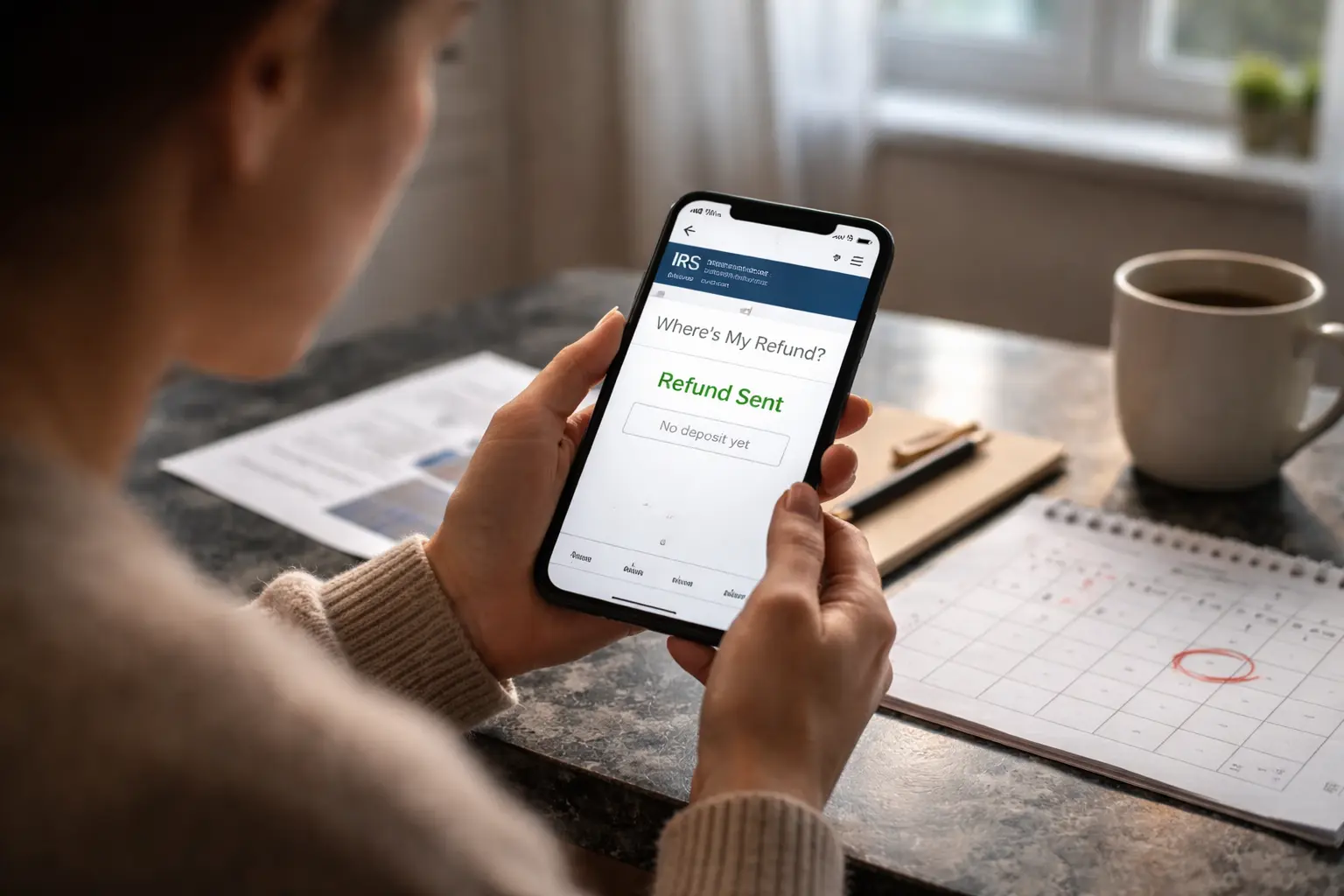

When Deposits Usually Appear

For most payments transmitted overnight, deposits begin appearing during the morning banking cycle. Early posting windows often open between the pre-dawn hours and mid-morning as institutions begin processing based on their specific settlement timing window.

Additional deposit batches may appear later in the day as banks complete reconciliation steps and release the next wave of transactions. This staggered pattern can make a balance update delay feel unpredictable.

But the underlying process follows a structured rhythm inside the overnight clearing cycle. If a payment has already been sent, the receiving bank is typically still moving it through internal processing before it becomes visible.

Once the next posting window opens, many balances update quickly, and the next deposit wave begins to reflect in accounts. In other words, the period between “payment sent” and “deposit visible” is often just a temporary stage inside the larger payment pipeline. As today’s banking cycles continue, more accounts across the country may begin reflecting incoming deposits.

Author