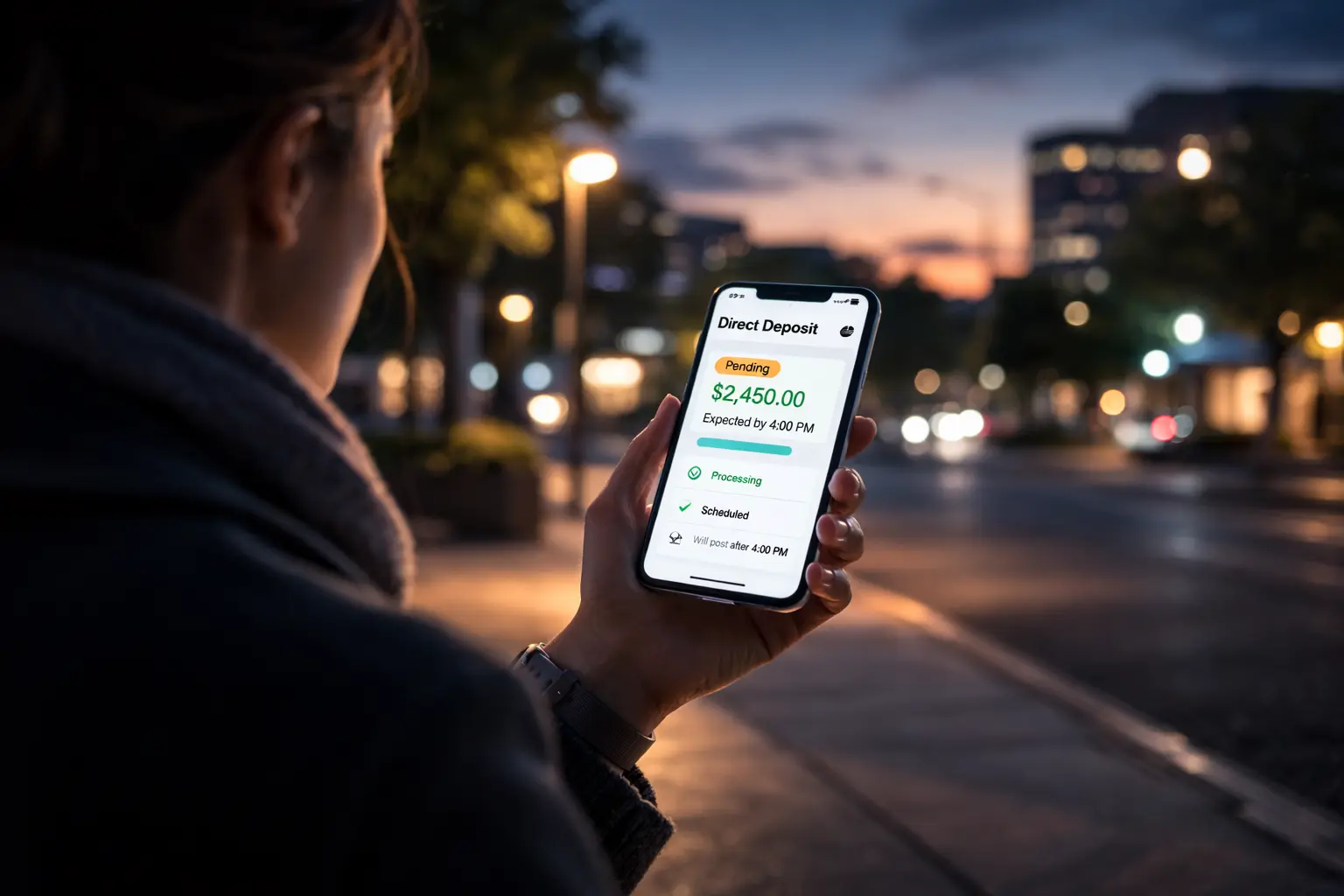

It’s happening again. Screenshots are spreading. Group chats are buzzing. Some people say they see activity. And you’re staring at your bank app wondering why your balance hasn’t moved.

If you’ve refreshed your account more than once today, you’re not alone. The phrase “$2,000 direct deposit” is trending across searches, not because everyone received money, but because visibility is uneven. Some accounts show movement. Others show nothing. Here’s what’s actually happening inside the system right now.

Why $2,000 Direct Deposit Activity Feels Uneven

When a large federal payment enters the pipeline, it does not land everywhere at once. Payments move through structured settlement layers that define the U.S. money movement infrastructure.

Once a payment is authorized, it flows through the Treasury’s disbursement channel before entering the ACH network. This internal sequence often creates confusion, but it is standard procedure within the Treasury payment system.

The key point is simple: Release does not equal availability. Some banks display incoming files earlier, while others wait for final settlement confirmation. Because some institutions show pending indicators and others show nothing until funds are spendable, this difference in bank policy creates today’s tension.

What Is Actually Moving Behind the Scenes

When a federal payment is initiated, it typically enters the Automated Clearing House system in coordinated batches. ACH processing is not instant; it is highly structured.

Even same-day ACH follows strict coordination rules regarding ACH timing differences. Banks receive these incoming files and perform internal processing steps that most customers never see.

Those critical steps include: Reserve reconciliation, ledger alignment, fraud screening and liquidity balancing. That final balancing stage is why some people see activity before others.

We explore the mechanics of these posting cycles in our breakdown of overnight clearing cycles. If your account shows $0 right now, it does not automatically mean no payment exists. It may simply mean your institution has not completed its final posting window.

Why Comparison Makes It Feel Worse

The real pressure comes from comparison. When someone in your group chat posts a screenshot or a coworker says their deposit just hit, you naturally wonder why you see nothing.

That difference is usually not IRS favoritism; it is simply posting structure. Banks control release timing through internal settlement windows, a process we documented in our analysis of how banks control posting. Some institutions release between midnight and 6 AM, while others finalize between 6 and 9 AM.

Even early direct deposit programs operate on modeled risk buffers rather than true settlement, a structure we cover in our review of early deposit risk. So when one person sees $2,000 and another sees $0, the difference is often timing, not eligibility.

Why Today Feels Amplified

Large federal payment cycles often cluster. When multiple payments are processed within the same settlement window, visibility spreads unevenly over hours.

We explored this dynamic in our review of federal payment timelines. The reason it feels explosive today is simple: social visibility moves faster than bank settlement. Search interest spikes and speculation grows, but behind the scenes, the system remains methodical.

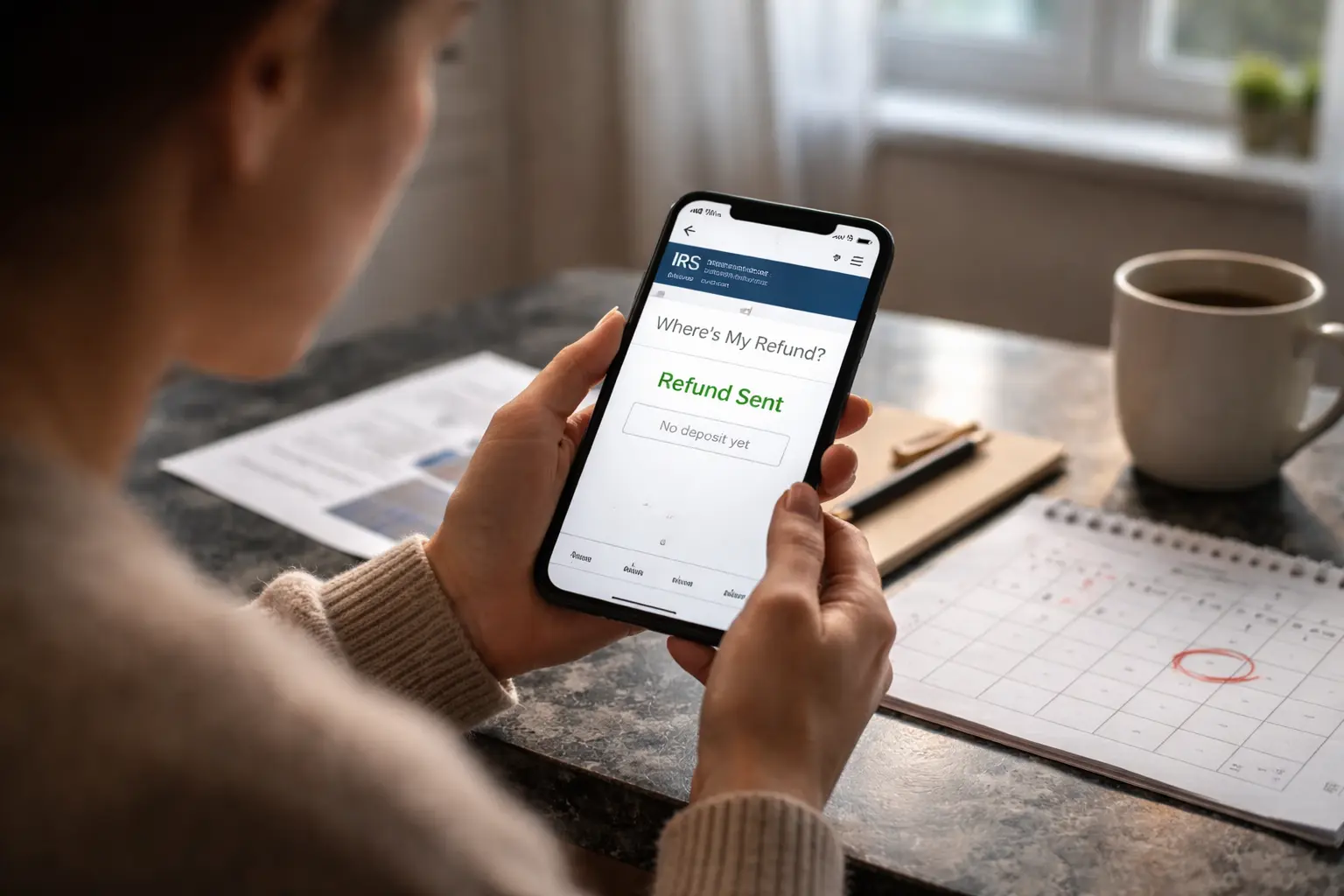

When a $0 Balance Actually Signals a Problem

Most temporary gaps resolve within a standard business cycle. However, you should investigate further if the next full business day passes with no update, your banking details were incorrect, or the payment was offset.

The IRS publishes official refund timing information, and Treasury disbursement guidance is also available for verification. Those are the authoritative sources. If your status shows payment issued and your banking details are correct, timing remains the most common explanation.

The Psychological Side of “Why Not Me?”

Liquidity timing impacts household stress more than most people realize. We have written extensively about how liquidity timing affects stability. When expected money hasn’t landed yet, it triggers pressure even if the delay is structural and temporary.

Modern banking apps expose intermediate stages of processing that older systems never showed customers, which increases anxiety even though it does not mean the system has failed.

What Changes Over the Next Few Hours

If your deposit is in the pipeline, the remaining step is institutional posting. Banks finalize settlement in defined windows, and we explain those cycles in our breakdown of deposit timing updates. That is the stage most people are waiting on right now. Timing, not approval alone, controls availability.

Final Perspective

If you’re seeing reports of $2,000 deposits hitting some accounts today while yours remains unchanged, you are likely watching staggered settlement timing, not exclusion.

Federal payments move in structured waves, visibility spreads unevenly, and the final posting stage is controlled by your bank’s internal schedule. Refreshing your app won’t accelerate settlement, but understanding the system may reduce the pressure.

Author