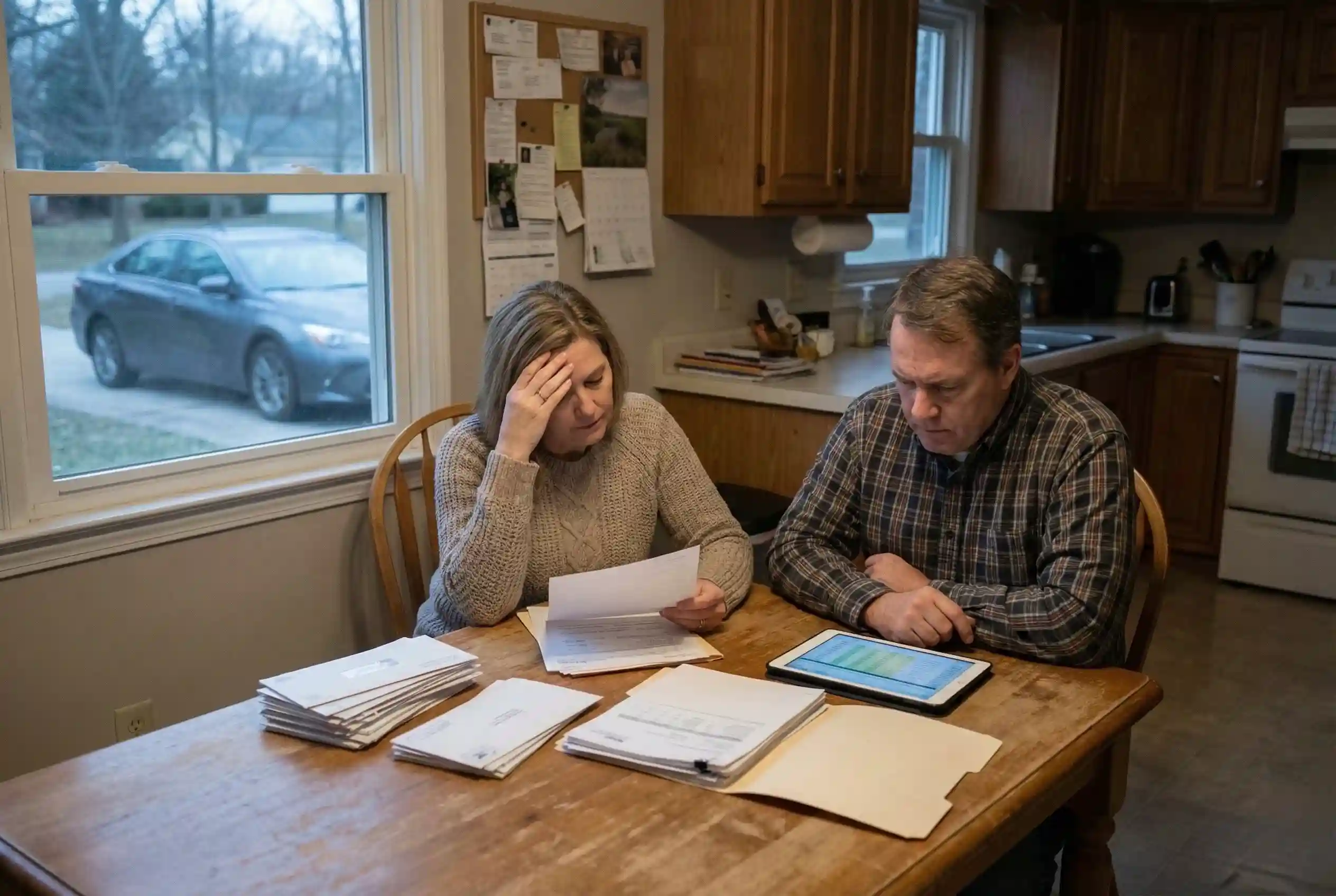

Car insurance prices are rising again in 2025, and many U.S. drivers are feeling the pressure every time their renewal notice arrives. Premiums are climbing because repair costs, medical bills, and severe weather claims are all higher than before.

This guide breaks down what is pushing rates up, which states are seeing the biggest jumps, and the practical steps you can take today to cut your monthly bill. Here’s what you need to know before your next renewal.

- Repair costs for modern vehicles have risen sharply because sensors, cameras, and safety modules are now part of even basic repairs.

- States with more weather events like hail, flooding, and severe storms are seeing the fastest premium increases as insurers adjust for higher risk.

- Drivers with strong credit scores, clean driving histories, and low annual mileage continue to qualify for the biggest savings.

- Usage-based programs are becoming a top discount tool, rewarding drivers who avoid late-night trips, speeding, and hard braking.

What’s Causing Car Insurance Rates to Rise in 2025

Car insurance prices are not rising because of one single issue. It’s a mix of higher repair bills, more severe crashes, rising medical expenses, and weather damage that has increased across many states. Since 2020, the cost of settling even a simple claim has climbed, and insurers are adjusting premiums to cover these larger expenses.

Drivers are seeing this more clearly during renewals because many insurers now update their pricing models faster. These models consider things like part shortages, labor rates, and new car technology. When repair and injury costs stay high for several years, monthly premiums usually move up as well.

You see the same pattern in other financial areas, such as changing savings rates in our guide on bank accounts when the cost structure shifts, pricing shifts too.

For a deeper understanding of how rising costs affect everyday finances, you can also explore our simple guide on low-risk investments. The same economic pressures that impact car repairs often influence broader consumer expenses.

Major Drivers Behind 2025 Price Increases

- Repair bills are climbing fast: Parts, labor, and new vehicle technology cost more, so fixing even a small crash now leads to bigger claim amounts.

- More severe accidents: Distracted driving and larger vehicles on the road make collisions more damaging.

- Weather events causing more losses: Storms, floods, and hail are hitting more states, leading to expensive insurance claims.

- Medical expenses keep rising: Higher hospital and treatment costs mean bodily-injury claims are more costly for insurers.

- Car theft cases increased in many cities: Popular models and keyless-entry vehicles are frequent targets, raising risk ratings.

Simple Breakdown: Why This Matters

When the cost of repairs, medical treatment, and weather damage goes up, insurers have to pay more on each claim. That higher payout is passed on to drivers through rising premiums.

You can see similar patterns in other financial products for example, when savings demand shifts quickly, banks adjust rates as explained in our guide on why banks raising savings rates. The same idea applies here: higher risk leads to higher pricing.

Example: If a bumper repair that used to cost $1,800 in 2019 now costs $3,200 because of sensors, cameras, and labor shortages, insurers must charge more to cover the difference. One small increase like this multiplies across millions of claims nationally.

Higher Repair Costs Are a Big Part of the Increase

Repair costs have climbed steadily since 2020, and this is now one of the biggest reasons car insurance is more expensive in 2025. Modern vehicles use sensors, cameras, and advanced safety parts that make even small repairs costly.

Data from the U.S. Bureau of Labor Statistics shows consistent inflation in the Motor Vehicle Maintenance and Repair index, confirming that repair bills are rising faster than overall prices. Similar cost pressure happens in other financial areas, such as changing bank account fees or shifting savings rates when demand changes.

New technology increases costs even more. A small bumper or mirror repair often requires recalibrating lane sensors or camera systems, turning a simple fix into a much larger bill. Data from the Federal Reserve Bank of St. Louis also shows a clear rise in auto-repair costs since 2020.

Because every repair costs more, insurers raise premiums to match higher claim payouts. Electric vehicles (EVs) add another layer of expense. Their battery systems, wiring, and software require specialized repair shops, and parts are harder to source.

This leads to slower repairs and higher claim totals. These rising costs create the same type of ripple effect seen in safe low-risk investments when the underlying cost increases, consumers end up paying more overall. As long as repair inflation stays high, premiums will reflect it.

Auto Repair Cost Inflation (2020–2025)

Source: FRED (CUUR0000SETD)

Repair Cost Inflation vs. Insurance Impact Table

Repair prices have increased faster than general inflation, and this trend directly affects how much insurers pay out after an accident. Modern vehicles use advanced sensors and electronics, which makes every repair more expensive than it was a few years ago. Data from the U.S. Bureau of Labor Statistics and the Federal Reserve Bank of St. Louis shows clear inflation in auto repair services, which is why premiums continue rising in 2025.

| Factor | How It Increased (2020–2025) | Impact on Car Insurance |

|---|---|---|

| Auto Repair Costs | Up due to sensors, cameras, and nationwide labor shortages | Higher payout per claim |

| Parts & Equipment Prices | More expensive materials and limited supply since 2021 | Premiums rise to match replacement cost |

| EV Repairs | Batteries, wiring systems, and electronics cost significantly more | Higher comprehensive & collision rates |

| Medical Costs | Steady inflation in ER visits, surgeries, and physical therapy | More expensive bodily-injury claims |

Source: Federal Reserve Auto Repair CPI Data | U.S. Bureau of Labor Statistics (BLS)

More Accidents and Severe Claims Since 2020

Accidents have become more severe since 2020, and this has a direct effect on car insurance pricing in 2025. More drivers are distracted by phones, navigation screens, and in-car apps, leading to harder impacts and greater damage.

Data from the National Highway Traffic Safety Administration shows that distraction-related crashes remain a major safety issue, increasing the average cost of each claim. When crashes are more severe, insurers must raise premiums to cover bigger payouts.

Many vehicles on the road today are also larger and heavier, especially SUVs and trucks. Heavier cars cause more damage in even light collisions, pushing claim amounts higher.

These rising expenses work just like changes in other consumer areas when underlying risks grow, pricing shifts. You can see this same pattern in financial products such as personal loans and credit cards when risk scores change.

Bodily-injury claims have also increased because medical care is more expensive than before. When each accident leads to higher hospital or treatment costs, insurers face larger loss totals. As a result, premiums rise to keep up with the new average claim cost.

Weather Damage and Natural Disasters Are Adding Pressure

Weather events are now causing more claim losses, and this is another reason car insurance rates are rising in 2025. Severe storms, hail, floods, and hurricanes have become more frequent, leading to more vehicles being damaged at the same time.

Reports from the Federal Emergency Management Agency show steady increases in weather-related disaster declarations, and that raises the risk level for many states. States like Texas, Florida, Colorado, and Louisiana often see spikes in hail and flood claims, which can total thousands of dollars per vehicle.

When insurers face repeated large losses, they adjust premiums in high-risk areas to balance their payouts. This is similar to how rising risks influence safer retirement planning or investment choices when economic conditions change.

Weather-related claims also take longer to process because repair shops become crowded after big storms. Longer repair times mean higher rental-car costs, which increases total claim amounts. As climate-related damage continues to rise, insurers use higher premiums to keep up with these larger and more frequent payouts.

Main Factors Driving Car Insurance Rates in 2025

Impact level shown as heartbeat-style zigzag line

Rising Medical Costs Increase Injury Claim Expenses

Medical bills have increased across the country, and this directly affects the cost of car insurance. Treatment, ambulance services, and hospital care all cost more today than they did just a few years ago. The U.S. Bureau of Labor Statistics tracks steady inflation in medical services, which pushes up the cost of every injury claim after an accident.

Bodily-injury coverage becomes more expensive when hospitals charge more for emergency visits, scans, and ongoing treatment. Even small injuries result in higher bills, and insurers must adjust premiums to match these higher payouts.

This is similar to changes seen in financial planning topics like tax-efficient investing or emergency funds when basic costs rise, consumers pay more overall. Higher medical inflation also means claims stay open longer because treatment requires more follow-ups and specialist visits.

These longer claim timelines increase total expenses, which is why insurers are raising premiums through 2025. As long as medical care keeps trending upward, injury-related insurance costs will remain high.

Where Car Insurance Is Increasing the Most in 2025

Car insurance prices are rising nationwide, but some states are seeing much larger jumps because of weather risks, accident trends, and repair costs. Data from the Insurance Information Institute shows that states facing more storms and higher crash rates typically experience faster premium increases.

States like Florida, Louisiana, Colorado, and Texas have some of the steepest climbs due to hail, flooding, and hurricane risks. Other states are seeing moderate increases, often linked to higher repair costs or growing cities with more traffic.

These areas may not face major storms but still experience rising payouts from everyday crashes. This pattern is similar to how financial markets respond when risk rises, as seen in topics like stock investing or bonds during uncertain periods.

Location matters a lot because insurers set rates based on risk within your ZIP code. That includes accident history, theft rates, repair costs, and local weather patterns. Drivers living in high-risk zones usually pay more, even if they personally have a clean record.

What You Can Do Right Now to Lower Your Premium

The good news is that there are simple steps you can take today to reduce the cost of car insurance. The first and most effective is to compare quotes from multiple companies because prices vary widely.

Many drivers save hundreds per year just by switching insurers. You can also ask about discounts for safe driving, low mileage, or bundling. These small actions can make a big difference.

Adjusting your coverage can help too. Raising your deductible lowers monthly costs, but only if you can afford it during an emergency. Improving your credit score can also reduce your premium in many states because insurers use credit-based scores when setting prices.

This works the same way your score affects loan options or credit cards. You can also consider usage-based insurance, which uses a small device or app to track your driving habits. Insurers give lower rates to drivers who avoid hard braking, late-night trips, and fast acceleration.

For many people, these programs offer quick savings without changing coverage. Always compare the long-term cost and make sure your plan matches the value of your car.

Pros and Cons of Reducing Car Insurance Coverage

Reducing coverage can save money, but it also creates tradeoffs that most drivers don’t realize until after a loss. The right choice depends on your vehicle’s value, your location, and how much financial risk you can handle. This quick pros and cons breakdown helps you understand when lowering coverage makes sense and when it can create bigger long-term costs.

- Monthly premiums may drop depending on state and vehicle value.

- Higher deductibles can reduce upfront insurance costs.

- Useful for older vehicles with limited resale value.

- Out-of-pocket repair costs can become very expensive after an accident.

- Drivers in high-risk areas face greater financial exposure.

- Lenders may reject reduced coverage for financed or leased cars.

When You Should Not Reduce Your Coverage

Even if prices are rising, there are times when cutting your car insurance coverage is risky. If you drive a new car or have a loan or lease, you usually need full coverage because the vehicle’s value is high. Reducing protection can leave you with large repair bills if something goes wrong.

This works much like reducing coverage in umbrella insurance lower protection can create bigger long-term risks. You should also avoid lowering coverage if you live in an area with high theft, flooding, or heavy traffic.

These conditions raise the chance of a costly accident or weather-related damage. Similarly, if you rely on your car for work or daily travel, having strong coverage gives better financial protection. Drivers with limited savings should be extra careful before cutting coverage.

If deductibles or out-of-pocket costs are too high, a single accident can strain your finances. Building a stronger emergency fund first is a safer approach before making any changes to your policy.

The Bottom Line

Car insurance prices are rising again in 2025 because the cost of repairs, medical care, and weather-related damage continues to move upward across the country. Modern vehicles use more advanced parts, storms are causing greater losses, and medical bills remain high, all of which raise claim totals.

While premiums may stay elevated for much of the year, drivers can still lower costs by comparing quotes, improving credit, reducing mileage, or using telematics programs. Staying informed and reviewing your policy regularly can help you avoid overpaying and keep your budget stable during this period of higher insurance costs.

Methodology

This guide was developed using verified national data and trusted public sources. Inflation and cost trends come from the U.S. Bureau of Labor Statistics and the Federal Reserve Bank of St. Louis, while accident-related insights are based on safety findings from the National Highway Traffic Safety Administration.

Weather-risk information reflects reports from the Federal Emergency Management Agency. All explanations follow U.S. insurance rules and Investozora’s editorial standards for accuracy, clarity, and reader-focused guidance.

Investozora uses only trusted, verified sources. We focus on white papers, government sites, original data, firsthand reporting, and interviews with respected industry experts. When relevant, we also use research from reputable publishers. Every fact is checked against a primary source so readers get clear, accurate, and up-to-date information, and we update our citations whenever official guidance changes.

- U.S. Bureau of Labor Statistics (CPI) – Inflation trends for auto repair, medical services, and consumer prices.

- Federal Reserve Bank of St. Louis (Auto Repair CPI) – Motor Vehicle Maintenance & Repair cost index.

- National Highway Traffic Safety Administration (NHTSA) – Crash data, safety reports, and national traffic trends.

- Federal Emergency Management Agency (FEMA) – Weather disaster declarations and climate-related risk data.

- Insurance Information Institute (III) – National insurance trends, state-level risk factors, and rate research.

Frequently Asked Questions

Author

-

The information on this site is for educational and general guidance only. It is not intended as financial, legal, or investment advice. Always consult a licensed professional for advice specific to your situation. We do not guarantee the accuracy, completeness, or suitability of any content.