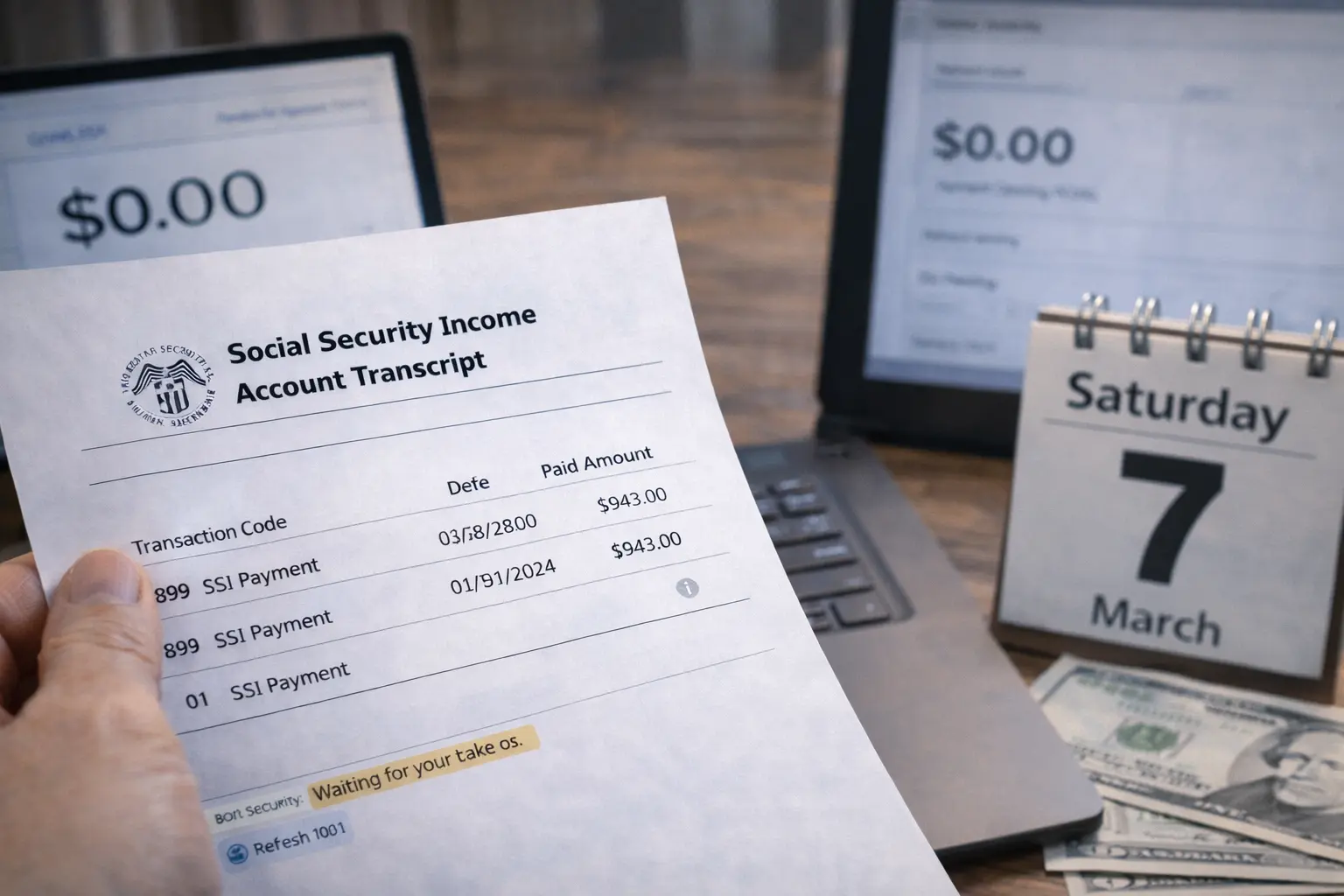

Many people opened their banking apps this morning expecting to see a deposit that was supposed to arrive today. Instead, the balance still shows $0 or the payment appears as pending. For some, the payment portal or government website already says the funds were sent.

This situation is common across the U.S. banking system. When a payment moves through the financial network, it does not become available instantly. The transfer passes through several settlement stages before banks update customer balances.

Understanding how the U.S. money movement system works can help explain why deposits often appear hours after they are officially released.

Direct Deposit Not Posted Today: What People Are Seeing

Across many banks, customers report the same pattern. A deposit is scheduled for today, but the account balance has not changed yet.

Sometimes the payment appears as “pending.” In other cases, there is no visible transaction even though the sender confirms the money was released.

These delays usually occur because payments move through multiple institutional layers before reaching the account. The full process is explained in the broader U.S. money movement infrastructure that governs how funds travel through the national banking network.

Why Deposits Often Arrive Hours After Being Sent

A payment marked as “sent” does not mean the money has finished moving through the system. It only means the sending institution has released the transaction file.

After that step, the payment enters the banking network where clearing and settlement occur. Banks typically process these transactions in batches rather than individually.

That is why many deposits appear later in the morning or early afternoon. The timing depends on when the bank processes the settlement file and updates customer balances.

More detail about this process appears in the explanation of deposit timing and why balances sometimes update after the early morning hours.

How the Federal Payment Pipeline Actually Works

Many government payments follow a structured pipeline before reaching bank accounts. The process usually begins with a federal agency sending a payment file to the Treasury system.

From there the transaction moves through national payment rails such as ACH or other settlement systems operated by the central banking infrastructure. Only after those systems complete processing does the payment arrive at individual banks.

The mechanics behind that movement are outlined in the Treasury system process that governs how federal payments leave government accounts and enter the banking network.

Why Some Banks Update Balances Earlier Than Others

Not all banks update deposits at the same time. Each institution controls its own posting schedule and internal processing rules.

Some banks update accounts immediately after receiving settlement files. Others wait until their next internal processing window before showing the funds as available.

This difference explains why two people receiving the same payment may see it hours apart. The timing depends on each bank’s posting policy and internal systems.

The broader explanation appears in the discussion of bank posting practices and why deposit updates can vary across institutions.

The Role of Settlement Windows in Deposit Timing

The banking network operates on scheduled settlement cycles rather than continuous updates. During these cycles, banks exchange transaction files and confirm balances between institutions.

When a payment arrives just after one of these processing windows closes, it may wait until the next cycle before appearing in the account.

This is one of the main reasons deposits often appear later in the morning. The next processing window allows the bank to finalize settlement and update balances.

The mechanics behind these cycles are explained in the article about settlement windows and how they influence deposit timing.

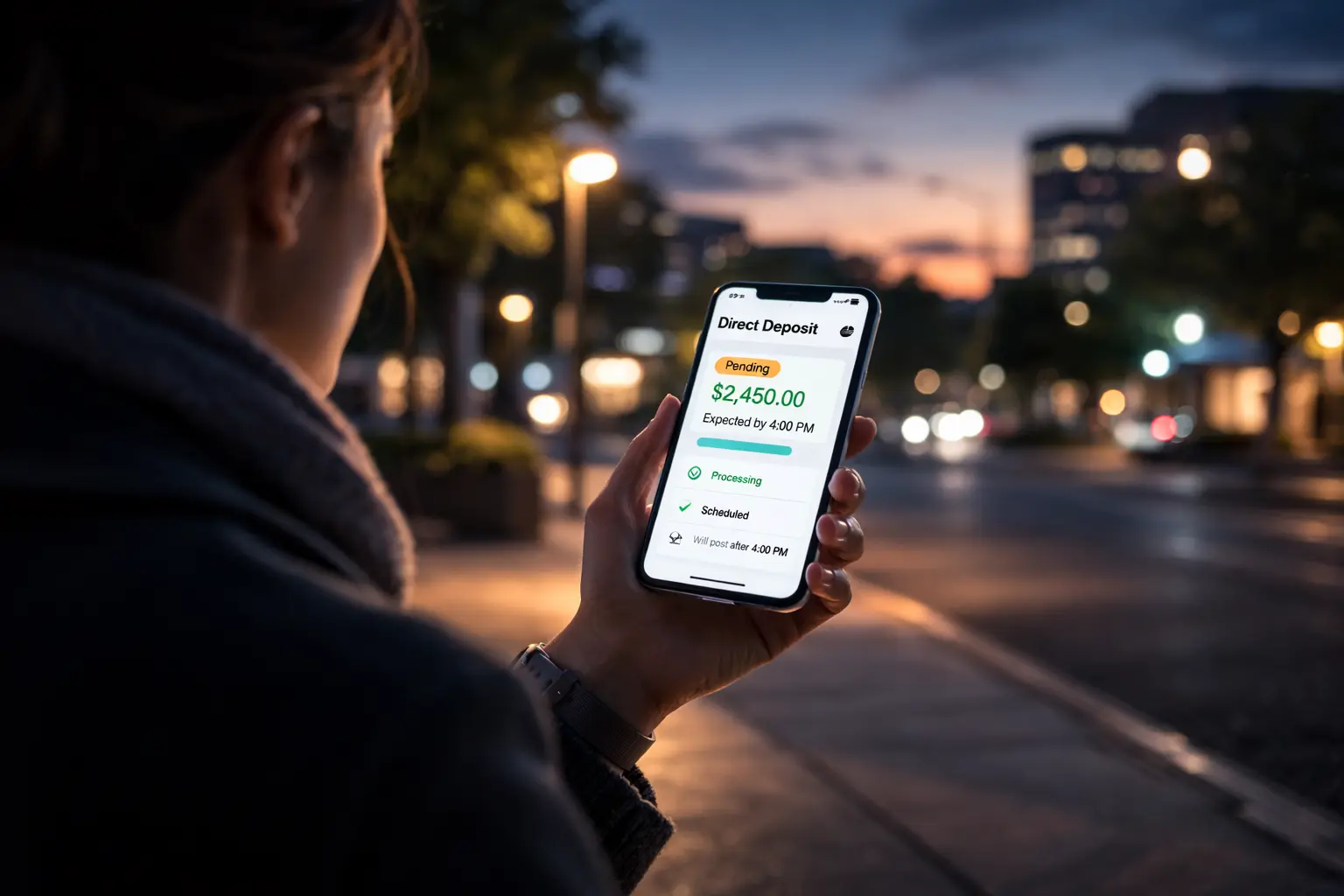

Why Some Deposits Appear as Pending First

Another common situation is when the deposit shows as pending before becoming available. This happens when the bank has received the payment but has not yet completed internal verification.

During this stage, the bank confirms the transaction details and ensures the sending institution’s settlement file clears properly.

Only after these checks does the balance update from pending to available. The early stage of that process is described in the explanation of pending deposits and why they often appear before clearing.

What You Should Check in Your Bank Account Today

If your deposit has not appeared yet, there are several simple checks you can make.

First, confirm the payment status with the sender. Many government payment portals and payroll systems display when funds were officially released.

Next, check your bank’s deposit history. Some banks list incoming deposits as pending before the balance updates.

You can also verify whether the payment arrived after a processing cutoff time. Transactions submitted late in the day sometimes wait until the next settlement cycle before posting.

Additional timing factors are explained in the article on ACH timing and how different transfer types move through the banking system.

What Usually Happens Next in the Payment Cycle

In most cases, deposits appear within the next posting window after settlement completes. This usually occurs later the same day or during the next bank processing cycle.

Banks update balances once they finalize the clearing process and confirm settlement with the sending institution. At that point, the payment becomes available for spending or transfer.

The next stage of that process is described in the explanation of deposit waves, which shows how large batches of payments often reach accounts at similar times.

Understanding Why Your Balance Still Shows $0

Seeing a zero balance while waiting for a deposit can be frustrating. In most cases, the payment is already moving through the financial network even if it is not visible yet.

The delay usually reflects the normal structure of the U.S. banking system rather than a problem with the payment itself.

As settlement cycles complete and banks update their posting windows, the deposit typically appears later the same day. Understanding how funds move through the financial infrastructure helps explain why the process often takes several hours rather than happening instantly.

Author