At 7:12 AM, the coffee is brewing. The phone is already in your hand. You open your banking app expecting to see your paycheck, tax refund, or transfer. The number hasn’t changed. No alert. No update. Just yesterday’s balance staring back at you.

For a few seconds, your mind runs ahead of the facts. Was it delayed? Did something go wrong? Did the bank hold it? If your deposit is not there this morning, the answer is usually far less dramatic, and far more procedural. U.S. banks do not begin their day when you wake up. They operate on settlement windows that started hours earlier.

Overnight, Automated Clearing House (ACH) files move between institutions, following the NACHA processing schedule. Employers submit payroll batches. Treasury releases authorized payment files. But those files still have to clear internal processing windows before balances visibly change inside consumer apps.

Why Your Deposit Looks Late Even When It’s Already Moving

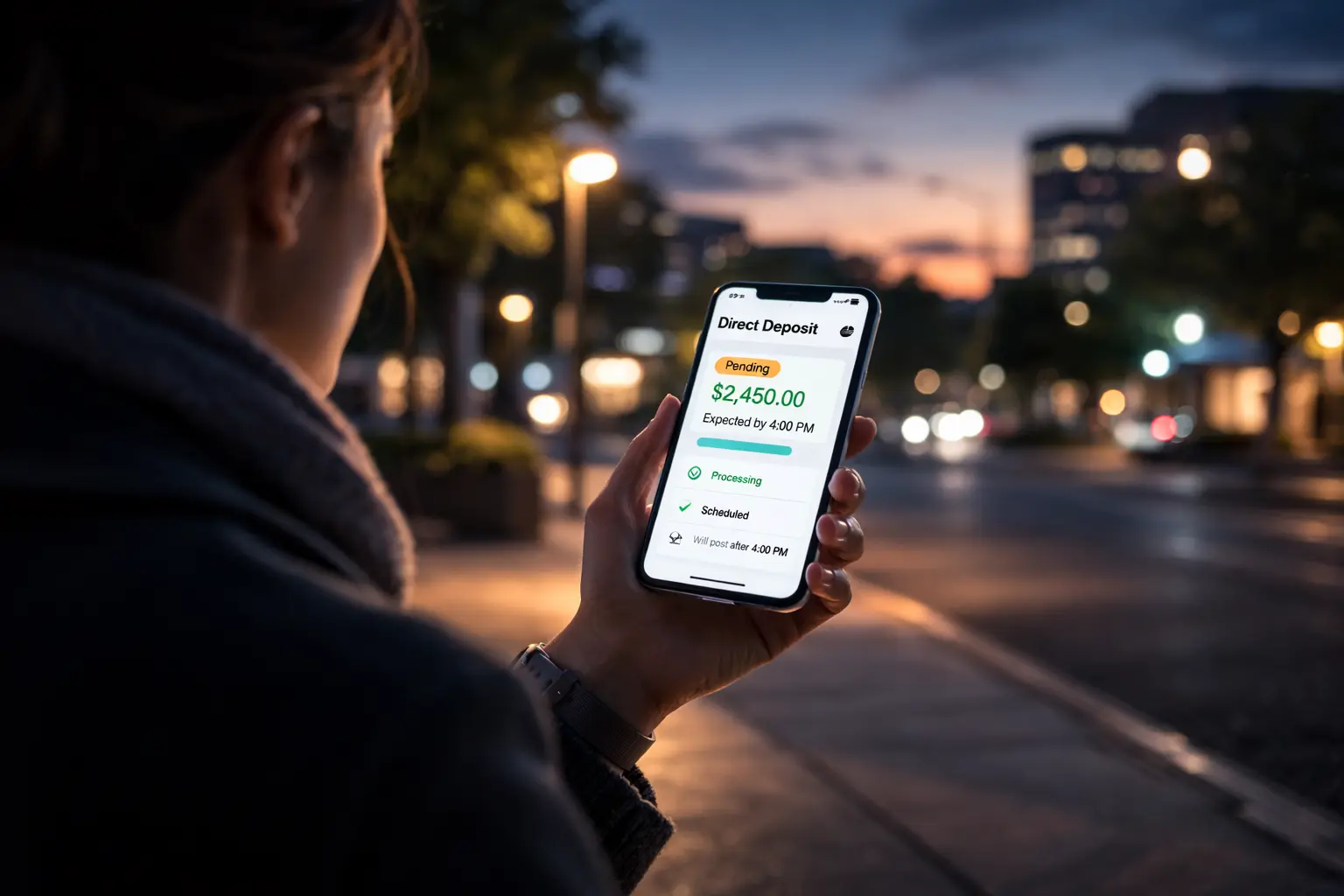

The key distinction is between authorization and posting. Authorization means the payment has been approved and transmitted. Posting means your bank has fully reconciled and reflected it inside your available balance. Those are not the same moment.

Most retail direct deposit timing moves through ACH batch cycles. While ACH operates multiple windows during business days, final posting inside your bank often depends on internal ledger sequencing. Some banks update visible balances between 6:00 AM and 9:00 AM Eastern Time. Others stagger updates throughout the morning.

The Morning Processing Gap That Makes Deposits Feel Delayed

That gap, sometimes only an hour or two, creates the emotional friction many households feel. Consider a typical payroll scenario. Your employer submits payroll Thursday afternoon. The ACH file settles overnight. Technically, funds are in motion. But your bank may process incoming credits in priority order early Friday morning. Until that ledger reconciliation completes, your app may still show yesterday’s balance.

The money is not missing. It is mid-sequence. This is the same structural timing discussed in liquidity timing mechanics and direct deposit posting cycles. Payment rails move in layers: file transmission, clearing, posting, and final availability. Morning visibility sits at the end of that chain.

There is also an internal risk component. Behind the scenes, banks manage liquidity buffers and reconcile inbound files before reflecting available balances. In doing so, this ensures that credits are verified against clearing instructions. Occasionally, files can be flagged for review; however, the overwhelming majority simply wait their turn in the posting queue. As a result, what feels personal is usually operational.

If your deposit is not there this morning, watch the clock

Meanwhile, another common confusion happens when deposits show as “pending” late at night. In many cases, banks pre-notify customers of expected credits ahead of final ledger updates. Because of this, that preview can create a psychological expectation that the balance will be there the moment you wake up. In reality, preview does not equal settlement.

If your deposit is not there this morning, watch the clock. Between 7:30 AM and 10:00 AM Eastern Time, most institutions finalize overnight batches. Treasury disbursements, payroll credits, and internal transfers typically post during that window on standard business days. Weekend slowdown and federal holidays shift this timing further, compressing updates into the next operating morning. This ties into the broader US money movement system.

The emotional cycle is predictable. Early morning: confusion. Mid-morning: update appears. Relief follows. Understanding that rhythm changes how the experience feels. The U.S. payment system is not built for emotional immediacy. It is built for structured finality. Files clear. Ledgers reconcile. Balances update.

When you see no change at 7:12 AM, it’s usually not because anything is wrong — rather, it’s because you’re simply ahead of the processing window. In other words, while the transfer has already been initiated, the system hasn’t yet reached the posting cycle. As a result, the balance appears frozen.

How Often This “Missing Deposit” Moment Actually Happens to Households

This gap, therefore, between when money actually moves behind the scenes and when you visibly see it update is precisely what defines modern liquidity timing. By mid-morning, in most cases, the number changes quietly. No announcement. No alert explaining the mechanics. Just a balance update that makes the earlier worry feel unnecessary. The system did not pause. It followed its schedule.

Author