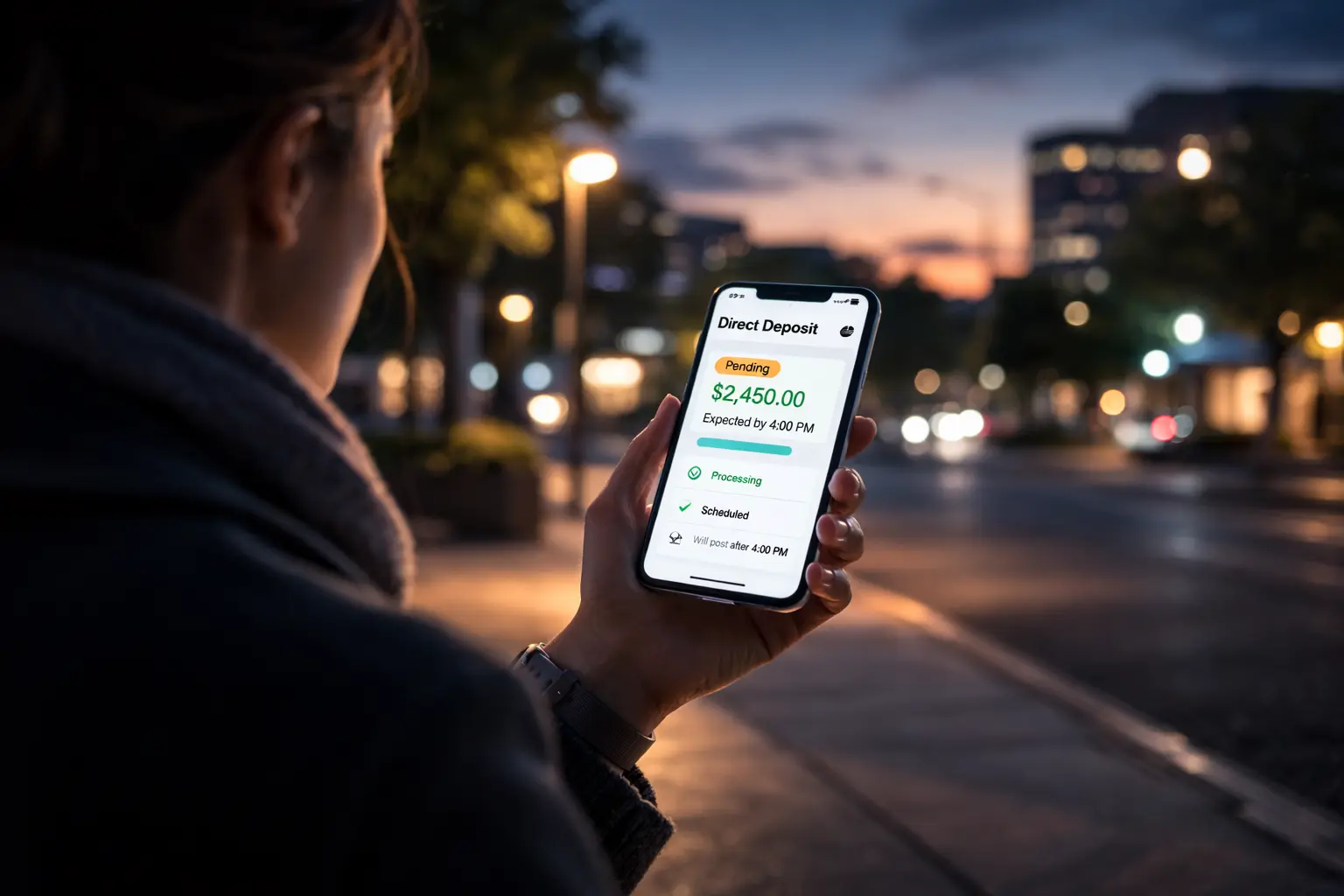

The experience of checking a mobile banking app to find a scheduled federal payment listed as “Pending” while the “Available Balance” remains unchanged is one of the most significant sources of financial anxiety for millions of Americans.

As of Tuesday evening, February 24, 2026, social media platforms and banking forums are already filling with reports from beneficiaries born between the 21st and 31st of any month who are expecting their Social Security birth-date wave deposits tomorrow morning.

This specific phenomenon is not a bank error or a sign of a failed transfer, but rather a visible symptom of the structured delay between information transmission and final reserve settlement.

Why ‘Pending’ Balances Don’t Always Match Your Available Cash Today

When you see a “Pending” transaction in your ledger today, you are looking at a memo-post created by your bank’s front-end system. Your financial institution has received a high-speed data file from the Federal Reserve, signaling that funds are authorized to arrive.

However, the actual “liquidity” or spendable cash does not move in real-time. Instead, it follows the rigid Federal Reserve settlement windows that dictate when institutional reserves actually shift from the Treasury’s account to your bank’s ledger.

Until that settlement window closes, usually in the early morning hours of Wednesday, February 25, the bank may show you the “intent” to pay without granting you access to the cash.

This disconnect is deeply rooted in the settlement window timing that governs the U.S. financial system. Most traditional banks wait for the “Final ACH File” to clear through the Fedwire system before they move funds from a pending state to a usable state.

This is why a coworker at a fintech or a credit union might have access to their funds at 6:00 AM, while a customer at a major national bank might not see their balance update until the 8:00 AM to 9:00 AM window.

The tension users feel tonight is effectively the “Settlement Gap,” a period where the data has arrived but the money is still technically moving through the U.S. money movement system.

The Wednesday Wave: IRS Code 846 and Social Security Coordination

For those expecting IRS refunds alongside Social Security payments tomorrow, the timing is even more precise. The Bureau of the Fiscal Service often batches these payments for a “Wednesday Effective Date.” If you are tracking a “Code 846” on your tax transcript, your bank is currently holding that instruction in a digital queue.

Because of the high volume of transactions expected on February 25, some banking servers may experience “Update Lag,” where the app shows the deposit as “Received” but the internal logic of the Treasury Payment System hasn’t triggered the final balance release.

Furthermore, today marks a critical transition in the broader economy as the new Section 122 Global Tariff officially went into effect at 12:01 AM on February 24. While seemingly unrelated to your paycheck, these macro-events can cause banks to tighten their liquidity and holiday settlement protocols to account for increased institutional volatility.

This can result in slightly longer processing times for non-real-time ACH batches as banks verify reserve levels before releasing massive payout waves to the public. If you find yourself staring at a “Pending” notification tonight, the most important thing to understand is that your deposit is likely secure and simply awaiting the 12:01 AM institutional handoff.

The synchronization between Fedwire and ACH liquidity timing ensures that by the time the West Coast wakes up tomorrow, the vast majority of these “Ghost Balances” will have converted into actual, spendable liquidity. Understanding this mechanical rhythm can transform the frustration of a “pending” screen into a predictable part of your monthly financial cycle.

Author