Many people woke up today to a familiar situation. A government portal or banking alert shows a federal payment marked sent, yet the bank balance still shows zero.

For many households waiting on a tax refund, Social Security payment, or other federal transfer, that message creates confusion. If the payment was sent, why is the money not available?

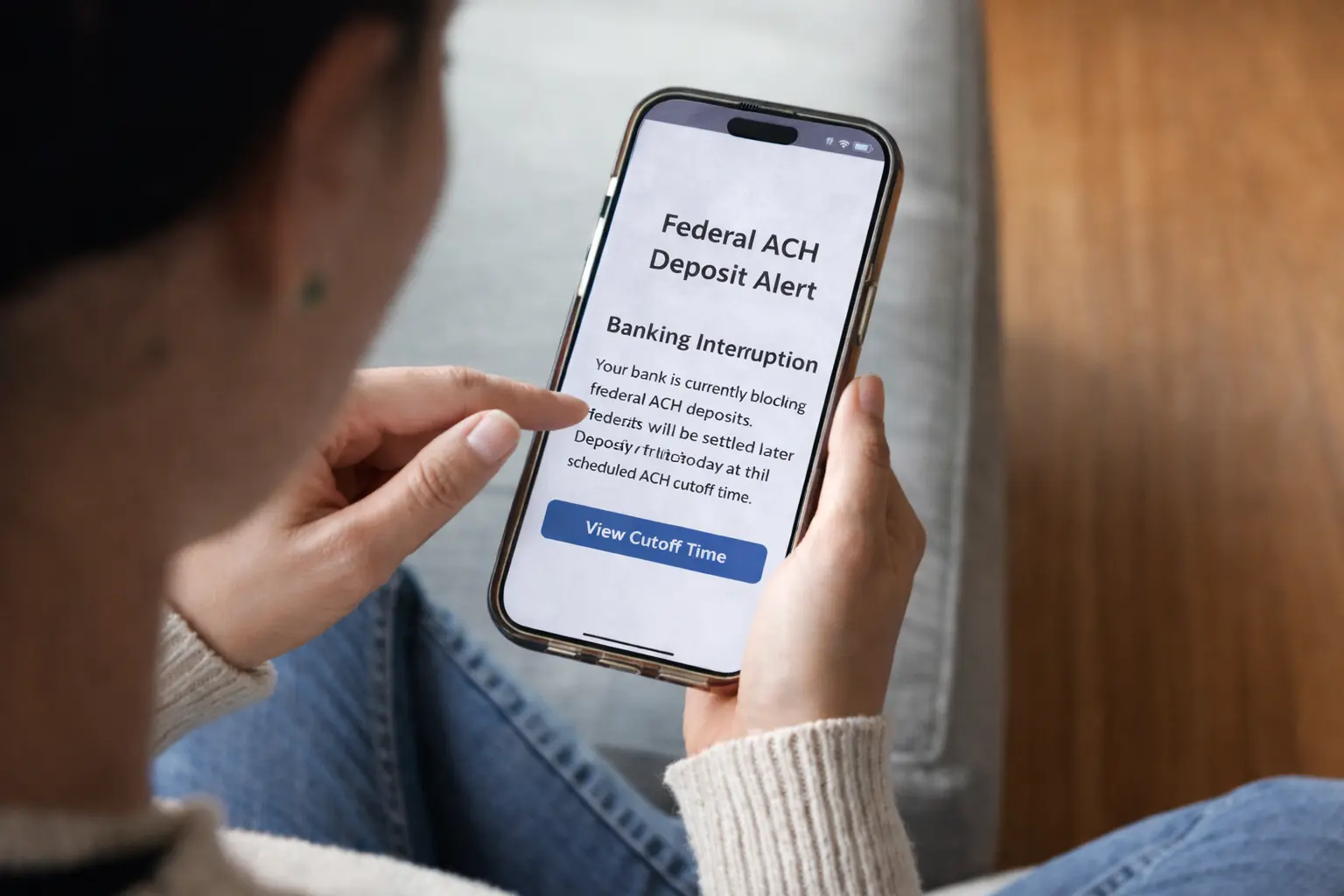

The short answer is that the message “sent” does not mean the money has fully moved through the banking system. It simply means the payment has entered the national payment network that moves funds between institutions.

The remaining steps happen inside the infrastructure that powers the broader U.S. financial system. Understanding that pipeline explains why deposits often arrive hours later even after the payment status shows completed.

Federal Payment Marked Sent: What People Are Seeing Today

Across the country, banking apps are displaying a common pattern. Government portals report payments as sent, but bank balances have not updated.

This situation often appears during large federal payment cycles. Treasury payments, IRS refunds, and Social Security benefits all move through the same banking rails before reaching individual accounts.

When a status says sent, it typically means the payment file has left the government agency. The funds are already moving through the banking network, but they have not reached the final posting stage yet.

Many of those payments are still traveling through the Treasury pipeline described in Treasury flow processing.

Why a Sent Payment Can Still Take Hours to Arrive

The word “sent” refers to the moment a payment file leaves a federal system. It does not represent the moment the money appears in your account.

After the payment is released, the transaction must move through the national banking settlement process. This includes routing through the clearing systems used by financial institutions.

Many government transfers move through the automated clearing system described in ACH timing infrastructure. That system processes large batches of payments throughout the day rather than instantly.

Once a payment enters those settlement cycles, banks must verify, clear, and prepare the deposit before it becomes available.

How Federal Payments Move Through the Banking Network

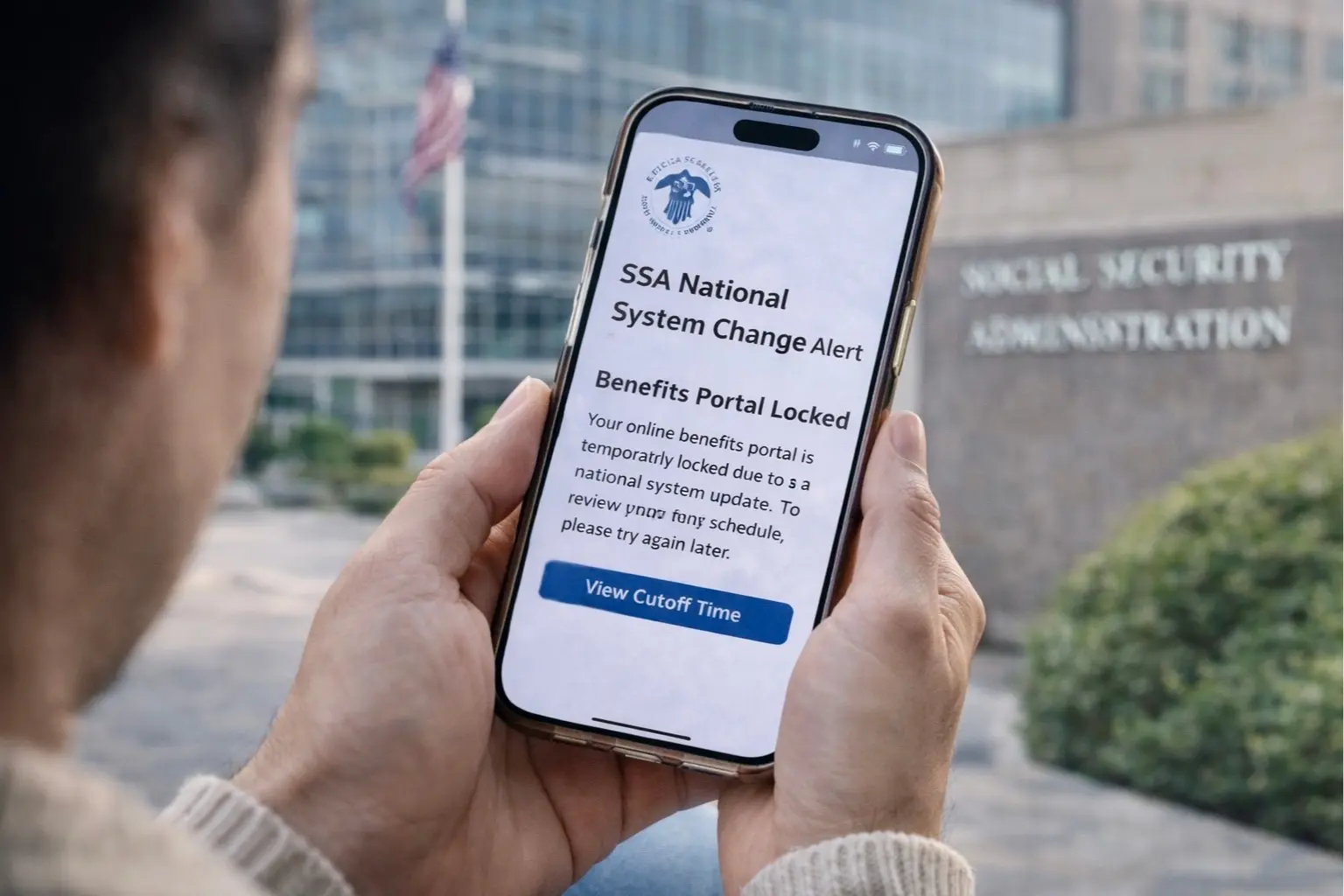

Federal payments begin inside government systems such as the U.S. Department of the Treasury. The Treasury distributes funds for agencies including the IRS and the Social Security Administration.

Once the payment is approved, the Treasury releases a payment file to the national banking network. At that point the payment enters clearing systems operated by the Federal Reserve.

From there the transaction moves toward the receiving bank. This stage is where payments often appear as pending deposits, a situation explained further in pending deposits behavior.

The bank then prepares the deposit for the next available posting window.

How Federal Agencies Release Payments

Federal payments do not leave government systems randomly during the day. Agencies typically release payment files through the U.S. Department of the Treasury’s official payment platform, which distributes funds to banks across the country.

Once the Treasury transmits the payment instructions, those transactions move into the banking network for clearing and settlement. The process is outlined by the U.S. Department of the Treasury’s Bureau of the Fiscal Service, which manages federal payments nationwide

Why Bank Posting Times Differ Across Institutions

One of the most confusing aspects of direct deposits is timing. Two people expecting the same payment can receive it at different times.

This difference happens because each bank operates its own posting schedule. Some institutions update accounts early in the morning, while others post deposits later in the day.

These posting cycles are commonly known as settlement windows, a process explained in settlement window timing mechanics. A payment can arrive at the bank hours before the bank actually updates customer balances.

Why Deposits Often Appear in Waves

During major payment events, deposits rarely arrive simultaneously across all banks. Instead, deposits appear in waves throughout the day.

Large federal payment releases can involve millions of transactions moving through the banking network. Each institution processes those transactions in stages as liquidity moves through the system.

This wave pattern is why some people see deposits early while others wait until later in the afternoon. Recent deposit cycles have shown similar patterns during events described in deposit wave coverage.

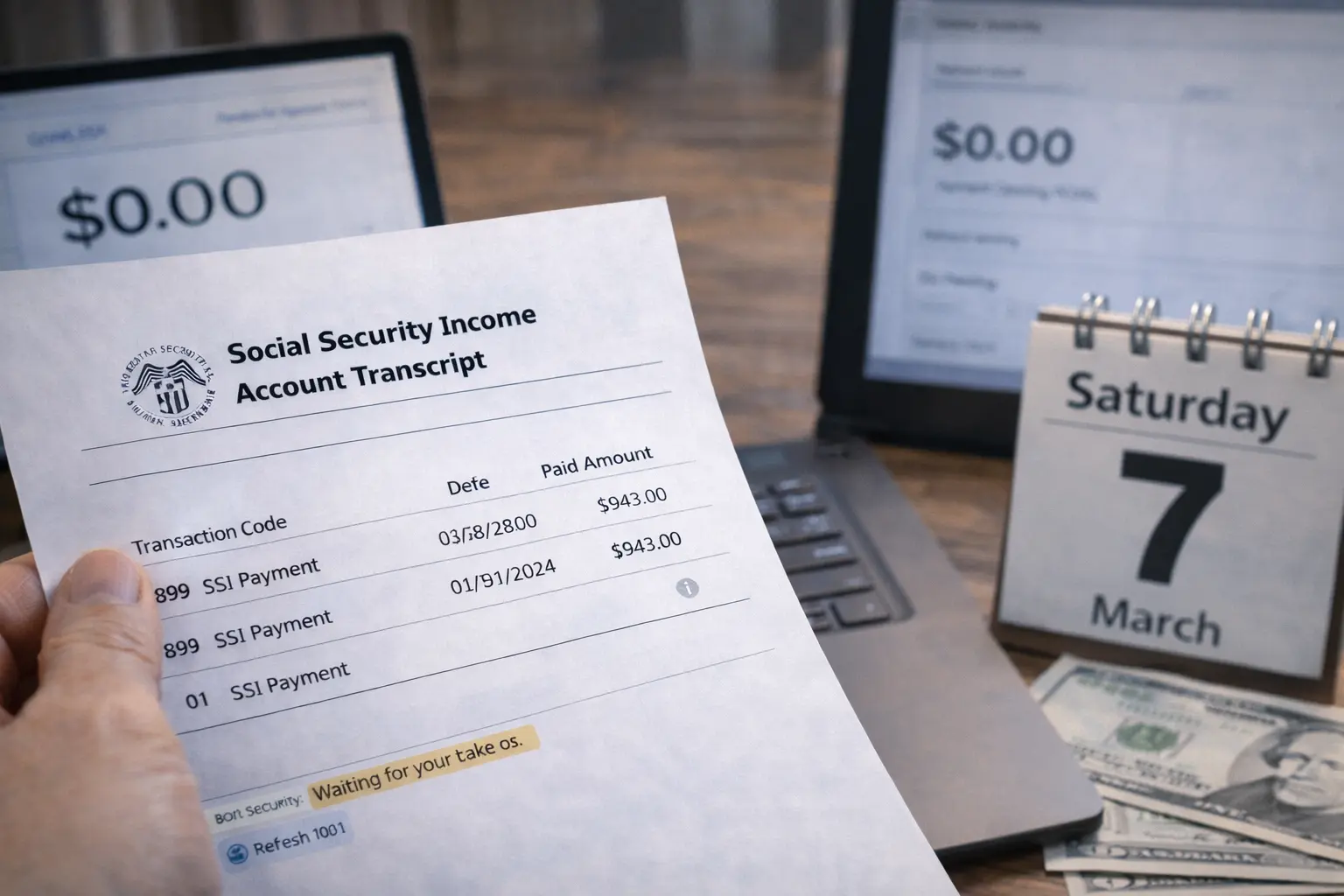

What to Check If Your Deposit Has Not Arrived

If your payment shows sent but the balance has not updated, there are a few things worth checking.

First, look for any pending deposit indicators in your banking app. Many banks show incoming payments before the funds become available.

Second, verify the payment date shown by the government portal or payment notice. Some deposits are scheduled for the next processing cycle rather than immediate posting.

Third, remember that overnight clearing cycles can affect timing. Payments released late in the day may not complete bank posting until the next morning. This pattern occurs frequently during overnight clearing cycles.

What Usually Happens Next in the Payment Cycle

Once a payment reaches the receiving bank, the final stage usually happens quickly. The bank completes internal verification and releases the deposit into the customer’s account.

In many cases this final step happens during the next posting window. That is why deposits often appear suddenly during early morning or midday account updates.

For many payments marked sent today, deposits may arrive during the next scheduled bank update cycle. These updates frequently occur between early morning and late afternoon depending on the institution.

Understanding the underlying deposit timing process helps explain why balances change at different hours.

Understanding What “Sent” Really Means

The phrase federal payment marked sent simply indicates that the government has released the payment into the financial system. It does not mean the funds have fully completed their journey through the banking network.

Between the moment a payment is released and the moment it appears in a bank account, several systems handle the transaction. These systems move funds through clearing networks, bank settlement windows, and posting schedules.

For most people waiting on a payment today, the deposit is already in transit. The final step is simply the bank’s posting process, which often completes later the same day or during the next processing cycle.

Understanding that process removes much of the uncertainty. What appears to be a delay is often just the normal timing of the financial infrastructure that moves trillions of dollars every day.

Author