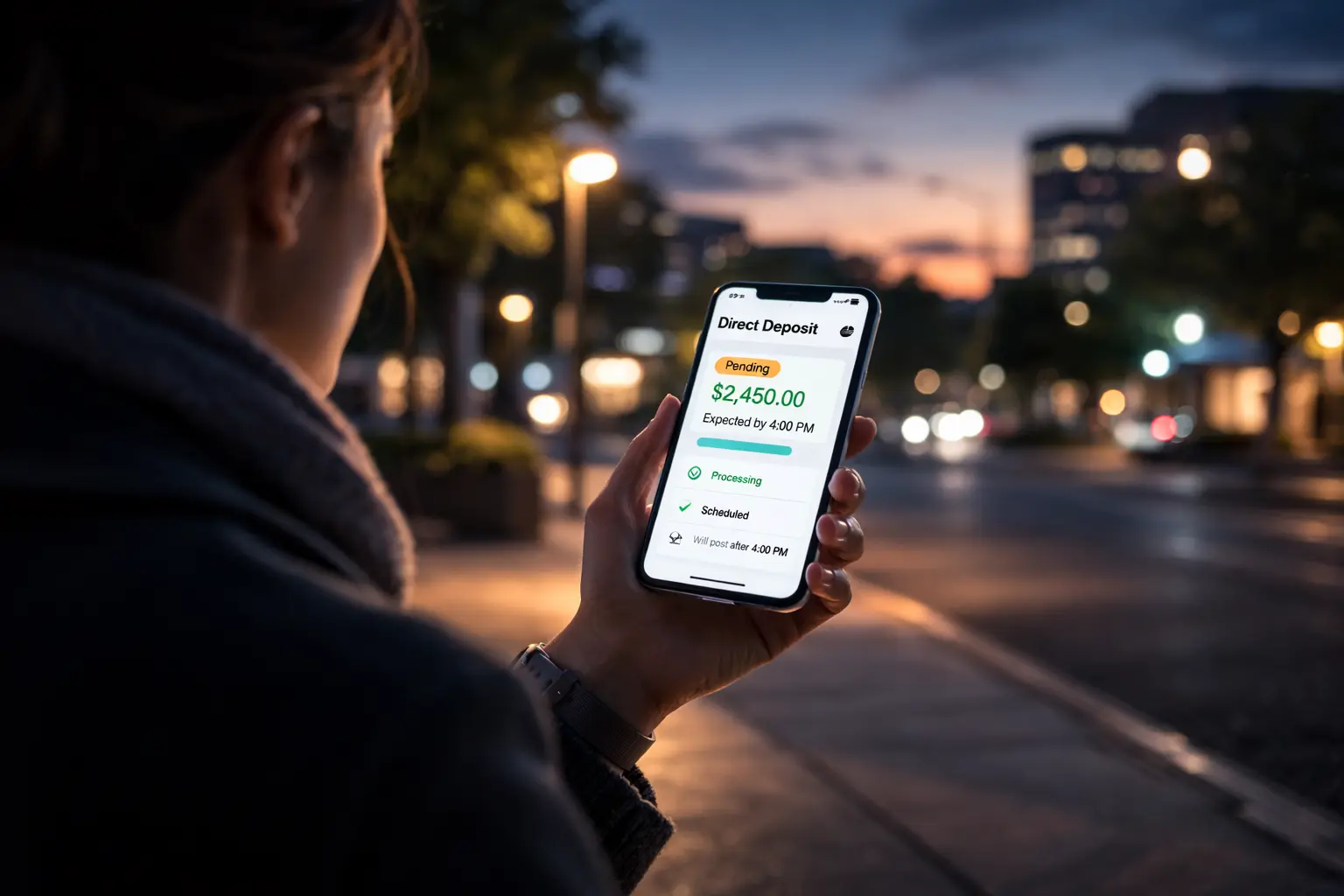

At 7:13 AM on Friday, a phone screen refreshes. The paycheck is not there. The balance looks unchanged.

Across payroll-heavy Fridays, this moment repeats millions of times before the final ACH window closes. Questions often center on a Friday direct deposit cutoff, especially on high-volume payroll and federal benefit disbursement days. The assumption is delay. The reality is sequencing inside a structured settlement chain.

Once the final ACH submission window closes, the system does not pause. It transitions into weekend rollover coordination.

The Final ACH Window and the Clearing Queue

Automated Clearing House files move through defined submission tiers. Standard next-day files close earlier in the afternoon. Same-day ACH windows extend later into the evening Eastern Time.

When the last eligible file enters the queue, hierarchy shifts. Files received before cutoff move into settlement preparation. Files received after cutoff move into the next processing day. On active payroll Fridays, millions of transactions flow through these windows before the weekend ledger pause fully engages.

The National Settlement Service calculates multilateral net positions across institutions. Those calculations affect reserve accounts rather than customer balances. The Federal Reserve details these operational phases within its ACH services framework.

Clearing does not equal posting. Settlement does not equal visibility. For a system-wide explanation of how these layers interconnect, see our analysis of the national payment system.

Ledger-Day Rollover and Reserve Positioning

Friday introduces a defined mechanical break inside bank ledgers. Institutions close their internal ledger day before the weekend. That closure separates Friday’s settlement obligations from Monday’s opening balances.

Fedwire Funds Service closes at 7:00 PM ET and reopens at 9:00 PM ET for the next processing day. This two-hour interval forms a rollover boundary between ledger days. Reserve accounts must reconcile before rollover completes. This is balance sheet discipline.

Federal payroll routing follows structured sequencing before retail visibility appears. The Bureau of the Fiscal Service outlines how federal disbursements enter reserve settlement frameworks. Readers can review the official Gold Book directly through the appropriate U.S. government source.

Institutional balances update first. Retail ledgers follow after internal verification completes. Our examination of reserve settlement timing explains how reserve positioning shapes visible posting.

The 8:00–9:00 AM Posting Window

Retail systems rarely update in real time. Most institutions finalize visible credits during an early-morning synchronization cycle. On large payroll Fridays, the highest posting concentration often occurs between 8:02 AM and 8:47 AM Eastern. That interval reflects reconciliation density.

Overnight batch reconciliation completes before sunrise. File integrity checks finalize. Liquidity thresholds clear. Between 8:00 and 9:00 AM ET, reserve confirmation data synchronizes with core banking systems. This morning posting cycle marks the convergence point between federal settlement and retail visibility.

If a payroll file misses Friday’s final window, settlement shifts to Monday’s cycle. Even when reserve entries process late Friday evening, many banks defer retail posting until the next 8 AM verification period.

Intraday Liquidity and Exposure Controls

Another structural layer activates quietly after cutoff: exposure management. Banks frequently extend provisional credit before final reserve confirmation to support continuity. This introduces provisional credit risk.

On Fridays, exposure thresholds tighten. Weekend liquidity cannot be replenished through routine same-day operations. If a file arrives near cutoff, some banks restrict early posting until full reserve confirmation clears, often leaving a pending deposit status visible to the user.

The National Settlement Service finalizes multilateral obligations. Core systems reconcile those figures against internal liquidity metrics. Posting follows verified settlement alignment to ensure available balance mechanics remain accurate.

Weekend Compression and Monday Reentry

After ledger rollover completes, the system compresses into weekend configuration. Standard next-day ACH settlement pauses until the next business cycle. Files queue for Monday processing.

When Monday’s full processing cycle begins, reserve balances realign. Retail posting follows the established 8:00–9:00 AM synchronization window.

Returning to the Screen

By Monday morning, the balance refreshes again. The funds were never missing. They were sequenced within a Friday direct deposit cutoff boundary. Federal settlement, reserve verification, and ledger rollover defined the timing of visibility.

Liquidity moved according to coordinated institutional systems. When a balance appears later than expected, the explanation usually lies inside structured settlement mechanics.

Author