The global financial system moves trillions of dollars across borders every day. Yet many international transfers still take hours or even days to settle.

Regulators now warn that the effort to modernize those payment rails may be moving more slowly than expected. Officials involved in the reform program say progress toward faster and cheaper cross-border transfers is uneven across banking networks.

Many institutions continue relying on legacy settlement infrastructure that processes transactions in stages before funds reach the final account.

The same mechanics that slow international transfers also shape how funds move through the domestic U.S. money movement infrastructure, where settlement timing often determines when deposits become available in bank balances.

Global Reform Effort Faces Slower Implementation

The international plan to modernize payment systems was designed to reduce transfer costs and accelerate settlement times by 2027.

The initiative is coordinated by organizations including the Financial Stability Board and the Bank for International Settlements, with regulators outlining the goals of the global payment reform in the official payment modernization roadmap published by the Financial Stability Board.

Regulators say progress depends heavily on how quickly banks upgrade their internal systems. Many institutions still rely on batch-based clearing models that process large groups of transactions at scheduled intervals.

This type of structured processing also appears in domestic banking networks. Deposits often move through settlement stages before becoming available, which explains why many transfers show a pending deposit status before final posting.

Cross-Border Payments Still Depend on Intermediary Banks

International transfers rarely travel directly between two financial institutions. In many cases, payments pass through multiple correspondent banks before reaching the receiving account.

Each intermediary bank must verify liquidity, perform compliance checks, and reconcile transaction files. These safeguards protect financial stability but also add additional processing time.

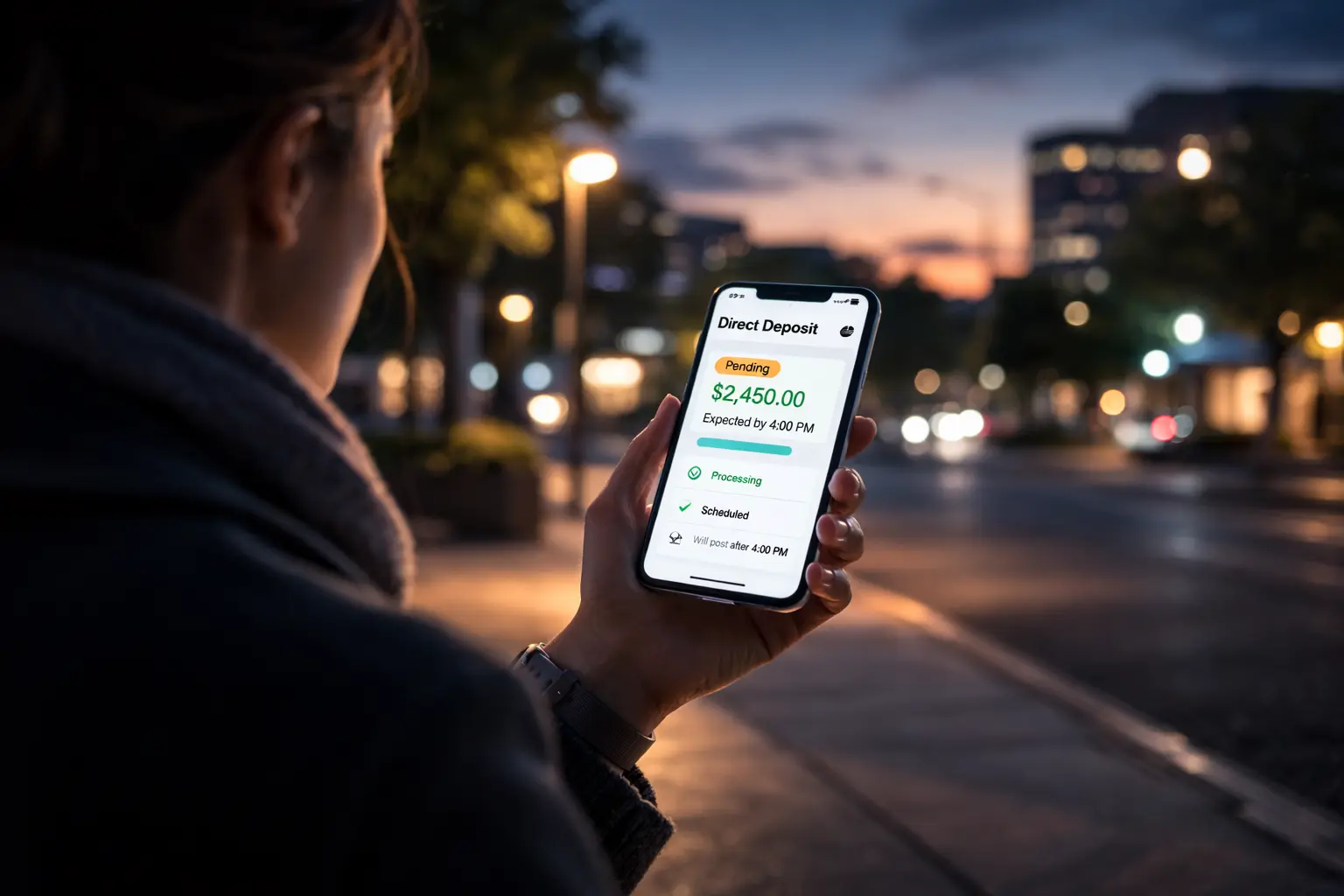

Domestic payment systems operate under similar timing constraints. Settlement windows and batch processing cycles determine when funds appear in accounts, a pattern frequently seen in deposit waves that update balances at different hours of the day.

Fintech Networks Push for Faster Settlement

Financial technology firms are developing new payment platforms designed to reduce settlement friction. Many of these systems rely on real-time processing that eliminates several intermediary steps.

Advocates argue that modern payment rails could allow transfers to settle within minutes rather than hours. These technologies aim to provide clearer transaction tracking and faster liquidity confirmation.

Traditional banks remain cautious. Payment infrastructure must still comply with regulatory controls and settlement rules similar to those governing ACH timing within the existing financial network.

The Future Control of Global Payment Rails

The push to modernize international transfers is about more than speed. The outcome may determine who controls the next generation of global financial infrastructure.

Banks, central banks, and fintech platforms are all competing to shape how money moves across borders in the future. Each approach offers different advantages in terms of stability, transparency, and settlement efficiency.

For consumers and businesses, the outcome will influence how quickly payments travel through the banking system. The same structural forces already affect everyday deposits and transfers, including the timing patterns explained in bank posting schedules across U.S. financial institutions.

Author