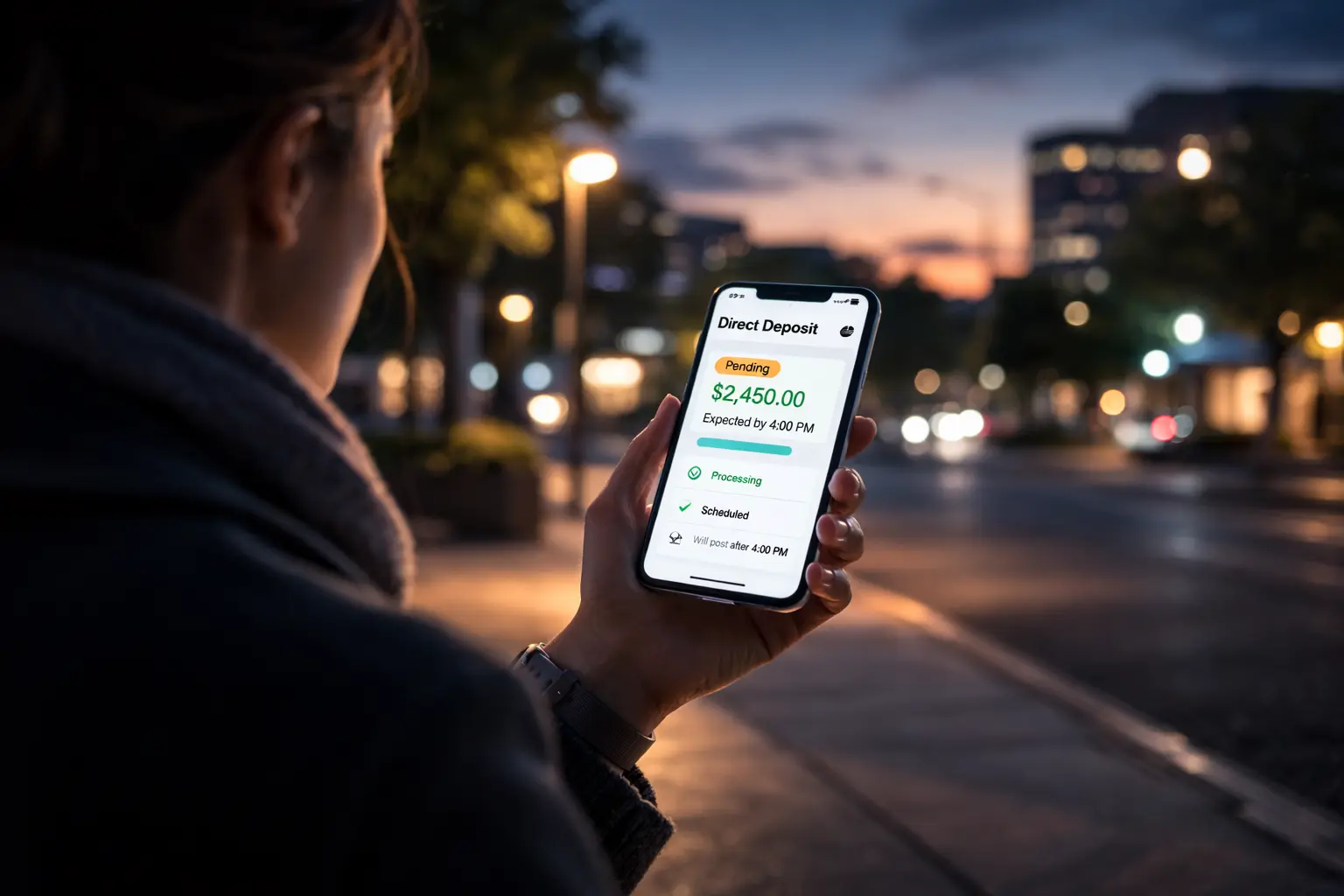

At 8:12 AM, the phone screen looks unchanged. The paycheck shows as pending. The available balance does not move. It feels like the money exists. but not for you. It feels like your paycheck arrived but you still cannot use it. That tension reflects a structural sequence inside the banking system. It does not reflect error. It does not reflect neglect. And it reflects timing. A pending credit signals acknowledgment. It does not confirm synchronized liquidity.

Pending Means Acknowledged, Not Settled

Most payroll and federal payments move through the ACH network overnight. Employers transmit files in the afternoon. Banks release them into clearing queues aligned with Federal Reserve processing cycles.

ACH operators calculate net debit and credit positions through the National Settlement Service before banks adjust master account balances. Only after that reconciliation can reserve balances change. Readers can review the official documentation directly through the appropriate U.S. government source at FRB Services.

That sequence prioritizes system integrity over retail immediacy. Your bank may receive the file at 2:14 AM. Your app may show “pending” at 6:02 AM. Yet final reserve confirmation can lag behind visible acknowledgment. Understanding this hierarchy clarifies how the broader U.S. money movement system separates instruction receipt from usable funds. The system does not stall. It sequences.

Early-Morning Reserve Verification

Between roughly 6:30 and 8:00 AM ET, treasury operations teams perform reserve verification. This layer rarely appears in consumer explanations.

Each commercial bank maintains a master account at its regional Federal Reserve Bank. Overnight ACH settlement alters that reserve position. Before retail posting begins, treasury desks confirm that net credits have finalized and that projected daylight liquidity remains within limits. This ensures the bank does not exceed intraday exposure caps before releasing retail funds.

If liquidity compresses, treasury desks may reposition balances through short-term funding channels before customer accounts update. Fedwire reopened at 9:00 PM ET the prior evening. Large-value transfers processed overnight can shift reserve positioning before dawn. Readers can review the official documentation directly through the appropriate U.S. government source at Fedwire Funds.

Retail customers do not see this choreography. Yet it determines when “pending” becomes usable.

The 8:00–9:00 AM Posting Window

Most major banks finalize deposit posting during the settlement window between 8:00 and 9:00 AM ET. That window reflects the moment verification concludes and internal ledgers synchronize.

Posting earlier increases institutional exposure. Posting later undermines customer confidence. Banks calibrate carefully. Overnight ACH batches typically settle before retail systems allocate credits to individual accounts. This explains why deposits often appear in clusters and why you might see a balance update just as the business day begins.

Our deeper review of ACH timing shows how batch hierarchy influences visible posting order.

Ledger-Day Rollover

Core banking systems close one ledger day and open another through automated rollover routines. That rollover often completes before sunrise, but it still depends on upstream settlement alignment.

If rollover completes before final ACH confirmation, balances can temporarily reflect prior-day liquidity. When reserve confirmation arrives, the ledger updates again. That distinction becomes more visible during high-volume periods such as tax season.

Our structural analysis of Treasury sequencing shows how federal disbursements enter clearing channels before retail availability. The household sees one static figure; the institution manages multiple synchronized ledgers.

Provisional Credit and Exposure Caps

Some banks extend provisional access before final settlement. They do so within internal limits to manage early deposit risk.

Predictive settlement models assess historical reliability of payroll and federal credits. When expected inflows match projected reserve positions, banks may release funds early. If inflow volatility increases, perhaps due to a missed ACH cutoff, provisional posting tightens.

Why the Screen Feels So Personal

Outgoing payments post immediately. Card authorizations reduce available balance in seconds. Incoming funds move differently. They must pass through clearing, netting, reserve settlement, verification, and ledger synchronization.

At 8:12 AM, that chain has not fully aligned. The screen reflects acknowledgment; it does not yet reflect true liquidity.

When the Number Changes

At 8:26 AM, the balance updates. The pending label disappears. Reserve accounts reconciled. ACH batches finalized. Exposure thresholds cleared. Nothing emotional shifted inside the institution. A sequence completed.

What felt like a missing paycheck was a timing interval inside institutional liquidity management. Once the system aligns, perception catches up to structure.

Author