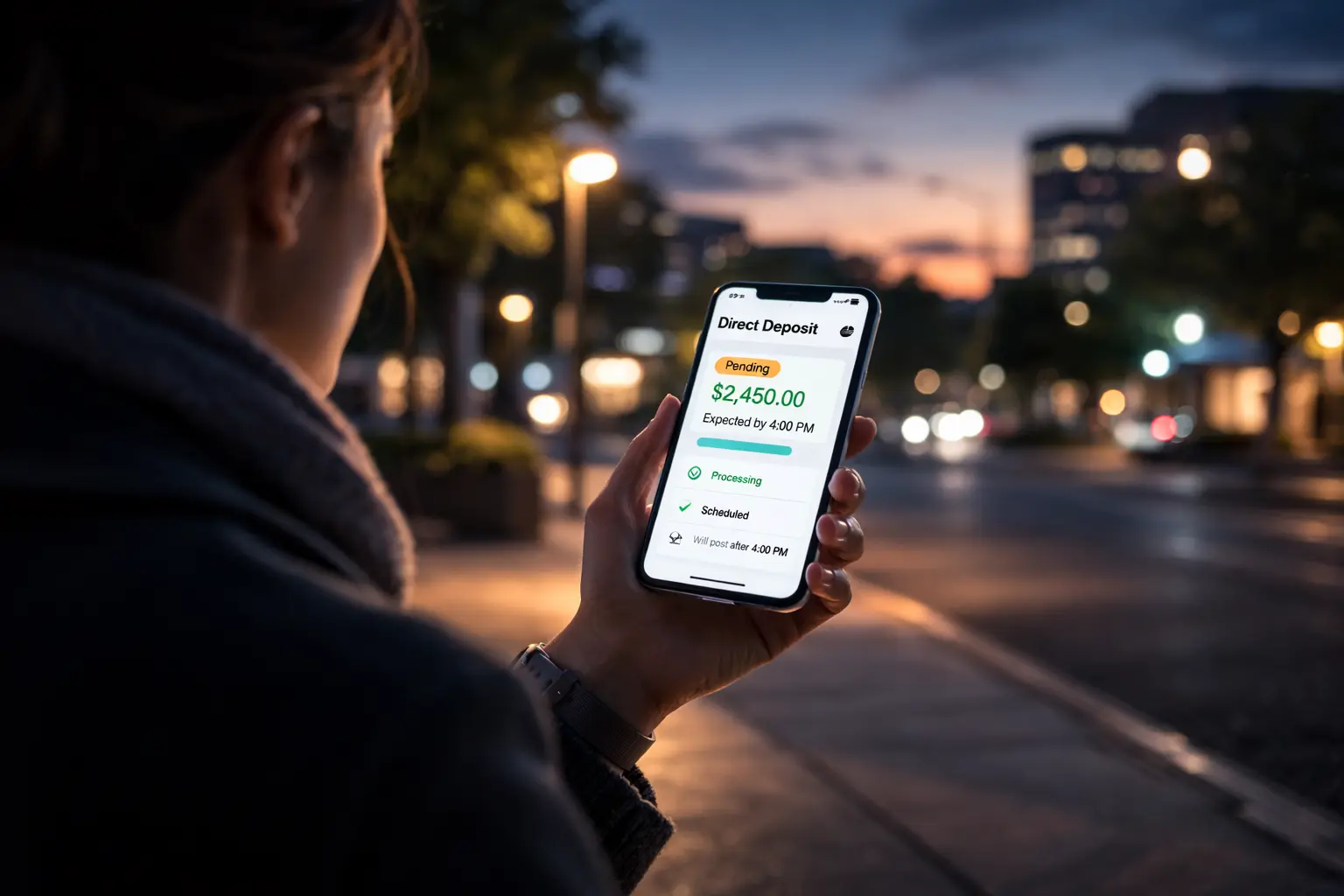

At 8:12 AM, the kitchen is quiet. A phone screen refreshes once. The expected Social Security payment day deposit is not there.

Bills draft automatically. Automatic payments do not adjust to posting windows. The pause feels personal. It rarely is. Another bank may already show the credit. What appears to be delay is usually structured sequencing inside the federal payment system.

Morning posting differences do not begin at the bank branch. They begin within coordinated Treasury transmission cycles, Federal Reserve settlement layers, and institutional liquidity controls that operate before most households wake. Understanding those layers requires stepping beyond the balance screen and into the architecture of the broader U.S. money movement system.

Treasury Transmission Occurs Before Retail Visibility

Social Security benefits originate through the Bureau of the Fiscal Service. The agency releases ACH credit files according to federal payment schedules. Those files enter the Federal Reserve’s processing environment in structured overnight batches.

The Treasury’s operational framework outlines how federal disbursements move from authorization to transmission. Readers can review the official Gold Book directly through the appropriate U.S. government source.

Authorization does not equal posting. Interbank settlement must occur before any retail ledger reflects funds. This distinction sits at the core of the money movement framework. Government agencies initiate payment instructions; the Federal Reserve processes and settles them. Commercial banks determine when to expose settled funds to customers. Retail timing follows institutional confirmation, not Treasury release.

Overnight ACH Processing and Settlement Finality

Social Security payments move through the Automated Clearing House network. ACH files containing federal credits enter Federal Reserve processing windows overnight, typically aligning with National Settlement Service cycles that finalize net interbank positions before dawn.

The Federal Reserve details operating hours and processing schedules. The system processes more than 30 million transactions on an average business day, and federal benefit credits travel within that same infrastructure.

Settlement often occurs before 6:00 AM Eastern, but posting to individual accounts usually happens later. Banks must reconcile inbound federal credits against outbound obligations.

This involves managing ACH cutoff timing and clearing queues that rank and net positions before reserve accounts adjust. That queue hierarchy determines visible posting order. Even after settlement finality, institutions perform additional checks before exposing balances.

Early-Morning Reserve Verification and Exposure Controls

Between roughly 6:30 and 8:30 AM Eastern, many banks conduct reserve verification against their master accounts at the Federal Reserve. These checks confirm that net credits from overnight settlement align with internal liquidity thresholds.

Reserve verification protects against daylight overdraft exposure and unexpected funding strain. High-volume federal payment days materially increase inbound credit totals. Institutions evaluate those totals against capital buffers and early deposit risk caps. This reserve settlement mechanics check occurs every business morning, not only on federal payment days.

If internal thresholds approach limits, posting may stagger by minutes while liquidity desks confirm sufficient cushion. Posting decisions depend on confirmed net position, not on perceived urgency.

Ledger-Day Rollover and Synchronization Windows

Another structural layer involves ledger-day rollover. Most banks close internal accounting ledgers during overnight batch processing. If a Social Security ACH file settles near that boundary, retail visibility may shift slightly forward.

Settlement finality at the Federal Reserve level precedes retail synchronization. Broader Federal Reserve operating schedules also influence liquidity forecasting. Although Social Security payments move through ACH, banks forecast reserve positions across both systems.

The settlement window timing across payment rails informs internal liquidity models. These synchronization windows collectively explain the common 8:00–9:00 AM posting range.

Why Posting Times Differ Across Banks

Consumers often compare timestamps. One bank posts at 8:04 AM. Another posts at 8:53 AM. The federal payment did not travel twice. Settlement occurred simultaneously at the interbank level.

Differences arise from liquidity architecture. Large institutions often maintain broader reserve cushions; their posting engines may activate quickly once reconciliation clears. Smaller institutions may route ACH files through layered verification workflows, often leaving the credit as direct deposit pending for a longer period.

Posting speed reflects liquidity architecture, not preference. Technology design, capital buffering, and internal synchronization checkpoints shape timing differences. None of those factors alter the underlying settlement event.

The 8:00–9:00 AM Retail Posting Window

The widely observed 8AM balance update window reflects coordinated completion of four internal steps:

- Overnight ACH batch reconciliation finalizes.

- Reserve accounts confirm net credit sufficiency.

- Exposure thresholds clear.

- Retail posting scripts activate.

Only after those confirmations does the deposit become available balance liquidity on the retail ledger. If reconciliation runs longer on a high-volume morning, visibility may approach 9:15 AM. Retail systems required final synchronization.

Returning to the Household Perspective

At 8:12 AM, the balance may not yet reflect the new credit. At 8:37 AM, it often updates without notice. On Social Security payment day, funds travel through federal settlement infrastructure before appearing in customer-facing ledgers.

The system operates methodically, not emotionally. Liquidity timing shapes perception more than authorization ever will.

Author