Every time a Social Security payment arrives, an IRS refund posts, or a federal benefit appears in your account, the transaction feels instant. A balance updates. A notification appears. Money becomes available.

But behind that simple moment is one of the most structured financial coordination systems in the world.

Federal payments do not travel directly from the government to your bank in real time. They move through a layered settlement architecture involving the U.S.

Treasury, the Federal Reserve, Automated Clearing House networks, liquidity verification checkpoints, and finally, your bank’s internal posting system.

Understanding how federal payments move from Treasury to your bank account removes confusion around “pending” statuses, posting delays, early deposits, and weekend timing gaps.

It also explains why two people can receive the same government benefit hours apart. This is the full U.S. settlement timeline explained.

Step 1: Treasury Disbursement Authorization

Every federal payment begins inside the U.S. Treasury’s disbursement systems. Whether the payment is a Social Security benefit, an SSI check, a veterans’ payment, or an IRS refund, the Treasury authorizes release through structured payment files.

These files contain batch instructions, not individual transfers. Instead of sending millions of payments one by one, the Treasury transmits grouped electronic instructions containing routing numbers, account numbers, and payment amounts.

Once authorized, these files are transmitted into federal settlement infrastructure. At this stage, the payment is approved, but it is not yet in your bank account. Approval is the beginning of the Treasury release cycle, not the final step.

Step 2: Entry Into the ACH Clearing System

Most federal payments travel through the Automated Clearing House network, commonly referred to as ACH. ACH is the payment rails infrastructure of recurring U.S. payments, including payroll, benefits, and tax refunds.

When Treasury sends payment files, they enter scheduled overnight clearing cycles. These windows operate in structured cycles, typically overnight and during business-day processing intervals.

During clearing, participating banks receive digital instructions indicating incoming credits. However, receipt of the instruction does not automatically mean funds are visible to customers.

Clearing confirms that the transaction has been routed correctly between institutions. Settlement determines when it is finalized.

Step 3: Settlement Through the Federal Reserve

The Federal Reserve plays a central role in settlement. It operates the core infrastructure that allows financial institutions to reconcile balances between one another through Fed settlement mechanics.

When ACH files are processed, interbank positions must be balanced. If Bank A owes Bank B a net amount from payment exchanges, the Federal Reserve adjusts reserve balances accordingly.

This reserve adjustment is what gives federal payments institutional finality. It ensures that the sending institution has actually transferred funds to the receiving institution at the reserve level.

At this point, settlement has occurred between banks, but posting to individual customer accounts may still be pending.

Fedwire vs ACH: Why It Matters

Not all federal money moves the same way.

ACH is designed for high-volume, lower-value batch payments such as Social Security benefits and payroll. It processes in scheduled windows and is optimized for efficiency. Readers can review the official FedACH schedules for detailed timing.

Fedwire, by contrast, handles real-time gross settlement for higher-value transactions. It operates continuously during Fedwire vs ACH timing hours and is typically used for institutional transfers rather than retail benefit payments.

Most individuals receiving federal benefits interact primarily with ACH settlement timing, not Fedwire. But both systems operate within the Federal Reserve’s broader settlement framework.

Understanding this distinction clarifies why government payments are not instant even in 2026.

Step 4: Liquidity Verification at Your Bank

Once settlement between institutions is complete, your bank receives confirmation of incoming funds. However, before releasing money to your account balance, banks perform internal liquidity verification.

Liquidity verification ensures that reserve balances align with expected incoming totals. Even though the Federal Reserve has settled positions, banks still conduct internal settlement windows reconciliation cycles.

This is why many retail banks post federal deposits during the Social Security posting window, often between 6:00 AM and 9:00 AM local time.

The gap between settlement and posting is where most confusion happens. Customers may see pending deposits explained during this stage. The money has been routed and settled at the institutional level, but internal posting waves have not yet executed.

Step 5: Posting to Your Account Ledger

Posting is the final visible step. It is when your bank updates your account ledger to reflect available balance logic.

Posting differences vary by institution. Some banks pre-position liquidity and release federal deposits early. Others wait for full internal verification before making funds accessible.

This difference explains why two Social Security recipients with different banks may see deposits at different times on the same day. Posting timing is a policy decision layered on top of settlement completion.

Settlement vs Posting: The Core Distinction

One of the most misunderstood aspects of federal payments is the difference between settlement and posting.

Settlement occurs between financial institutions through Federal Reserve systems. It confirms that funds have moved at the reserve level. Posting is a bank-level action that updates your visible balance.

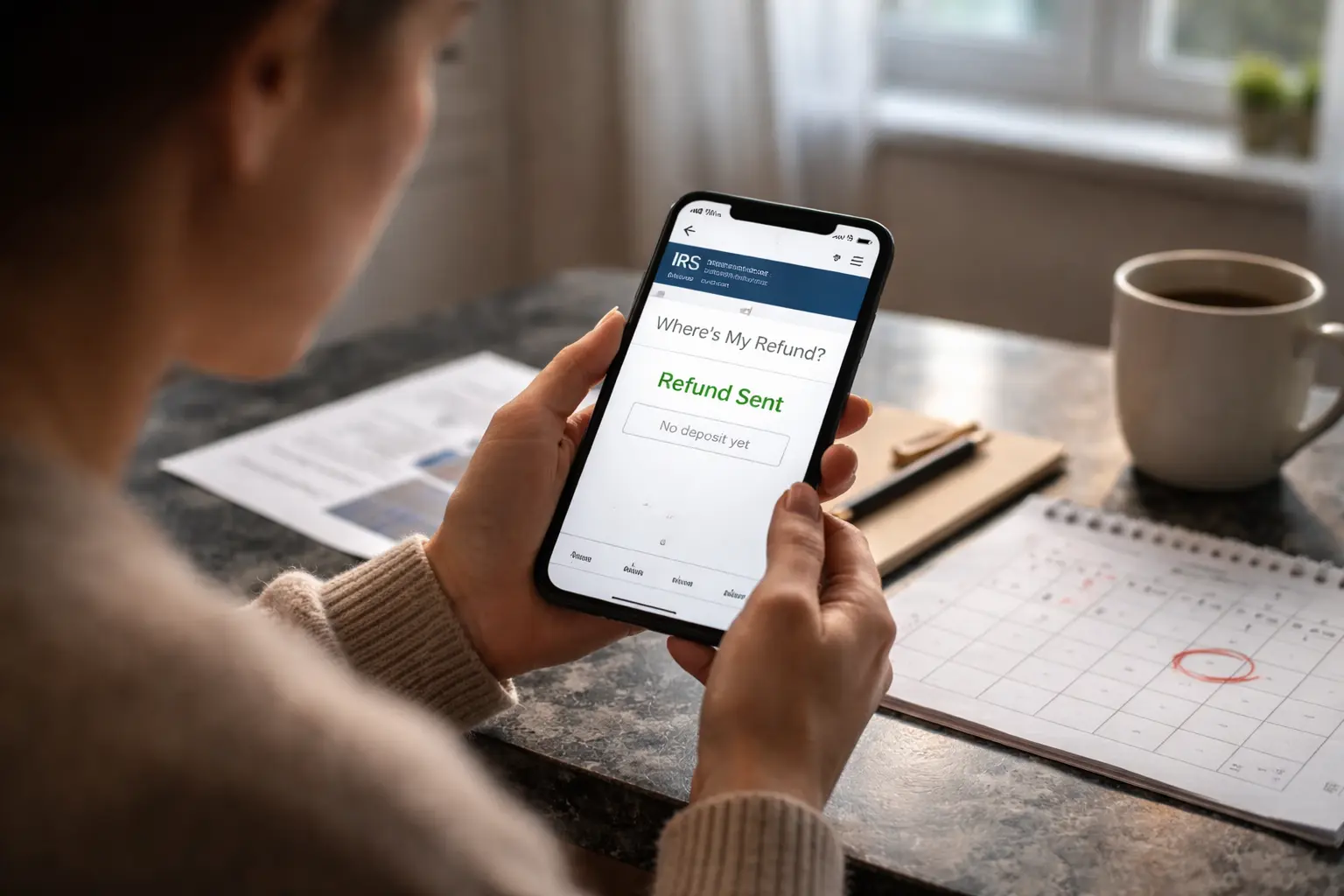

When people ask why a refund has a refund sent status but is not in their account, they are observing the gap between these two stages. That gap is procedural, not a malfunction.

The Federal Payment Timeline: From Treasury Release to Bank Posting

Federal payments move through a layered structure. Each stage is controlled by a different institution and serves a distinct purpose. The timeline below shows how money travels from government authorization to visible balance.

| Stage | Institution Responsible | What Happens | Visible to Customer |

|---|---|---|---|

| Treasury Authorization | U.S. Treasury | Payment file created and approved | No |

| ACH Clearing Window | ACH Network | File routed between financial institutions | No |

| Federal Reserve Settlement | Federal Reserve | Reserve balances adjusted between banks | No |

| Bank Liquidity Verification | Receiving Bank | Internal reserve confirmation and reconciliation | Sometimes shows “Pending” |

| Ledger Posting | Receiving Bank | Funds credited and available in account | Yes |

Source framework derived from U.S. Treasury disbursement procedures, Federal Reserve settlement operations, and ACH network processing guidelines.

Why Timing Changes During High-Volume Weeks

During periods of heavy federal payment volume, such as overlapping Social Security waves and IRS refund timing surges, settlement loads increase significantly.

Banks may adjust posting timing slightly during these high-volume cycles to manage liquidity buffers and processing order. This can create the perception of slower deposits even though the infrastructure is functioning normally.

Calendar shifts, federal holidays, and end-of-month surges can all influence the visible timing of federal funds. But the underlying path remains the same.

The Role of ACH Clearing Windows

ACH does not process continuously in the same way card networks do. It operates in defined ACH cutoff timing windows.

If a Treasury file enters the network after a cutoff, it may roll into the next processing window. That is why same-day ACH differs from standard batch timing.

Cutoff timing, settlement cycles, and bank posting waves form a synchronized chain. When one element shifts, visibility shifts. The structure itself remains stable.

Why This Infrastructure Matters for Households

Understanding how federal payments move from Treasury to your bank account reduces unnecessary anxiety during payment weeks.

If you see a CP53E notice or a pending status overnight, you are likely between settlement and posting. If a deposit appears early at one bank but not another, you are observing differences in posting policy, not preferential treatment.

And if a weekend passes without visible funds, it may reflect ACH business-day timing rather than payment cancellation. The U.S. money movement system is layered, disciplined, and predictable, even when visibility feels inconsistent.

The Full U.S. Settlement Timeline, Simplified

This structured sequence represents the core journey of every federal dollar from government authorization to your available balance. Each phase must conclude successfully within specific regulatory and technical windows before the next layer of the U.S. money movement system can trigger.

1. Treasury Authorization: The process begins when the Bureau of the Fiscal Service generates overnight Treasury releases for approved benefit or tax files.

2. ACH Routing: Payment files enter the payment rails infrastructure where they are sorted and routed to the correct financial institutions.

3. Federal Reserve Settlement: Institutional finality occurs as the Fed adjusts reserve balances between banks during specific settlement windows.

4. Liquidity Verification: Receiving banks perform internal checks to ensure true liquidity available matches the incoming settlement data.

5. Ledger Posting: The bank executes final posting waves to update your account, moving funds from “pending” to “available.”

Each step is independent, yet synchronized. And each layer explains why federal payments sometimes feel immediate, and sometimes delayed.

Final Perspective

Federal payments are not random transfers. They move through one of the most structured financial infrastructures in the world.

Treasury disbursement, ACH clearing windows, Federal Reserve settlement, liquidity verification, and bank posting all operate in coordinated cycles.

When visibility shifts, it reflects timing between these layers, not instability in the system. By understanding the full U.S. settlement timeline, you can interpret deposit timing with clarity instead of concern. And that clarity is the foundation of real financial confidence.

Author