Across financial institutions, a familiar pattern unfolds almost every morning inside the banking system. Long before most people begin their day, financial institutions start processing deposit files that arrived overnight.

By the time millions of Americans open their banking apps, the first round of account updates may already be underway. That moment, when balances suddenly change in the early hours, is often called the morning deposit window.

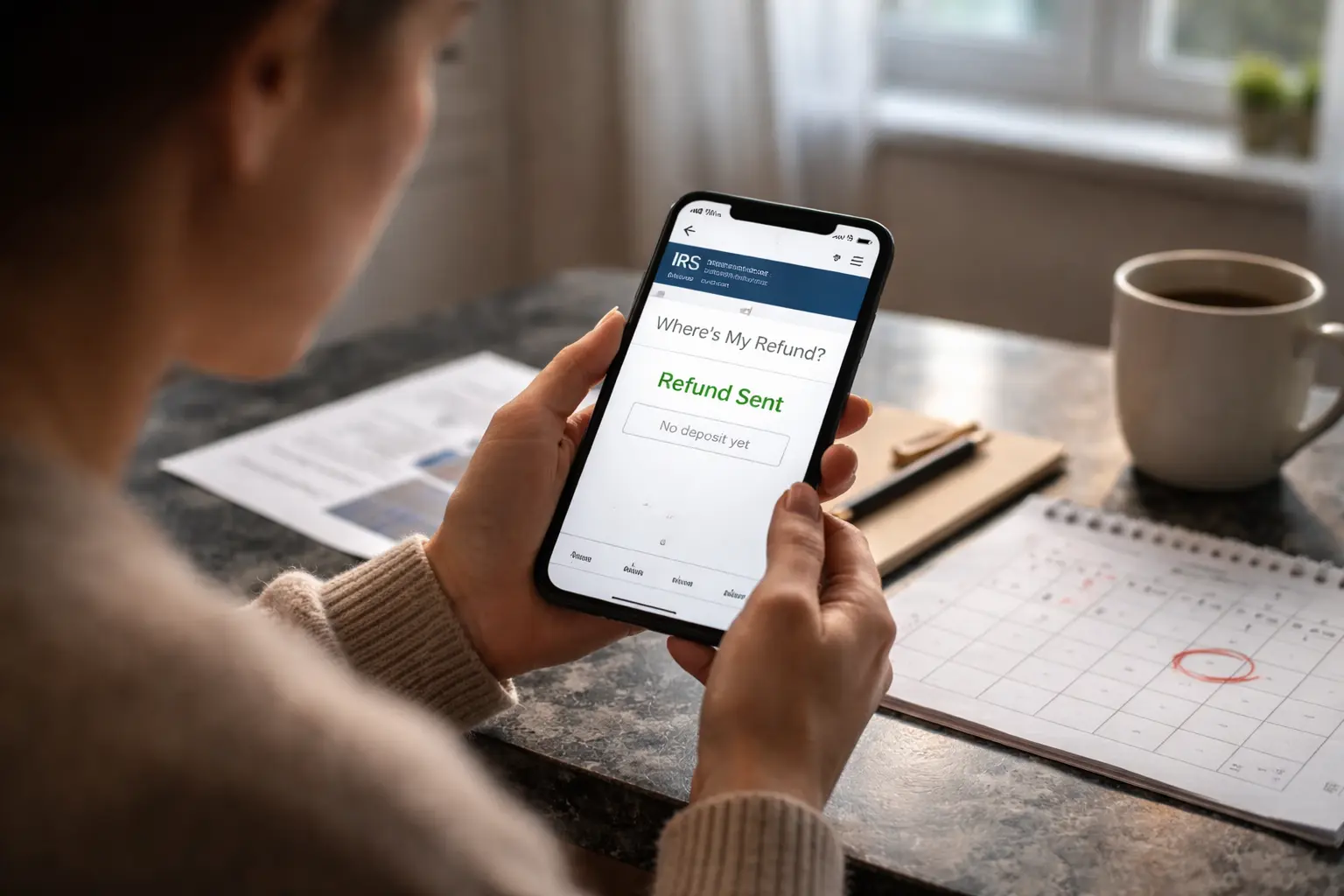

It is one of the primary periods when banks begin posting incoming transactions from payroll providers, federal payments, tax refunds, and other direct deposits.

Through the national payment system, these funds move securely. But this window does not open everywhere at the same time. As today’s banking cycles begin, some accounts may update early while others remain unchanged until later in the day.

The Morning Deposit Cycle

Most direct deposits in the United States move through the banking system overnight. During this time, employers, federal agencies, and payment processors transmit large batches of payment instructions into the ACH clearing network.

These transactions are grouped into settlement files that financial institutions begin receiving in the early hours of the morning. When banks receive these files, they start preparing the deposits for posting to customer accounts.

This process creates the first deposit cycle of the day. For many banks, the earliest posting windows occur in the pre-dawn hours or shortly after sunrise, often influenced by the Treasury payment release.

Once the system begins updating balances, customers may suddenly see deposits appear when they open their banking apps. However, this is only the first stage of the day’s processing activity.

How Banks Receive Payment Files

When deposits are initiated, they travel through a structured network that moves funds between financial institutions. Payment files from employers, Treasury agencies, and financial service providers enter clearing systems designed to coordinate settlement between banks.

These systems transmit deposit batches to receiving institutions overnight. When banks receive those files, they begin direct deposit processing steps to verify the transactions and prepare them for posting.

Although customers only see the final balance update, several institutional layers operate behind the scenes to move funds through the payment system.

Each bank must reconcile incoming settlement data before making deposits visible inside customer accounts. Because these files arrive in groups, banks often process them sequentially rather than simultaneously.

Why Deposits Appear in Waves

One of the most noticeable characteristics of deposit timing is that balances rarely update everywhere at once. Instead, deposits tend to appear in waves. The first wave typically occurs when banks process early settlement files that arrived overnight.

Once those deposits are posted, additional files may continue arriving from clearing networks throughout the morning. Banks process each batch according to their bank posting windows. Some institutions release deposits as soon as files are verified, while others wait until the next scheduled posting window.

This structure explains why one account might update early in the morning while another remains unchanged for several hours, even if both payments were issued at the same time.

The system prioritizes accuracy and reconciliation, which naturally produces staggered deposit settlement timing across different banks.

What Happens During the Next Posting Window

As the morning progresses, additional deposit batches continue moving through the banking system. Banks receive new settlement files and run them through internal verification processes before posting funds to accounts.

Each institution determines when the next posting cycle will occur, often adhering to a strict ACH cutoff schedule, which can happen at different points during the day.

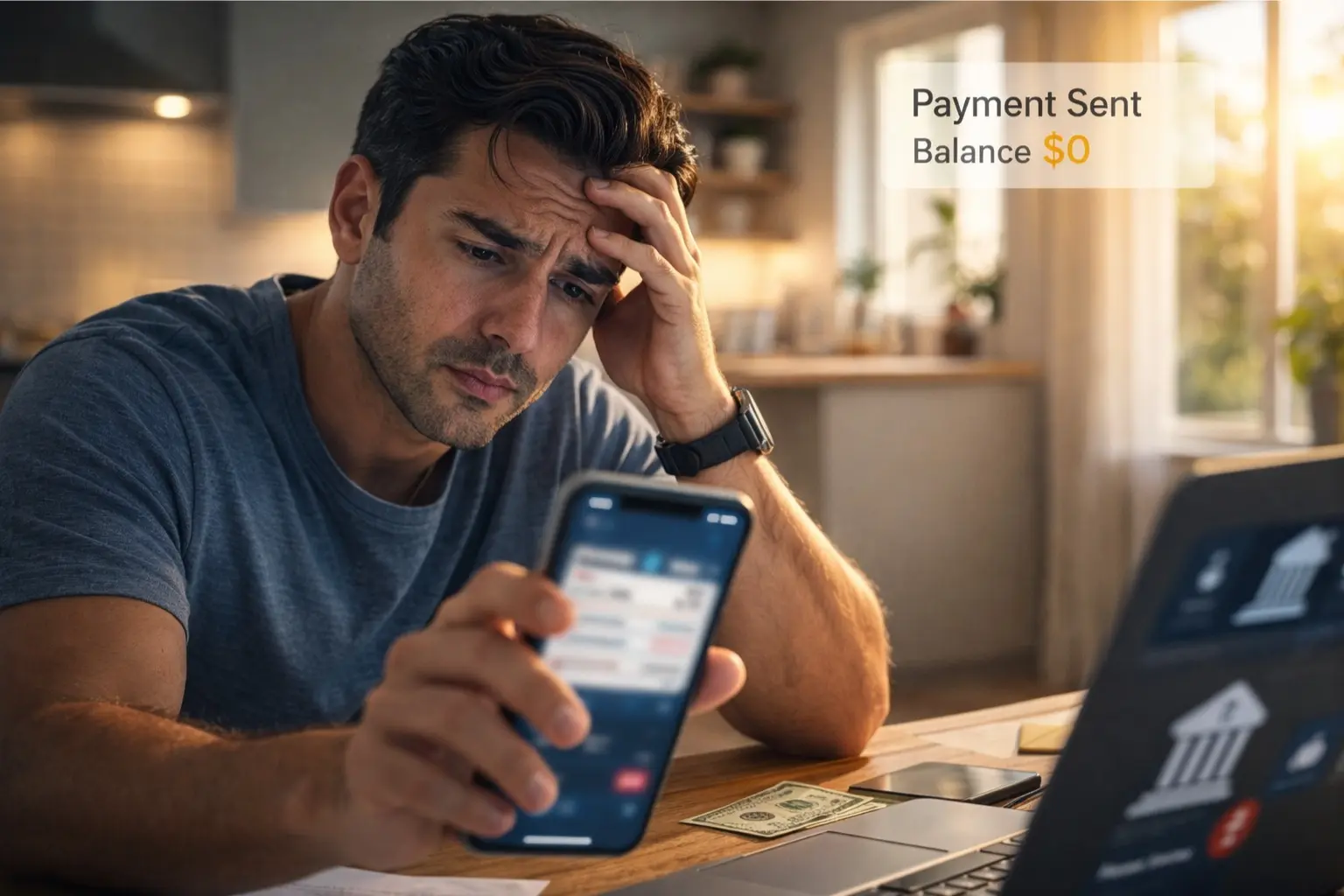

For customers waiting on deposits, this means a balance that has not changed yet may simply be waiting for the next posting window to open. In many cases, deposits that do not appear during the earliest deposit batch cycles become visible later in the day once additional processing batches are released.

Understanding how these cycles operate, including the nuance in balance update timing, helps explain why deposit timing can vary even when payments were transmitted at the same time.

As banks continue processing incoming files throughout the day, the next deposit wave may mean more accounts across the country begin reflecting new deposits.

Author