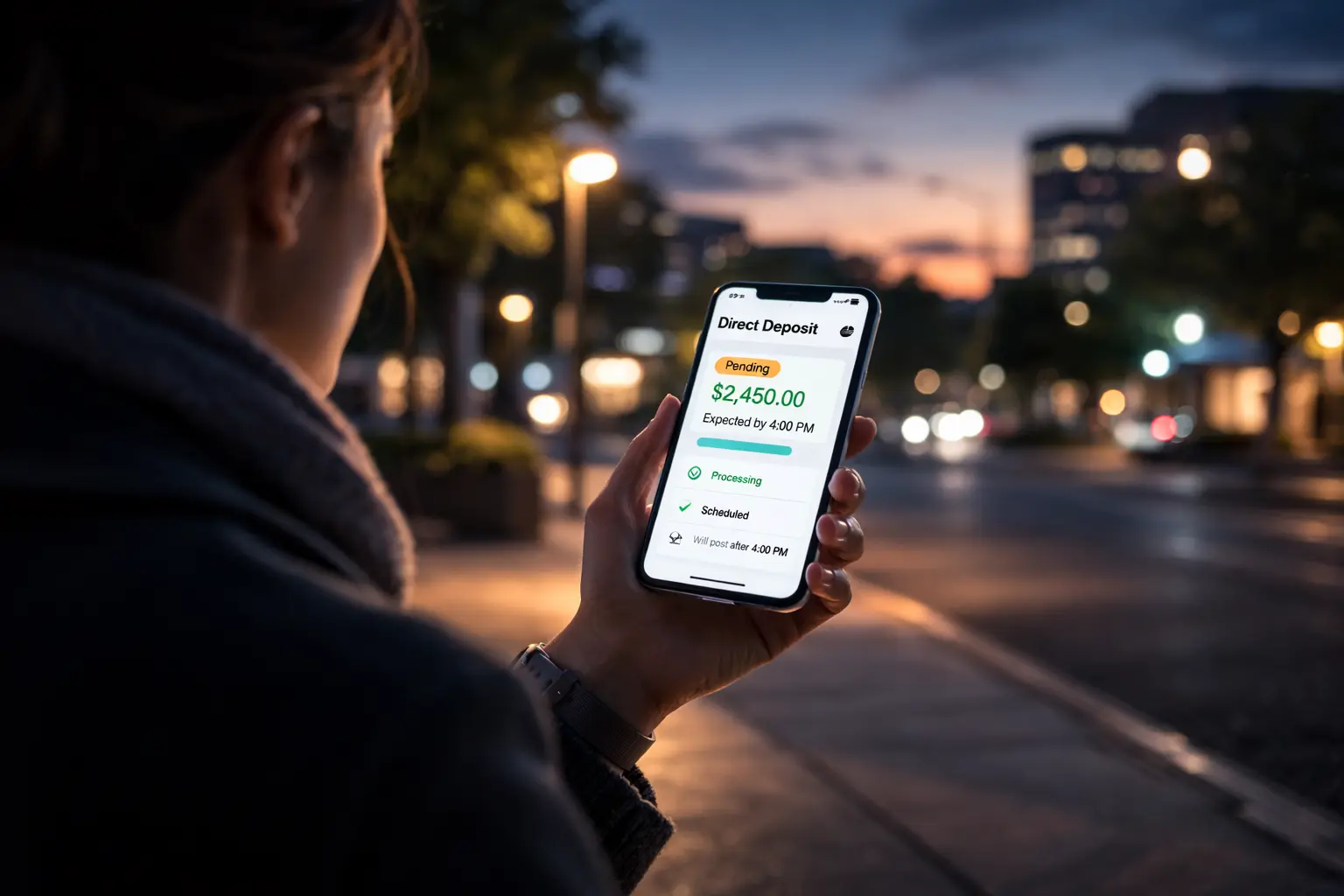

It says pending. The money is there. But you still can’t use it. If your bank app shows a deposit as ‘pending’ yet your available balance hasn’t moved, you’re inside one of the most misunderstood moments in the U.S. banking system. The funds are not frozen. They are not rejected. They are waiting for final release. Here’s what that actually means.

Why ‘Pending’ Is Not the Same as ‘Posted’

When a federal payment or payroll deposit arrives at your bank, it first enters a notification phase. The institution receives confirmation of incoming funds before it releases them into your spendable balance. That intermediate stage is why direct deposits clearing happens this way.

The bank sees the money. You see the status. But the system has not completed final settlement. That final step is controlled by the broader U.S. money system infrastructure. Pending does not mean problem. It means sequencing.

The Exact Minute Banks Release Funds

Most institutions do not release deposits randomly. They finalize availability during structured posting windows tied to Automated Clearing House cycles. The timing gap between notification and availability is governed by settlement window timing rules.

Some banks update available balances at 6:00 AM. Others closer to 8:00 or 9:00 AM. Some fintech platforms batch slightly later. That difference is not about the IRS or employer.

It’s about your bank’s internal liquidity release policy. The mechanics behind those cycles are detailed in overnight bank clearing systems. If your deposit is pending this morning, you are likely waiting for that internal release checkpoint.

Why This Moment Feels Like a Delay

Seeing ‘pending’ creates urgency because it suggests the money is right there. Technically, it is. But only at the interbank confirmation level. The distinction between visible balance and actual usable funds is explained in true liquidity balance mechanics.

Until the bank updates its core ledger and reserve positioning, funds remain unavailable for withdrawal or transfer. This is especially common after weekends or federal holidays.

Timing compression following non-business days is explained in weekend banking slowdown patterns. The system is catching up. Not stopping.

Federal Payment Pending? Here’s What’s Moving

If your pending deposit is tied to a federal payment or tax refund, the release timeline begins with Treasury transmission. That release stage is governed by official IRS Refund Guidance. Once the Treasury sends the file, it moves through ACH cycles before banks mark funds available.

The cutoff that determines which posting window your deposit enters is explained in ACH cutoff timing rules. If your deposit entered just after a cutoff, it simply rolls into the next batch cycle. That can create a short but stressful gap between pending and posted.

Why Some Accounts Update Before Yours

Two people can receive the same payment on the same day and see different availability times. That difference is controlled by bank posting timing windows. Some institutions pre-release funds. Others wait for final reserve confirmation. The strategic risk management behind those choices is explored in liquidity risk mechanics. Banks are not slow. They are cautious.

When ‘Pending’ Actually Signals a Problem

In most cases, pending simply means waiting for structured posting. It becomes unusual only if the next full business cycle passes with no update, a rejection notice appears, or the IRS indicates an offset under official IRS Offset Rules. If none of those apply, your pending status is part of scheduled release sequencing.

What Happens Next

Right now, banks are reconciling reserves, confirming ACH batches, and synchronizing ledger updates. When that process completes, pending becomes posted. And posted becomes available. That final moment is invisible until it happens. But it is structured. And it is predictable.

The Bottom Line

A deposit showing pending but not available does not mean delay. It means you are inside the final release window of the U.S. settlement system. Your bank sees the funds. The network confirms the transfer. The ledger just hasn’t flipped yet. And when it does, it happens instantly.

For additional context on how these financial infrastructures operate at the institutional level, you may also find information from the Federal Reserve Payment Overview useful.

Author