A federal payment was released. The status changed. The date matched. The system says it was sent. And yet your bank balance hasn’t moved. It feels like something stalled. It feels like a freeze. And it feels personal. But it isn’t.

What you’re experiencing right now is one of the most misunderstood stages in the U.S. payment infrastructure, the gap between federal release and bank ledger availability. And that gap is where tension lives.

‘Released’ Does Not Mean ‘Available’

When a federal agency issues a payment, whether it’s a Social Security benefit, an IRS refund, or another Treasury disbursement, the word ‘released’ means the funds have entered the federal payment network.

It does not mean your bank has posted them to your account. We broke down this full system architecture in the U.S. payment system. That release stage is the beginning of a settlement chain, not the end.

What Happens After Treasury Sends the Payment

Once Treasury initiates a payment file, it enters structured coordination channels. This includes federal authorization, transmission to the ACH network, distribution to receiving banks, bank-level reconciliation, and final posting window.

The mechanics behind that early phase are detailed in the Treasury payment system before deposit. Your bank does not simply ‘receive and display.’ It receives, verifies, batches, and schedules. And that scheduling is where the freeze feeling begins.

Why Your Balance Looks Frozen

Most banks operate within defined posting windows. Even if the incoming file is received overnight, internal systems often wait for coordinated ledger updates. We’ve outlined how these posting windows vary in banks control payment posting windows.

Some banks update between midnight and 3 AM, some between 6 AM and 9 AM, and others finalize later in the morning. If your bank hasn’t reached its designated posting cycle, your balance remains unchanged even though the funds are already moving inside the infrastructure. That’s not a freeze; that’s sequencing.

The ACH Coordination Layer Most People Don’t See

The majority of federal payments move through the Automated Clearing House network. ACH operates in structured settlement batches; it does not function like instant peer-to-peer transfers.

We explained this difference clearly in Fedwire and ACH liquidity timing. ACH requires coordination and finality. Until final settlement clears inside your bank’s internal ledger system, your available balance will not change.

Why Other People’s Deposits Appear First

This is where anxiety spikes. Someone you know says theirs hit, your coworker shows a screenshot, social media fills with confirmation posts, and your account still shows the same number. This difference is caused by internal bank policy, not payment denial.

Some institutions allow early visibility of pending funds, while others wait for confirmed settlement. We explored that distinction in direct deposits show pending before clearing. Visibility is not availability, and absence of visibility is not absence of payment.

The Overnight Gap That Creates Morning Stress

Many federal payments are transmitted during evening cycles, but banks often finalize posting during defined overnight reconciliation periods. This process is explained further in overnight bank clearing cycles.

If your payment was released late in the day, your bank may not update your available balance until its next operational window. That delay can feel like a system pause, but in reality, it’s controlled sequencing.

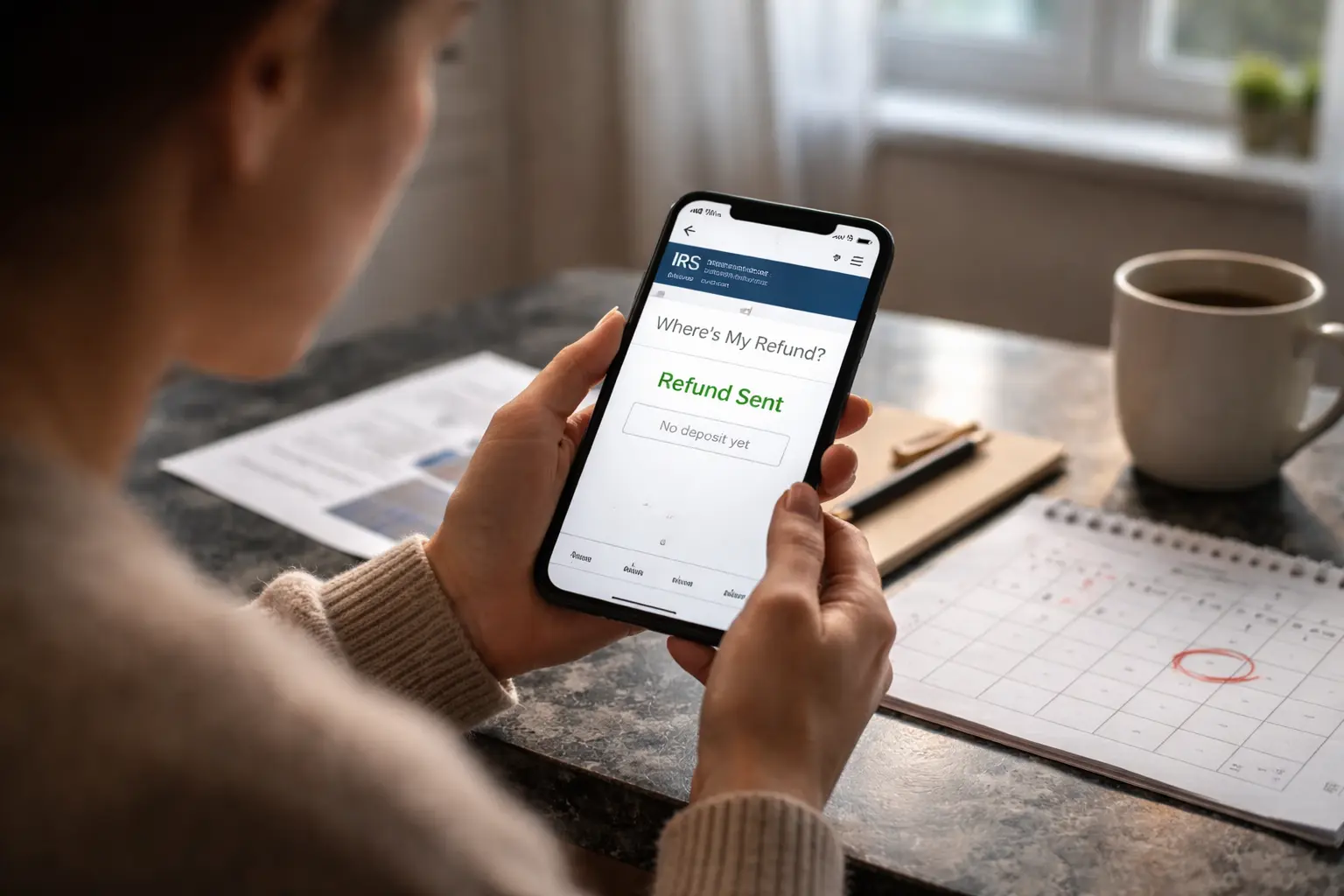

When a Frozen Balance Actually Signals a Problem

Most frozen-looking balances resolve within the same business day. However, you should investigate if a full business day passes with no change, you recently changed bank details, or you received an IRS offset notice.

For IRS-specific refund timing guidance, see the official IRS refund processing page. For federal payment system information, refer to the U.S. Treasury Fiscal Service. Those are the primary federal authorities.

The Psychology of Release vs Reality

The word ‘released’ creates an expectation of immediacy, but the system prioritizes reconciliation, fraud controls, liquidity coordination, and risk buffers. We discussed how liquidity timing impacts households in liquidity timing household stability. Speed is secondary to settlement integrity, and settlement integrity requires sequencing.

Why This Feels More Intense During High-Volume Periods

When millions of federal payments are issued within narrow windows, such as benefit days or peak tax season, banks experience concentrated inflows. This creates staggered visibility across institutions. The structured flow is explained in the federal payment timeline explained. Not all balances update simultaneously; they cascade.

The Ending Line

If a federal payment was released but your balance still looks frozen, the payment likely entered the system, your bank likely received the file, and your posting window likely hasn’t finalized yet.

The infrastructure is moving, even if your app isn’t. Understanding that difference reduces unnecessary panic, because a frozen balance during settlement is usually a timing gap, not a denial.

Author