When a federal payment shows ‘approved,’ most people assume the money is already on the way to their bank account. But approval is only one step inside a much larger structure. Between IRS authorization, Treasury release, Federal Reserve processing, and bank posting windows, multiple institutional layers coordinate before cash becomes available.

Understanding the U.S. money system removes confusion around pending deposits, Sunday delays, and morning posting gaps. This guide explains, step by step, how federal payments actually move, and why ‘approved’ rarely means ‘available immediately.’

Step 1: What ‘Approved’ Really Means Inside the Federal System

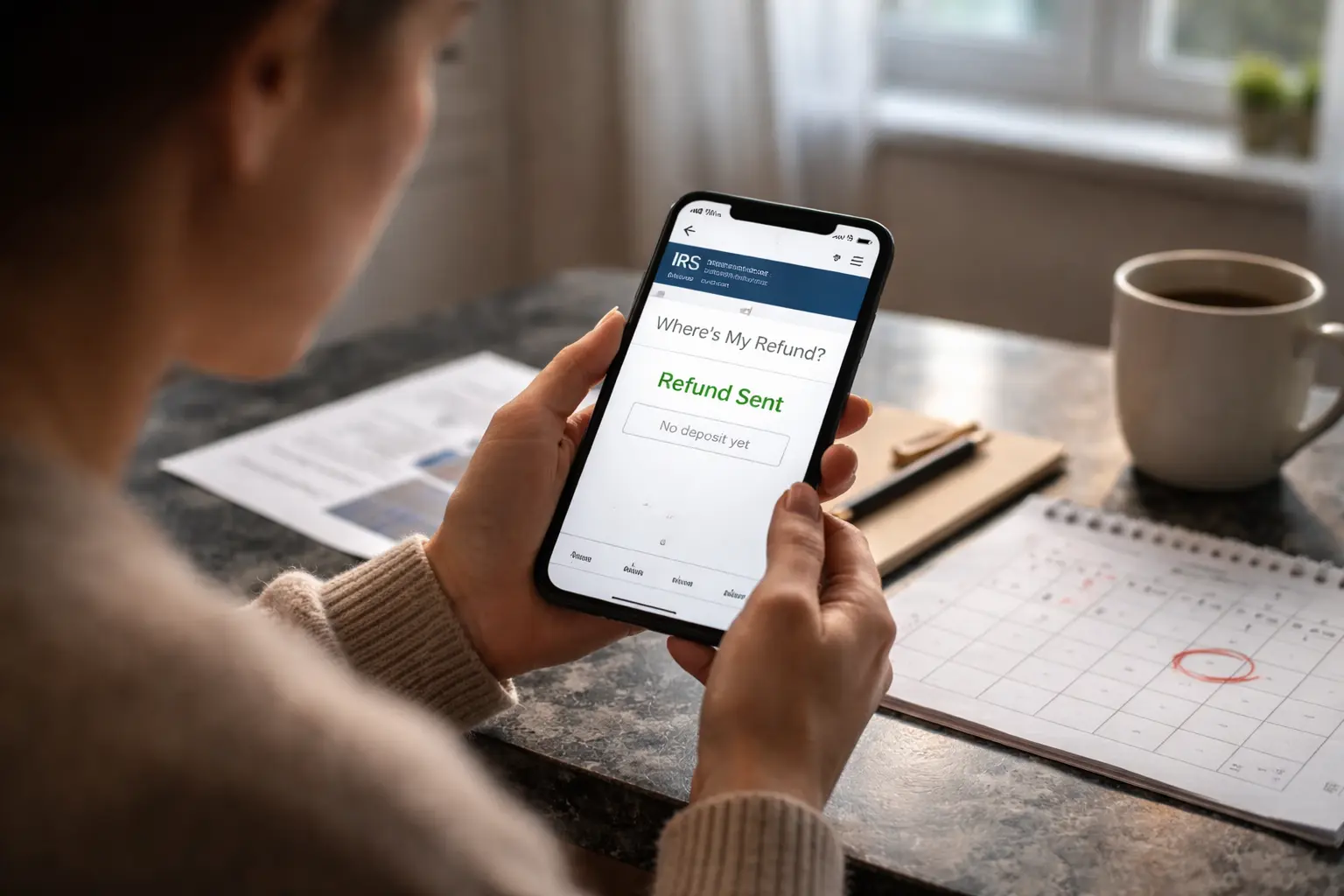

When the IRS marks a refund as approved, it signals that your tax return has cleared internal review and is authorized for disbursement. For many taxpayers, this is associated with Code 846 on an IRS transcript, which represents a refund issued status.

However, approval does not mean the money has landed in your bank account. It means the payment instruction has been created and scheduled for transmission.

The IRS does not directly deposit funds into personal bank accounts. Instead, the Department of the Treasury initiates the actual payment release. That file is then routed through the federal payment infrastructure. Inside the broader settlement timeline, approval is an administrative milestone — not a liquidity event.

Step 2: Treasury Release and the Federal Reserve Processing Layer

Once approved, the refund or federal benefit payment enters the Treasury disbursement phase. The Treasury aggregates payment files and sends them into the banking system through structured channels.

Most individual payments move via the Automated Clearing House (ACH) network. High-value institutional transfers may move through Fedwire, but Social Security and IRS refunds typically use ACH batches.

The ACH system operates in coordinated same-day ACH windows. Payments are grouped, transmitted, cleared, and settled in cycles rather than individually in real time.

This structure explains why many people see deposits cluster on specific mornings rather than arrive at random hours. Within the U.S. federal payment timeline, Treasury release timing does not equal immediate settlement. It begins the clearing process.

Step 3: ACH Clearing vs. Final Settlement

Clearing and settlement are distinct processes. Clearing identifies and verifies payment obligations between financial institutions. Settlement is the final movement of reserves between banks at the Federal Reserve level.

During clearing, your bank is notified of incoming funds. That is when many banking apps display a ‘pending deposits explained‘ deposit. Settlement occurs when reserve balances are adjusted.

Only after this step can a bank fully release funds into available balances without risk exposure. This is why you may see a refund listed in your transaction history but not reflected in your available balance. The gap between these two steps is one of the most misunderstood elements of the U.S. federal payment timeline.

Step 4: Why Banks Show ‘Pending’ Before ‘Available’

Banks manage internal liquidity carefully. Even when a payment has cleared at the ACH level, institutions often conduct additional verification before making funds spendable. This includes: Reserve reconciliation Fraud monitoring checks Core ledger synchronization Risk buffer validation

Many banks perform these updates during designated posting windows, typically between early morning hours. For example, some institutions update balances around 6:00 AM local time, while others finalize between 8:00 and 9:00 AM.

This explains why two people with the same refund date can see different availability times. Within the U.S. federal payment timeline, pending vs available status reflects structural sequencing, not delay.

Step 5: The Weekend and Sunday Bridge Effect

Weekend timing introduces a visible pause in settlement cycles. Although payment files can be transmitted ahead of schedule, new ACH settlement batches generally do not finalize on Sundays. Instead, banks stage deposits internally for the next full processing window.

This creates what many perceive as a ‘freeze,’ but it is actually a staging period between visibility and liquidity. If a payment appears on a Sunday as pending but not available, it often transitions during Monday’s early processing cycle. The weekend settlement pause is not a malfunction. It is a feature of coordinated settlement design.

Step 6: Federal Holidays and Liquidity Shifts

Federal holidays further affect timing. When the Federal Reserve system is closed for a holiday, settlement windows shift. Payments scheduled near those dates may appear early or stage temporarily before final posting.

This is particularly noticeable when the first of the month falls near a weekend or holiday, affecting Social Security schedules. These shifts do not cancel or reduce payments. They simply alter the sequencing inside holiday liquidity shifts.

Step 7: IRS Refunds vs. Social Security Payments

While both use federal payment infrastructure, refunds and Social Security benefits originate from different administrative paths. IRS refunds follow tax return processing cycles and may be influenced by legislative filters such as PATH Act review windows.

Social Security payments follow benefit disbursement calendars, often aligned with birth dates or standardized monthly schedules. Despite these administrative differences, both converge into the same ACH cutoff timing framework. That convergence is where timing patterns become visible to individuals checking their balances.

Step 8: Why Posting Times Differ by Bank

Bank posting time differences are often misinterpreted as errors. In reality, institutions have discretion over when to credit incoming funds to customer accounts. Some banks provide early access as a competitive feature. Others wait for complete reserve confirmation before releasing funds.

This difference in internal policy is why one account may show funds available at 6:00 AM while another shows pending until 9:00 AM. Both are aligned with the same federal transmission timeline. The variation happens at the final institutional layer.

Step 9: When a Delay Is Actually a Problem

Most perceived delays resolve naturally within one business day. However, genuine issues may arise if: No deposit appears at all after the scheduled date Incorrect account information was provided The refund was offset for obligations The bank rejected the transfer

In those cases, further verification with the IRS or the financial institution may be necessary. But visible pending status alone is rarely cause for concern.

Step 10: The Psychological Effect of Real-Time Banking

Modern mobile banking apps allow users to see intermediate processing stages that were previously invisible. Years ago, individuals only saw final balances after full posting. Today, pending notifications create awareness of each step inside the invisible payment rails.

This transparency increases anxiety during processing windows. The system itself has not become slower. It has become more visible. Understanding the structure reduces misinterpretation.

The Structural Recap: From Approval to Availability

The full timeline can be summarized as follows: IRS approval authorizes payment. Treasury releases payment instruction. ACH clearing notifies banks. Settlement adjusts reserve balances. Banks complete final posting window. Available balance updates.

Each stage serves a purpose. None are redundant. When you see a pending deposit, you are observing the middle of that sequence, not the end.

Why Understanding the U.S. Federal Payment Timeline Matters

Knowing how federal payments move does more than reduce confusion. It improves financial planning. When you understand posting windows, weekend bridges, and reserve verification timing, you can anticipate availability instead of reacting emotionally.

The U.S. federal payment timeline is a coordinated infrastructure designed for stability, scale, and risk management. It prioritizes systemic reliability over cosmetic speed. And when viewed in full, it becomes predictable.

Final Perspective

Federal payments do not move randomly. They follow structured institutional choreography. Approval is administrative. Release is procedural. Clearing is technical. Settlement is final. Availability is the last visible step.

When a refund or Social Security benefit appears pending, it is not lost in the system. It is inside the system. Understanding the complete U.S. federal payment timeline transforms uncertainty into clarity. And clarity is what turns temporary anxiety into long-term confidence.

Author